The ETF Portfolio Strategist: 11 Mar 2022

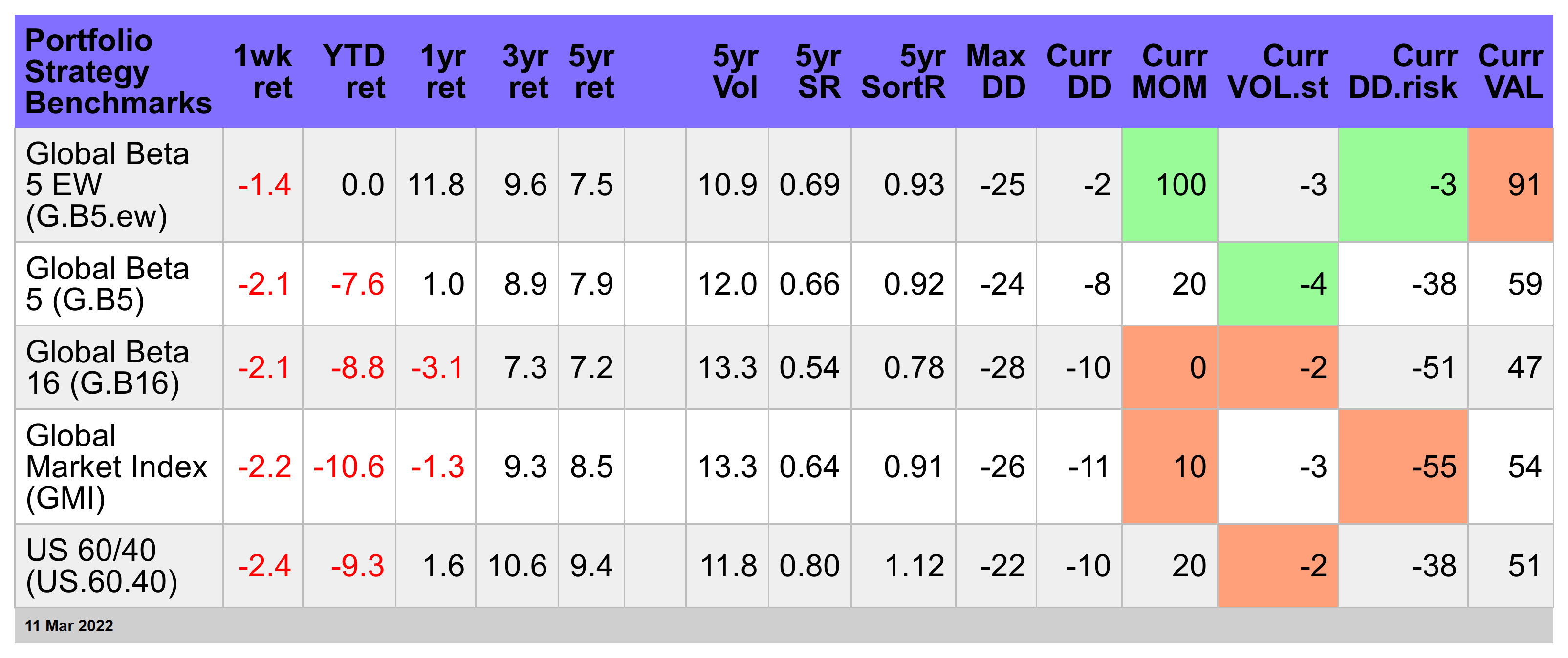

Portfolio Strategy Benchmarks

European shares are the only winner this week for our global opportunity set

Equal weighting the major asset classes continues to generate a performance edge this year.

The search for signal amid the noise is always challenging in financial markets and it’s not getting any easier. The war in Ukraine is tragic on several levels, but as a risk factor in money management it’s noise. Unfortunately, it’s the dominant noise factor and threatens to remain so for the foreseeable future. How then can we assess market action in the short run? With great caution and humility. With that in mind, this week’s only winner for our global opportunity set: shares in Europe, as of Friday’s close (Mar. 11). For details on the metrics in the table below, see this summary.

