The ETF Portfolio Strategist: 13 AUG 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Global markets continued to slide last week for the most part, which isn’t especially surprising, as we’ve been discussing in recent weeks. As noted in the July 23 edition of the newsletter, “The rally of late that’s fired up prices has probably gone too far too fast…”

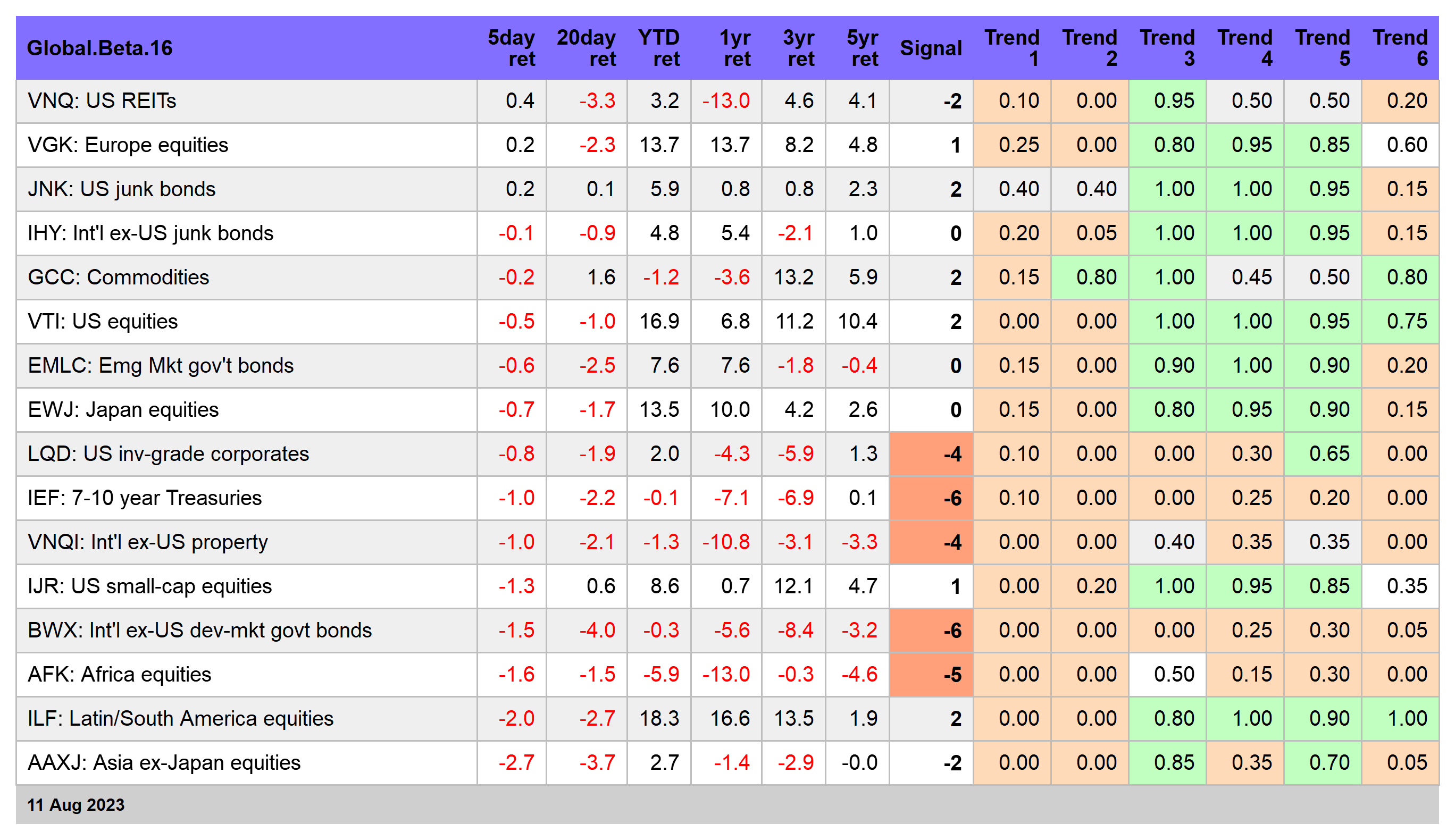

Some of the froth of the spring/summer has evaporated but it’s not yet clear that the pullback has run its course. Our G.B16 benchmark of global assets is now hovering just above its 50-day average. If the index falls below that average, it’ll mark the first dip below that mark in several months. In that case, it could signal that markets will be trading in a range, or worse, for an extended period. A deeper wound for the outlook, however, is still nowhere on the horizon, i.e., G.B16’s 50-day average falling below its 200-day average. See this summary for design details on the strategy benchmarks and this summary for how the metrics in the tables below are calculated.

For the moment, it’s reasonable to assume that markets will be backing and filling for the near term. One reason is a growing sense that China’s economy is facing stronger headwinds than recently anticipated. In turn, the diminished outlook has downside implications for the global economic expansion.

Notably, recent economic numbers for China highlight the growing risk of disinflation/deflation. “Before the pandemic, China was growing at about 6%, and now it's struggling to recover,” says David Dollar, a senior fellow at the Brookings Institute's China center. “Consumption really didn't hold up coming out of the lockdown. The main components of GDP on the demand side — consumption, investment, net exports — they all have serious problems right now.”

Despite recent efforts in the West at decoupling from China, the country still casts a long shadow for the ebb an flow of global economic activity. “The slowdown in China is definitely going to weigh on the global economic outlook,” predicts Larry Hu, Hong Kong-based chief China economist for Macquarie. “Because China is now the No. 1 commodity consumer in the world, the impact is going to be pretty, pretty big.”

If so, the blowback isn’t showing up in America, at least not yet. The US economy is still on track to expand in the near term, according to a recent nowcast of third-quarter GDP. In fact, the Atlanta Fed’s GDPNow model is currently estimating that growth will accelerate sharply to 4.1% from 2.4% in Q2. It’s still too early in the quarter to take this estimate seriously, but it’s a sign that recession appears to be a low-probability risk for the near term.

The challenge for markets is deciphering how the current narratives of a slowing China and a resilient US translate into pricing of risk assets and the course of interest rates. Until there’s more confidence and clarity about how the conflicting trends in the US and China play out, the recent caution in markets seems likely to roll on.

Keep in mind that if the US stock market simply flatlined through the end of year it would post a sizzling 16.9% return for 2023. The question in the days and weeks ahead is one of deciding if that strong performance is still justified? The crowd’s reaction at the moment is straight out of an old Jack Benny sketch: “I’m thinking it over.”