The ETF Portfolio Strategist: 10 Dec 2021

Portfolio Strategy Benchmarks

Stocks rebound as inflation accelerates

Strong gains for all our strategy benchmarks this week

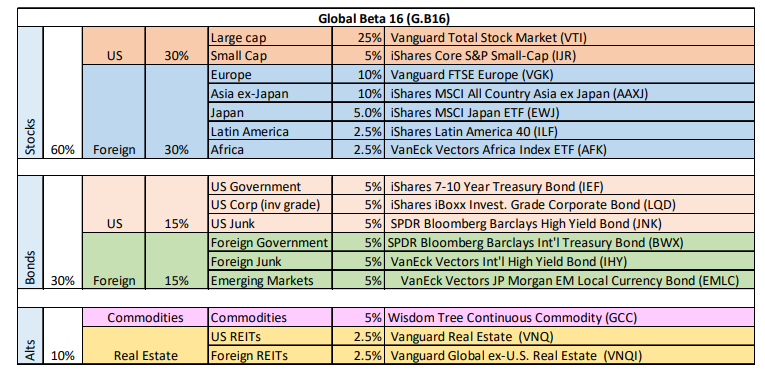

US equities rose for the first time in 5 weeks: After four weekly losses, US shares bounced this week, rising 3.6% — the strongest gain among our 16-fund opportunity set (through Dec. 10), based on Vanguard Total US Stock Market (VTI). The only losers: US bonds. For details on metrics in the table, see this summary.

The rebound in equities comes as US consumer inflation scored it hottest report in nearly four decades. Headline CPI rose 6.8% year over year through November, the Labor Dept. reports. Core CPI, which excludes food and energy (considered a more reliable measure of the trend) accelerated too, advancing 4.9% vs. a year ago — the highest in 30 years.

Are stocks immune to inflation? No, although recent trading activity suggests Mr. Market is reassessing the threat this time. Unless there’s a disconnect between investment sentiment and inflation risk. Maybe, but the alternative view is that the ongoing rise in consumer spending and expectations for the strong rebound in US economic growth in the fourth quarter (which will help drive corporate earnings higher) are inspiring the crowd to look through the hot inflation numbers of late.

But let’s not dismiss risk entirely. The Federal Reserve policy meeting next week will be closely watched for signs, subtle or not, on whether the central bank will accelerate plans to end its bond-buying program and bring forward the start of interest-rate hikes.

What does the Treasury market think? The policy-sensitive 2-year yield is certainly pricing in higher rates. After today’s session, this maturity ended the week at 0.67%, just below a pandemic high.

But the 10-year yield continues to meander in a range, effectively signaling doubts that 1) elevated inflation will be persistent; and 2) the Fed will be able to lift rates more than slightly without creating serious headwinds for the economy.

Then again, let’s see how the bond market next week digests today’s inflation news and the messages, implied or otherwise, in next week’s Fed meeting.

For guidance, consider Fed funds futures, which are pricing in a 2% probability that the central bank lifts rates at next week’s meeting, which rises to 7% for the January meeting, 36% for March and 57% by the time May rolls around, based on CME data.

The main questions for next week: How will these probabilities shift and how will stocks and bonds react? At the moment, markets don’t appear concerned that rate hikes or near, or if they are that there’s more than a modest set of increases around the corner.

One factor that’s likely to keep any policy tightening light for the near term: the reversal in the Treasury market’s 10-year/2-year yield curve, which continues to show a downside bias — and one that’s picked up speed lately. The message here is that the bond market is starting to smell the potential for softer growth in the new year, albeit after a likely ramp-up in Q4 growth. Until/if the yield curve stabilizes (or rise), it’s a factor that suggests any policy tightening will be a mild and brief affair. Indeed, one way to pull inflation lower is by unleashing a recession. That worked for Paul Volcker in the early 1980s, but a repeat performance this time looks unlikely, at least not intentionally so.

The Fed has made its share of policy mistakes in the past. Is a new one lurking? If so, of what type? There are two widely-discussed possibilities making the rounds. First, the Fed has allowed the inflation cat out of the bag and needs to roll out rate hikes to play catch-up. But that inspires some analysts to warn that the Fed might trigger a recession with an overly aggressive round of policy tightening.

Threading this needle isn’t going to be easy, at least not any time soon. That suggests the recent calm in markets could be a lull before a storm.

Strong rebounds for our portfolio-strategy benchmarks: The bounce in risk assets around the world delivered solid gains to multi-asset-class portfolios this week. Leading the charge: a sizzling 2.4% weekly advance for the Global Market Index (GMI), an unmanaged market-value-weighted mix of the major asset classes. See this summary for an overview of benchmark-design rules.

Despite the recoveries this week, the strategy benchmarks have yet to regain recent highs. That may be coming, but as discussed above first there’s the issue of working through inflation risk and the central bank guidance in the week ahead.

“It feels like the market has climbed two walls of worry already: Omicron and the path of the Fed,” says Mona Mahajan, senior investment strategist at Edward Jones. “I do think over the next couple of weeks we will get a little bit more certainty on both fronts.” ■