The ETF Portfolio Strategist: 12 Feb 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Most global markets sold off last week, taking a toll on the previously upbeat trend indicators highlighted on these pages recently. The reversal in bullish signals is probably a warning that it’s still early to confidently assume that a strong upside bias has taken root.

To be fair, it’s not obvious that this year’s rebound is set to fade either. In other words, I’m now in the neutral camp, but cautiously so as I continue to consider if the bounce is a bear market rally or not.

On the plus side, our global 16-fund opportunity set is holding above its 200-day average, which suggests that upside momentum is still bubbling. Last week’s pullback doesn’t change the profile, but the mixed economic data for the US and elsewhere continue to suggest there may be another shoe to drop.

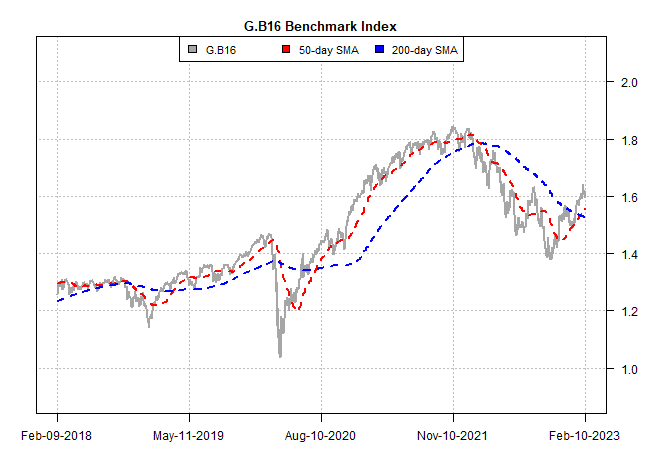

What is clear is that all our strategy benchmarks are posting solid year-to-date gains. See this summary for design details on the strategy benchmarks. G.B16’s 5.6% rally so far this year certainly compares favorably after 2022’s sharp loss. But it’s still not obvious that the recovery is on sound footing and that we’ve seen the lows for this cycle.

The days and weeks ahead may shred our lingering skepticism, but we continue to gravitate toward an all-out bullish posture reluctantly, slowly and cautiously. That view comes with a specific set of caveats, namely: our wary approach will be late to the start of the next bull run, but in the current environment that’s more appealing than being early. In other words, the ever-present risk that the bear market may reappear keeps us humble this time around.

Meanwhile, commodities are last week’s upside outliers for the G.B16 opportunity set. For details on how the metrics in the tables above and below are calculated, see this summary.

But while the equal-weighted WisdomTree Commodity ETF (GCC) was the clear winner last week, the fund remains caught in a tight trading range and so the latest pop is probably noise.

Meanwhile, US small-cap stocks, although they took a hit last week, remain on the short list for markets that appear well-positioned to take advantage of new bull run… assuming one is emerging anew. The iShares Core S&P Small Cap ETF (IJR) still enjoys an upside bias that appears set to persist. Note that IJR still posts the strongest bullish signals for the G.B16 opportunity set via our proprietary trend analytics per the table immediately above. If the fund can close and hold decisively its previous high from last August, the bullish aura for these stocks will strengthen.

US equities overall are looking relatively strong, even after last week’s setback. Vanguard Total Stocks Market ETF (VTI) is second only to small caps (IJR) in terms of bullish readings for our Signal score shown above. Nonetheless, VTI’s recovery is weaker relative to IJR’s. Until/if that changes, IJR’s upside may be limited without broader, firmer support from US equities beta.

But for the moment, sentiment on both fronts appears neutral at worst. Let’s see if the week ahead changes the outlook. ■