The ETF Portfolio Strategist: 11 September 2020

And That Makes Two: US stocks fell for a second straight week, which hasn’t happened since April. The S&P 500 retreated 2.5% for the trading week through today’s close (Sep. 11), which left the index just above its 50-day moving average.

Meanwhile, bond yields continued to inch lower. The benchmark 10-year Treasury yield, for example, ticked down for a second week, slipping to 0.67% (based on daily data via Treasury.gov).

Markets still seem to be in a waiting-for-Godot moment for deeper clarity on the outlook, but no one’s really sure what that moment might be or when it could arrive. A fresh round of bad news on coronavirus? A smoking gun in the US presidential campaign? A game-changing release of a Covid-19 vaccine?

If there’s an ominous twist to this week’s retreat in US equities, it’s not showing up in the so-called fear gauge: the VIX Index eased this week, slipping to the lowest close since Sep. 2. Perhaps it’s the calm before the storm, but so far the selling has (mostly) been a relatively orderly affair.

What could trigger an attitude adjustment for good or ill? Next week’s Fed meeting is a possibility. The crowd’s eager to hear details on the Fed’s plans for monetary policy, which was revised late last month when the central bank announced it was taking a more dovish stance by adopting a looser set of rules for its inflation targeting. But if guidance is the goal, The ETF Portfolio Strategist is expecting that Wednesday’s Fed announcement (Sep. 16) will disappoint by offering minimal details and an abundance of wonkish chatter. Mr. Market, as a result, may have to look elsewhere for inspiration on deciding what comes next.

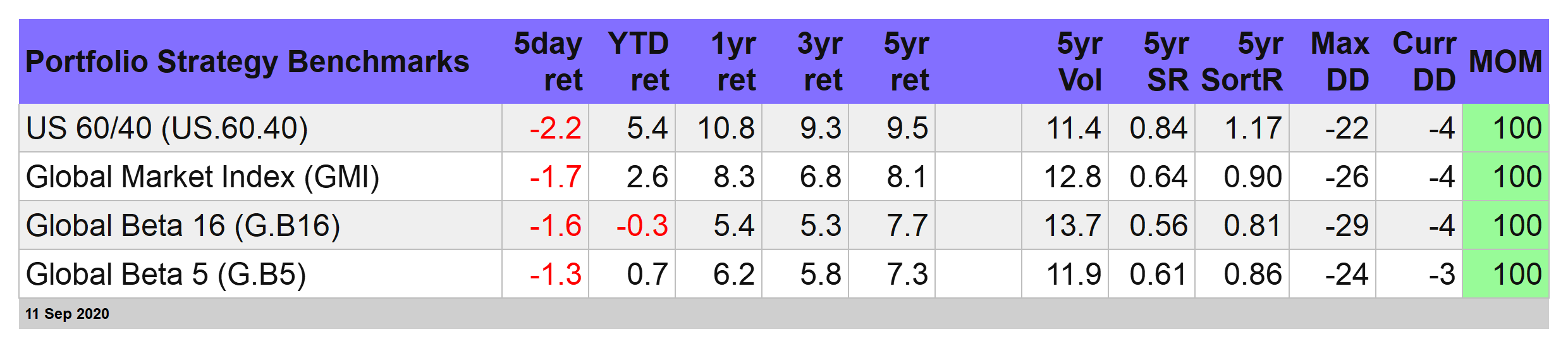

More Red Ink For The Portfolio Strategies: A downside bias continued to weigh on our three proprietary strategies. Global Managed Volatility (G.B16.MVOL) suffered the biggest setback for the week, falling 1.4%. That was a touch better than the 1.6% slide for its benchmark – Global Beta 16 (G.B16), which holds the same 16 funds and is passively managed other than a year-end rebalancing mandate that resets to the target weights. (For details on all the strategies and benchmarks, see this summary.)

This week’s decline was softer for Global Managed Drawdown (G.B16.MDD), which fell a relatively mild 0.6%. Here, too, the same opportunity set of 16 funds applies, but with a distinct strategy of using drawdown signals to manage risk exposure.

G.B16.MDD’s weekly slide was milder than the losses for G.B16.MVOL and the benchmark (G.B16) for an obvious reason: G.B16.MDD has become progressively more defensive in recent weeks – a shift that, so far, has been helpful in recent weeks.

In fact, G.B16.MDD signaled that three new fund positions are slated to shift to cash: ILF, IHY and VNQ, which target Latin American equities, foreign high-yield bonds and US real estate investment trusts, respectively. When these sell signals are executed at Monday’s open, G.B16.MDD will have six of its 16 risk fund allocations in the risk-off cash proxy (SHV).

G.B16.MVOL, by contrast, remains fully invested across its 16 funds that cover the waterfront for the major asset classes. The reason: return volatility has yet to rise enough to trigger sell signal in any corner of the portfolio.

It’s clear that G.B16.MDD and G.B16.MVOL are complimentary in terms of risk management biases of late. Deciding which one will be right (or wrong) in the months and year ahead is, alas, beyond our capacity since the future is as uncertain as ever.

What we do know is that on both fronts risk management has paid off year to date: both strategies are well ahead of their benchmark, G.B16, which is slightly under water so far in 2020.

Note that G.B16.MVOL, which still holds a full boat of risk exposure, is slightly ahead of G.B16.MDD this year. Impressive, although there’s a little voice whispering in The ETF Portfolio Strategist’s ear that a stress test is waiting in the wings before the curtain closes on 2020.

Asset Allocation Funds Take A Mild Hit: Finally, here’s how BlackRock’s four asset allocation ETFs compare.

Here, too, there was red ink for the week just ended, ranging from a 0.7% drop to a 1.3% slide. That’s a respectable performance given the downside bias of late for beta. Note, however, that the year-to-date results for the four BlackRock funds are middling relative to our benchmarks and well below performances for two of our proprietary strategies. That’s a reminder that conventional asset allocation strategies continue to find 2020 to be a difficult year for the usual routine. For what it’s worth, your editor expects more of the same will prevail for the near term. ■