The ETF Portfolio Strategist: 13 Nov 2022

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

As market rebounds go, last week’s gains stack up as one of the stronger bounces in recent history. It wasn’t a clean sweep of recovery, but most markets rallied sharply.

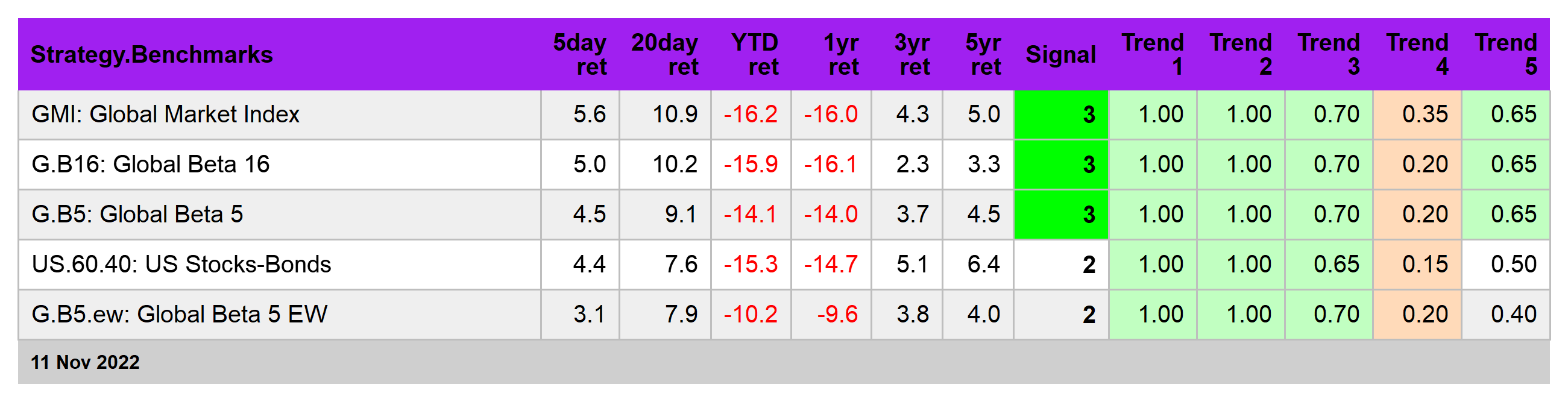

The latest gains flipped our Signal score to green (strong bull readings) for half of the markets in our global 16-fund opportunity set. For details on the Signal methodology, see this summary. Encouraging, but let’s see if the revival of bullish scores persists. Meantime, I remain defensive on the outlook for risk.

But perhaps we’re at a turning point. The poster boy du jour for considering the idea: stocks in Europe. Vanguard FTSE Europe (VGK) surged 8.3% last week, extending its recovery to a four-week run. We may have seen the bottom, but there’s still reason to reserve judgment on whether a durable rally has started. The ongoing Ukraine war is (still) the elephant in the room. With winter approaching and energy-related risk sky-high for the Continent, the potential for macro-related trouble is, at best, in remission and will remain so as long as the conflict continues.

The third-best performer last week: stocks in Japan. The iShares MSCI Japan ETF (EWJ) soared 8.0%, but here too it’s open for debate if this this bear market has run out of road. The downside bias has faded in recent weeks, but the primary trend still looks bearish.

Respecting the trend is still our recommendation for US stocks, too. Although Vanguard Total US Stock Market (VTI) rose to its highest close in two months, it’s premature to conclude that the negative bias has faded.

The same is true for US Treasuries. Last week brought relief to iShares 7-10 Year Treasury Bond ETF (IEF), but the best you can say for the fund is that it’s forming a bottom… maybe.

Until there’s more support for thinking that interest rates have peaked, staying cautious on bonds is still warranted. The softer-than-expected inflation report for October may be a sign that the worst has passed for fixed income, but for the moment the optimistic outlook is that the Federal Reserve will slow (rather than pause) its rate hikes rather. Fed funds futures are pricing in a near certainty of another hike at the next FOMC meeting on Dec. 14. The crowd expects a softer hike of 50 basis points this time rather than 75. Perhaps the central bank will pause after this next increase, a scenario for 2023 that the bond market is increasingly anticipating. Much depends on how the inflation report for November stacks up. Buying bonds at this point is effectively a bet that pricing pressure will continue to fade this month. Plausible, perhaps even likely, but that’s a bet we’re not yet willing to take.

Our global strategy benchmarks posted strong recoveries last week, led by the Global Market Index (GMI), which holds all the major asset classes weighted by market values. See this summary for design details on the benchmarks. This could be the start of a new bull market, but I’m still skeptical. One reason: the US economic outlook still looks dicey, as explained in today’s issue of The US Business Cycle Risk Report.

Markets may be anticipating that the selling wave of 2022 has ended or is close to ending. I’m no longer dismissing the idea outright, but I’m not ready to dive into that forecast either. That’s a calculated risk and one that may come with an opportunity cost. But I’m still inclined to favor being late than early in the current climate. ■