The ETF Portfolio Strategist: 09 JUL 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

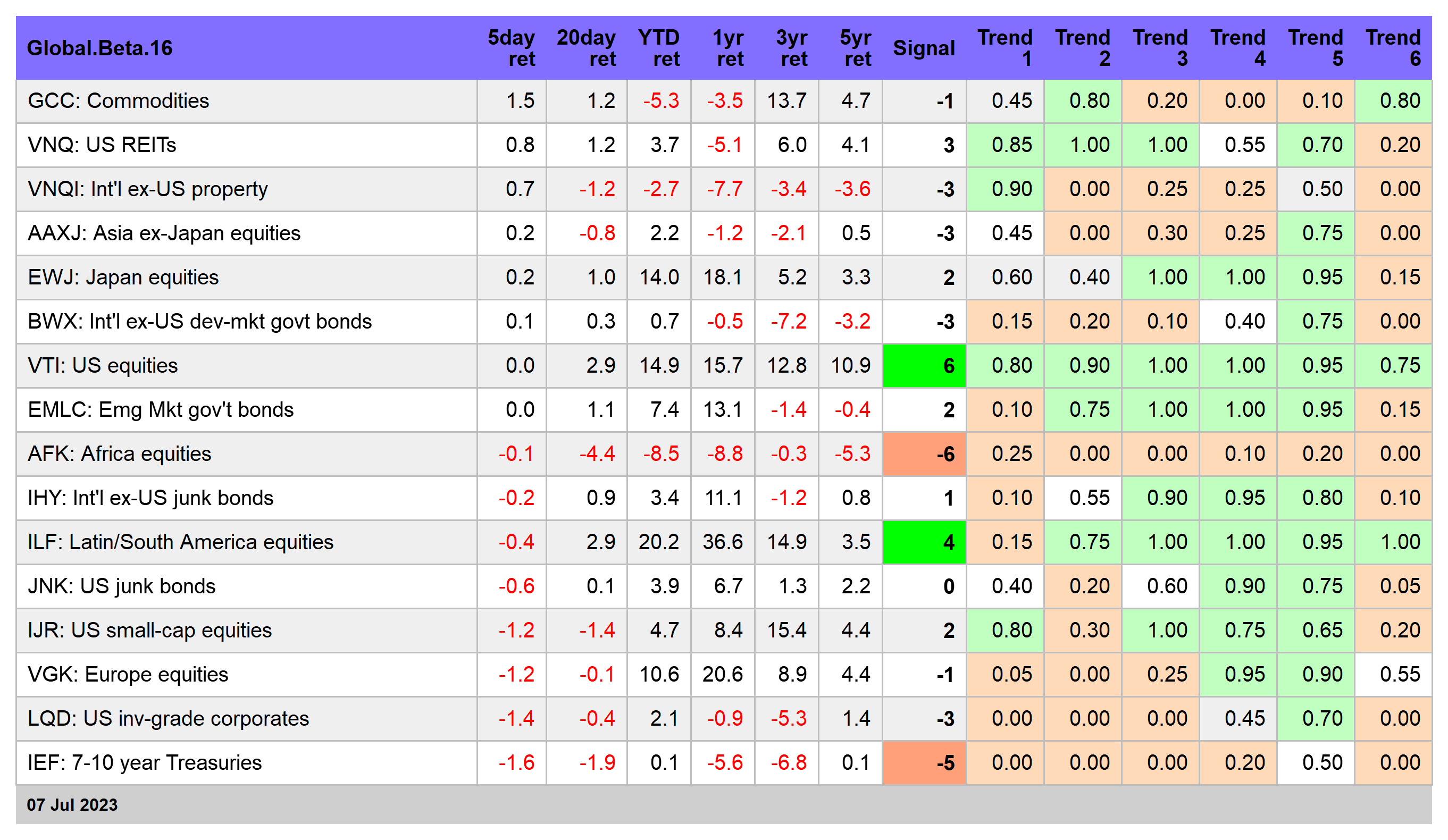

Is it a pause or a top? I’m inclined to go with the former, although my confidence is only moderate at this point. But there are several factors that suggest the bull run for our G.B16 global opportunity set that started in October still has room to run. See this summary for design details on the strategy benchmarks and this summary for how the metrics in the tables below are calculated.

For starters, it’s always encouraging when the price trend is friendly, and on that score there’s still a decent tailwind. That’s obvious in the chart below, which shows G.B16’s 50-day moving average holding well above the 200-day average.

The Signal score for G.B16 is moderately bullish as of Friday’s close, a tick better vs. the previous week.

G.B16 is up a strong 7.1% so far this year, but that’s a bit hot over a 6-month time frame for a multi-asset-class portfolio and so I’m expecting that markets will be digesting gains for a period.

A key driver of the upside bias (still) is US equities. Vanguard Total Stock Market (VTI) was flat over the past five trading days, but the trend still looks bullish. Indeed, VTI’s Signal score of 6 is the strongest by far for the G.B16 opportunity set.

But US shares have rallied too far too fast and so the immediate future probably will deliver flat to modestly negative results. The key to watch is if the deterioration in momentum accelerates. Much will likely depend on how this week’s inflation data stacks up.

The US Consumer Price Index (CPI) is expected to post a solid round of disinflation for the June data (Wed., June 12), based on Econoday.com’s consensus point forecast for the 1-year change. Headline CPI is projected to slow sharply to 3.1% vs. 4.0% in May. Core CPI is also expected to slow, albeit modestly, dipping to 5.0% in June from 5.3% previously. That’s still well above the Fed’s 2% inflation target, but if the forecast is correct the news will strengthen the market’s view that Fed will lift interest rates one more time for the cycle with a 1/4-point hike at the July 26 FOMC meeting. Beyond that, Fed funds futures are pricing in expectations that the central bank will leave rates unchanged for the near term.

If the Fed’s target rate peaks at 5.25%-5.50%, the Treasury market’s bear market be near. It’s still too early to go bottom-fishing with iShares 7-10 Year Treasury Bond ETF (IEF), but if the CPI data cooperates on Wednesday the case will strengthen for risk-tolerant investors to start accumulating shares.

Speaking of bonds, the emerging-markets variety continues to look intriguing. If EMLC can punch above its recent highs — roughly $25.60 — this rally, which has been off the radar for most investors, may be setting the groundwork for a new run higher. A component of the allure: a relatively attractive 5.66% trailing 12-month yield. For comparison, the equivalent for IEF is a relatively paltry 2.45%, according to Morningstar.com.