The ETF Portfolio Strategist: 14 Jul 2022

Trend Watch: US Bonds

The fixed-income markets have taken a bullet this year. Even worse, bonds have lost altitude at the same time that stocks have suffered. The core of the asset allocation paradigm, in short, is being stress tested in no small degree. But there are signs that the rout for bonds is easing. But is it reversing? Maybe, but it’s too soon to develop a high-confidence forecast. That said, there are some subtle hints that the tide may be turning.

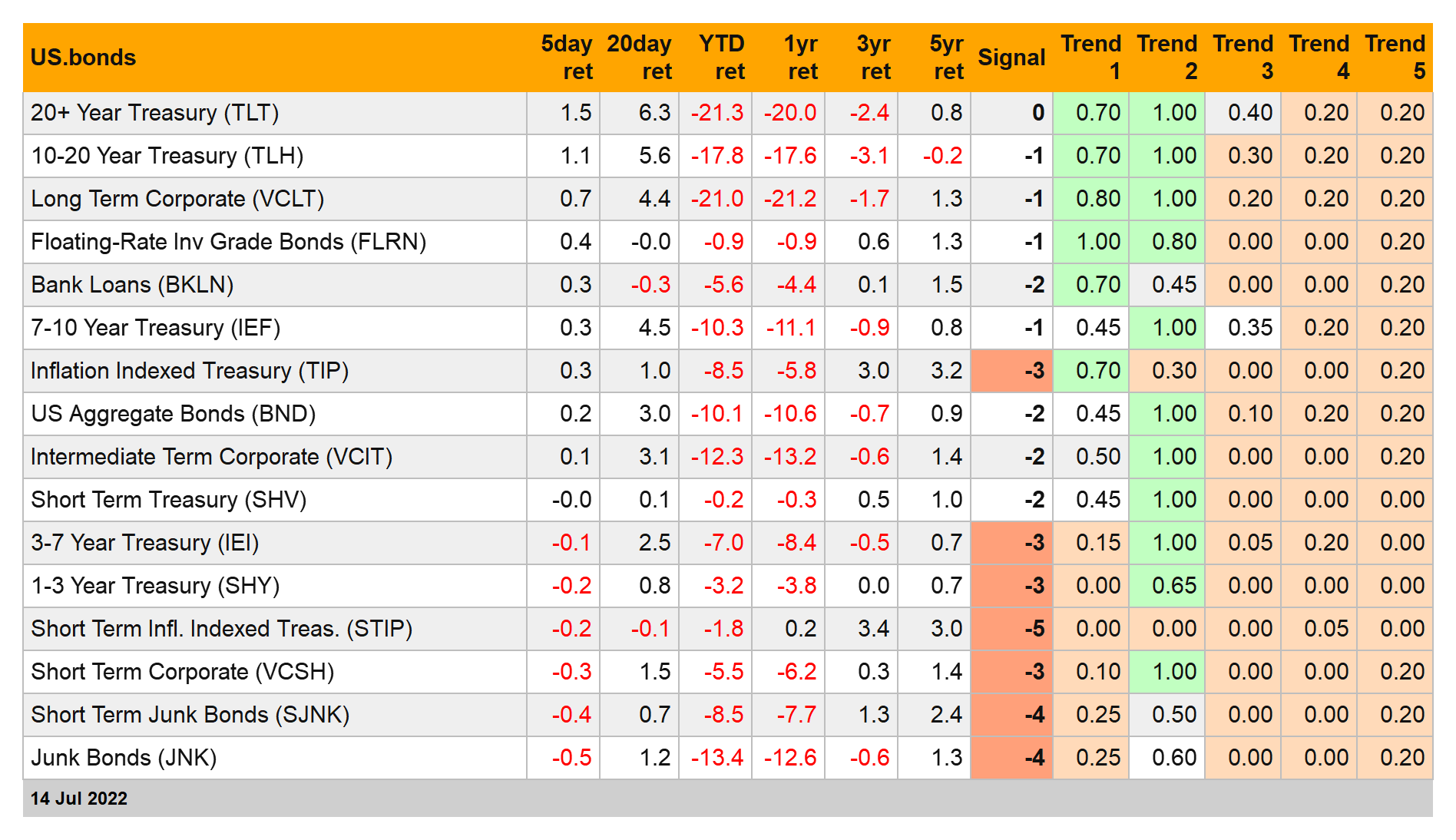

The first stop on the short list to monitor: long-term Treasuries via iShares 20+ Year Treasury Bond ETF (TLT). The fund currently ranks highest via our proprietary trend analytics with a score of 0. That’s still far from a buy signal, but amid a basket of dirty laundry it’s the cleanest shirt in the bunch. (See the Signal column in the chart below, which is ranked by 5-day return; for details on the scoring methodology, see this summary.)

Looking at TLT’s weekly price chart through today’s close shows a bit of a bounce of late. But a 0 trend score isn’t enough to convince us that better days are immediately ahead for TLT. The Federal Reserve, after all, is still committed to raising interest rates and Fed funds futures are pricing in relatively aggressive hikes for the next several meetings.

When we see TLT’s Trend 3 and Trend 4 boxes turn to green in the table above (assuming Trend 1 and Trend 2 stay green) the outlook will look considerably brighter. Indeed, the same can be said for most bond ETFs in the table above. Most are posting green for the short-term Trend 1 and Trend 2 columns. That may be an early sign of a rebound brewing… or not. Meantime, we’re waiting to see when/if more columns tick green.

For now, the bond market continues to struggle with pricing two conflicting risk factors: rising interest rates/high inflation vs. recession risk. The former may be (probably will be) a key factor that triggers the latter, but not yet. And so the crowd seems to be on the fence about which risk factor will have the upper hand in the immediate future.

Until recently, rising rates/inflation have been driving pricing, which means that bond prices have declined. Is that about to change? If recession risk continues to rise and becomes the dominating risk factor for the bond market, prices will likely start trending higher for some period of time. That will signal a sentiment shift in that investors will see bonds are beneficiaries of economic growth worries, which in turn will revive the perception of bonds (Treasuries in particular) as safe havens for waiting out recessionary troubles.

The complicating factor is that while the US economy is weakening, it’s not yet clear that it’s weakening enough to trigger a recession in the immediate future. As a result, there’s still plenty of doubt about how/when/if to see bonds/Treasuries as timely buys for an approaching recession. For the moment, there’s room for debate (and, no, forecasting a recession for 2023 doesn’t really count for much since there are too many moving pieces between now and next year).

For the near term, the bond market is betwixt and between on the matter of how to price in rising rates/inflation risk vs. recession risk. Clarity is coming, and when it arrives it’ll be easier to argue that the near-term direction for the bond market is bullish or not. Meantime, we remain defensive on fixed income until the numbers give a reason to think otherwise. ■