The ETF Portfolio Strategist: 01 Jan 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

A new year has arrived but the old trends still prevail. But hope springs eternal and so 2023 may dispense something new. To be determined. Meanwhile, the bearish trends of 2022 are assumed to spill over into the start of trading for 2023, at least until the markets make a convincing case otherwise.

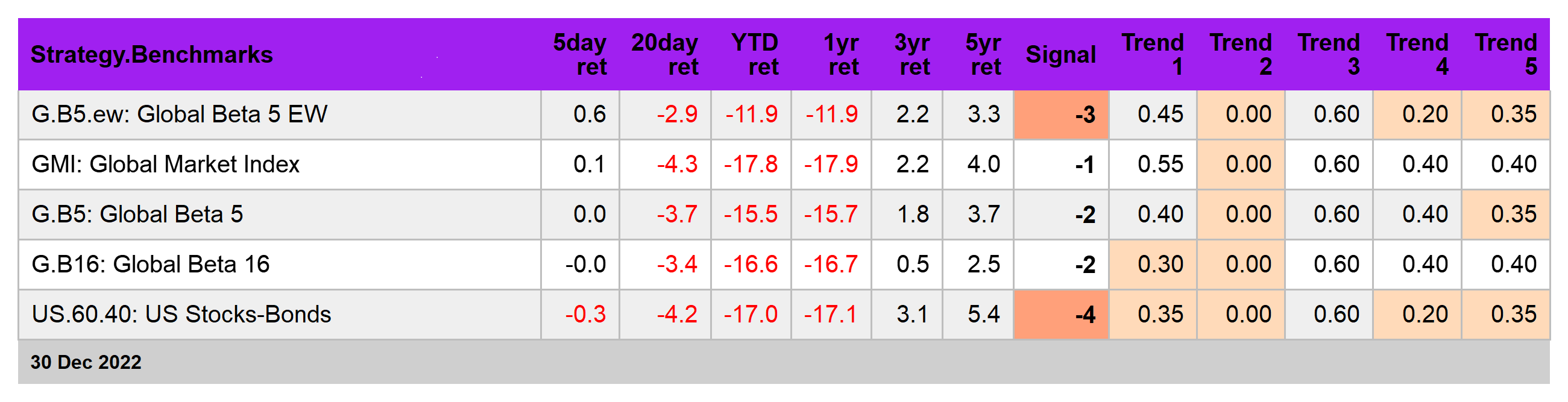

The trends at 2022’s close were biased to the downside for our 16-fund global opportunity set, with one exception: junk bonds ex-US. For details on the metrics in the table below, see this summary.

VanEck Vectors International High Yield Bond ETF (IHY) has rebounded in recent weeks and is now poised to extend the rally, or so it seems. It’s encouraging to see IHY posting a 4 for our aggregated Signal score (one notch below 5, the highest level of upside momentum). It’s still early to confidently forecast an extended bull run for IHY, but at the moment this slice of the bond market is on the short list to monitor as a possible early candidate for upside regime shift in the new year. On that point, let’s see if IHY can hold on to its rebound in the days ahead.

US stocks (VTI), by contrast, still look caught in a bear market. Late last year the ETF mounted a rally for the third time in 2022, and for a third time the rally failed. The test is whether the current slide runs below the previous low in October, which would reaffirm the bear-market trend.

US Treasuries are in a similar state. The latest gap down for the final trading week of the year isn’t reassuring.

Commodities (GCC) have been immune to the selling that otherwise dominated 2022. But with inflation peaking, or so it appears, and recession risk rising it’s not obvious that GCC is about to repeat its early 2022 rally.

From a strategic perspective, a key question is whether the G.B16 strategy benchmark begins to stabilizing after a year of trending down. To be fair, nothing’s changed simply because the calendar flipped to Jan. 1, but perhaps the crowd will sense that change for the better is in the air. Maybe, but most of the ills that plagued last year are still lurking. See this summary for design details on the benchmarks. ■