The ETF Portfolio Strategist: 10 MAR 2024

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Trending behavior for a given directional bias tends to beget more of the same. That, at least, is you editor’s baseline forecast generally, until there’s a compelling reason to change the outlook. History suggests caution in dismissing trend-based forecasts, mainly because doing so has been a losing proposition more often than not. That’s not to say you should be a slave to trend. But neither can you be cavalier in deciding that this time is different.

That worldview sets us up for reviewing where we stand with our usual proxies for asset allocation strategies. The main takeaway: the upside trend remains strong (making mincemeat, still, of our earlier behavioral-driven misgivings). The numbers, however, continue to impress. The iShares Aggressive Allocation ETF (AOA), for example, rose for an seventh straight week.

In fact, all four flavors of risk design for the iShares asset allocation ETFs posted gains last week. And all four funds held on to bullish Signal scores of 5, which is just one notch below the highest-possible reading. See this summary for details on the metrics in the tables below.

Optimists will find even more reason to celebrate in the wake of the conservative asset allocation ETF’s upside breakout to a two-year high. Recall that until recently AOK had not been confirming AOA’s bull run. But with that caveat giving way to the trend, another rationale for doubting the rally has faded.

Reviewing the major components of global markets also offer a diminishing number of reasons to cast aspersions on the party. Except for a handful of holdouts, bullish market sentiment has broadened.

Among the laggards: US Treasuries (IEF). Although this ETF appears to be stabilizing, it’s yet to persuasively break higher and move into the green re: the Signal score. But there are hints that a change in trend is near. After three years-plus of downside trending behavior, IEF is flirting with a rebound, as its moderately positive 3 Signal score suggests.

There’s still room for debate on whether IEF will trend higher in the weeks/months ahead or is merely stabilizing after a grueling bear market for bonds. This much is clear: to the extent that fixed-income is no longer trending down, that’s productive for conservative strategies (such as AOK), which have relatively higher bond weights.

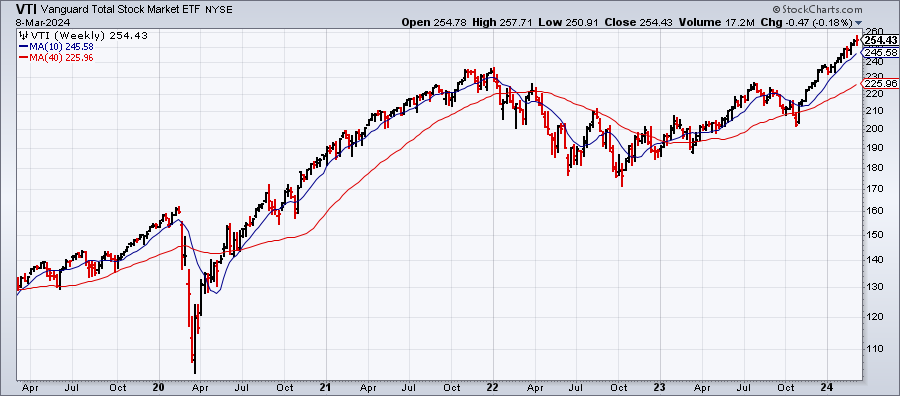

As for staying all-in on a bullish call for risk assets, the strong trend of late certainly lends support. The key question is how long can a bull run last? Alas, there are no easy/reliable answers because history reflects a wide array of results, depending on how you slice and dice. The previous uptrend in US stocks (VTI), for example, ran for almost two years before ending in early 2022. By that standard, the market still has room to run relative to its previous Oct. 2022 trough.

For risk-mind investors, such as yours truly, it’s prudent to keep an eye open for possible spoilers that upend the party. One that appears to be bubbling: emerging signs that the US economy is still slowing, and that the deceleration will run longer and go deeper than generally assumed at the moment.

The crowd has only recently come round to the view that US recession risk is lower than some (many?) analysts advised through much of 2023 into early 2024. Our sister publication — The US Business Cycle Risk Report — has been saying as much since late-spring 2023, based on the data. But in recent weeks the numbers have been increasingly indicating that business-cycle risk post-Q1 is bubbling again.

Once again, that view is out of step with the consensus. The next several weeks may be decisive for deciding if the emerging warning is a genuine signal.

Meantime, the stock market is carefree. When that starts to change (as it one day will), we’ll be looking to Mr. Market for an early warning via a directional change in the trend.