The ETF Portfolio Strategist: 08 SEP 2024

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Globally diversified portfolio strategies retreated for a second week, based on a set of asset allocation ETFs. The downturn still looks like a garden-variety correction in the normal ebb and flow of trading, but the backdrop chatter about recession is becoming louder.

There’s still room for debate about whether the US economy is rolling over vs. stabilizing at a softer growth rate. The outcome of this debate, which will become clearer over the next few weeks, will determine if the latest market downturn is noise in an otherwise ongoing bull trend or the start of deeper trouble.

What we do know is that the red-hot upside momentum that’s prevailed for various flavors of global asset allocation has cooled. The Signal scores for the strategy ETFs shown below fell to 4. That’s still a strong positive reading. The question is whether the pullback of late will persist? See this summary for details on the metrics in the tables.

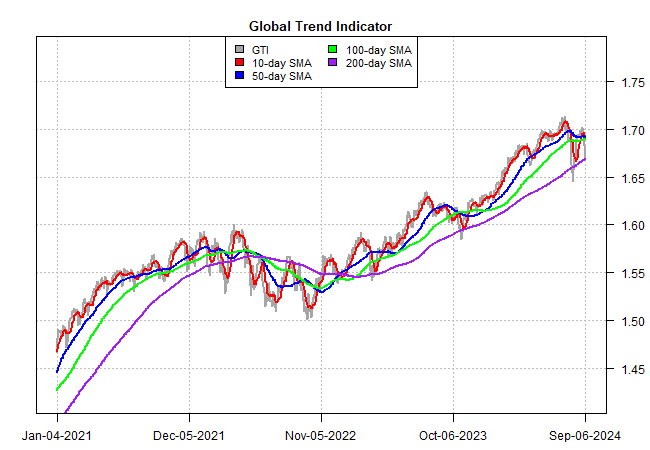

One way to gauge the downside risk potential is with our proprietary Global Trend Indicator, which analyzes and aggregates relative trend behavior for the four asset allocation ETFs listed in the table above. The current profile reflects a switch to short-term weakness via the 10-day average (red line) falling ever so slightly below its 50-day counterpart (blue line). Medium- and long-term investors can ignore this weakness as long as the longer-term metrics continue to trend positive, as they currently do.

But the potential for a deeper warning is lurking via the 50-day GTI average, which is holding just slightly above the 100-day counterpart (green line). If that positive profile gives way, which could occur this week, it would signal a higher-level risk that suggest the recent downturn may run for several weeks. If GTI’s 50-day/100-day trend breaks down, the next tipping point is the 100-day/200-day ratio. If and when that gives way, a prolonged market correction appears likely.

For now, it’s reasonable to reserve judgment on whether the selling over the past two weeks is noise or signal. From a US perspective, all eyes will focus on the labor market to refine thinking on whether the slowdown in hiring is a genuine warning sign for the economy and that a recession, if it hasn’t already started, is imminent.

By some accounts, the fix is in and it’s too late for Fed rate cuts to save the day. By your editor’s reasoning, that view is premature, as I write in this week’s edition of The US Business Cycle Risk Report: “Some indicators are suggesting that economic growth is relatively stable at a moderate pace. Even better, there is new evidence from other corners of the macro toolkit that show the economic trend is firming after the recent downshift.”

The pushback is that the rise in unemployment in recent months is telling. Ditto for the disinversion of the 10-year/2-year US Treasury yield curve following inversion — a change that suggests a recession is at hand, based on the indicator’s track record.

One can argue that the bond market is on board with the shifting outlook for rising recession risk. Note that the strong Signal scores for global markets in the chart below are concentrated in fixed income. US Treasuries (IEF) led last week’s winners and are posting a 6 Signal score, the highest bullish reading. The implication: IEF’s rally has room to run.

Growing confidence that the Fed will cut interest rates next week at the Sep. 18 FOMC meeting sweetens the deal for bonds. This week’s inflation report for August (Wed., Sep. 11) is expected to cooperate with another round of disinflation for headline CPI and unchanged core CPI via the year-over-year comparisons.

Otherwise, the week’s main event is the weekly update on jobless claims. This leading indicator for the labor market still paints a relatively upbeat profile. Economists expect more of the same in Thursday’s release (Sep. 12), namely: new filings for unemployment benefits are projected to hold at a relatively low level.

There’s no denying that hiring is slowing. But in previous recessions, there’s been a clear run higher in jobless claims as payrolls fell. This time, at least so far, there’s a conflict: softer hiring but without a spike in layoffs.

One explanation is that the macro shocks of the pandemic continue to resonate. Will the reluctance to cut payrolls sharply, rather than just downshift hiring, immunize the economy recession? No one knows. Until there’s deeper clarity via the incoming data, equities will continue to flirt (without fully embracing) a risk-off signal while bonds do the same in reverse: flirt with risk-on after suffering through several years of risk-off.

All of which inspires your editor to shift modestly away from equities and pick up the slack in bonds, perhaps with real estate investment trusts (VNQ) too. That’s my calculated-risk bias these days.

Markets and the economy are almost certainly knee-deep in a transition phase. The mystery is what exactly we’re transitioning to and when the transition will be clear. ■