A casual observer might assume that the markets closest to war, and therefore the most vulnerable to blowback, would suffer the most. A reasonable assumption, but not this week. Vanguard FTSE Europe (VGK) rose 1.3%, posting its first weekly gain since January. What’s the crowd thinking? Early in the European trading day there were relatively upbeat reports citing Russian President Vladimir Putin’s comments — “certain positive developments” — related to talks with Ukraine. As quickly became clear in subsequent updates, however, it was another false dawn and, as I write, the war rages on. Yet the earlier bounce in stocks remained intact to a degree that lifted VGK. But with no convincing sign that Russia’s about to pause its war machine, VGK’s bounce looks to be a temporary deviation in an otherwise risk-off trend.

Elsewhere, global markets fell across the board this week. Even the surging commodities markets, driven by fears of supply shortages brought on by the war, took a break with a touch of red ink. After a week of unsually high volatility — even by the standards for commodities markets — WisdomTree Commodity Index (GCC) eased 0.4%, its first weekly setback since January. When there are genuine signs that the war is ending, or that negotiations worthy of the name are in progress and making some discernible headway, commodities will likely reverse sharply. But amid ongoing reports of relentless bombing of Ukraine, it’s still hard to see anything resembling light at the end of this very dark tunnel.

The near total decline in markets is painful because it’s a reminder that relief was nearly impossible to find by way of conventional risk betas around the world. The conventional ballast of US Treasuries was certainly no help. After a recent bounce, iShares 7-10 Year treasury Bond (IEF) reversed course with a 2.2% slide this week, leaving the ETF close to its lowest level in two years.

Although war on Europe’s eastern border continues to wreak havoc near and far, there’s growing recognition that central banks need to tighten monetary policy. This reality was in sharp relief in the US this week in the wake of yesterday’s update on consumer prices for February, which continued to accelerate to a 7.9% year-on-year pace—a new 40-year high. When you consider that the jump in inflation doesn’t yet reflect the pricing blowback from the war in Ukraine, it’s even clearer that the Federal Reserve needs to raise interest rates no matter how ill-timed such a decision is in the midst of war that’s become a global economic conflict and shock.

The week’s biggest loser: stocks in Asia ex-Japan via iShares MSCI All Country Asia ex Japan (AAXJ), which tumbled 5.4%. The fund’s hefty weighting in China is becoming increasingly risky after the SEC stoked fears this week that the country’s companies listed in America may be forced to delist from US exchanges. “The clock is ticking, and some of the investors have lost patience, and they are leaving this space in the face of uncertainty,” says Bruce Pang, an analyst with China Renaissance Securities in Hong Kong. How do you price in delisting risk? Sell.

AAXJ’s long-running slide has been sending warning signs for months. Along the way, the allure of Asia portfolios ex-China is looking have become ever more compelling. Stripping out direct exposure to the Middle Kingdom has its advantages this year, as suggested by the relatively stable and, more recently, gentle slide in iShares MSCI Emerging Markets ex-China ETF (EMXC).

Red ink dominates the strategy benchmarks. The breadth of decline this week also caught this year’s darling in its snare: Global Beta 5 EW (G.B5.ew), which equally weights the major asset classes on a global basis.

In line with this year’s results, G.B5.ew continued to outperform its counterparts. For the year so far, the strategy is flat. No mean feat in 2022. In fact, more than a few investors would be happy to swap their results with a holding-steady profile. Even better, G.B5.ew’s one-year return — nearly 12% — is a world above its competitors’s results. For details on the benchmark designs, see this summary.

Adopting a strict equal-weighted portfolio mix is probably going too far for most investors. But given this year’s results, moving closer to a quasi-equal weighting will likely be front and center for strategy discussions for the foreseeable future, or at least as long equal-weighting’s relative strength shines brighter than most. ■