The ETF Portfolio Strategist: 14 Nov 2021

Proprietary Strategies

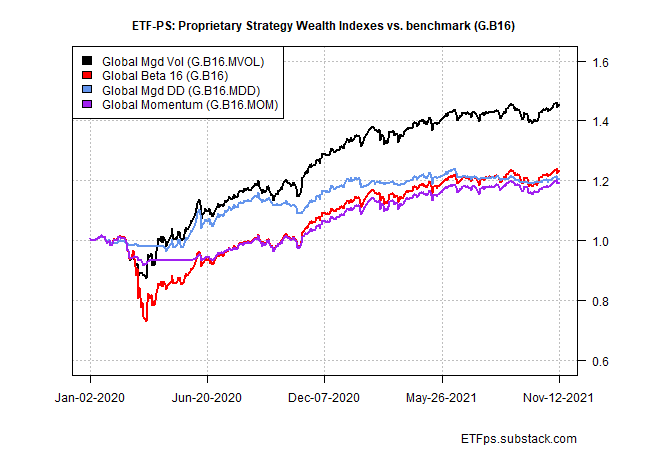

Global Managed Volatility (G.B16.MVOL), the best performer this year among our proprietary strategies, switched to a risk-off position for two slices of the bond market at Friday’s close (Nov. 12). One of the new risk-off signals is for medium-term US Treasuries (IEF). The change is conspicuous because it’s only one of two risk-off positions for the strategy (the other is international junk bonds via IHY). Otherwise, G.B16.MVOL is risk-on for the remainder of its 16-fund portfolio strategy. For details on the strategy rules and metrics in the tables below, see this summary.

This is the first time that G.B16.MVOL has issued a risk-off signal for IEF since March. Is this an early clue for expecting IEF’s recent weakness to accelerate? If so, it wouldn’t be a huge shock: IEF’s downside trend has revived in recent weeks following a rally earlier in the year.

Otherwise, all three of our prop strategies lost ground last week, in line with the benchmark’s setback: Global Beta 16 (G.B16), which passively holds all 16 funds in the opportunity set (see last table below), dipped 0.1% for the week just passed. G.B16.MVOL matched the loss, while the other two prop strategies posted deeper weekly setbacks.

Since 2020’s start, G.B16.MVOL has been the clear-away performance leader vs. the other prop strategies and the benchmark. That leadership has faded in 2021, however, largely because any degree of risk management has been a headwind this year.

By contrast, G.B16’s passive always-full-on risk exposure to the opportunity set has been tough to beat. Whether that turns out to be a repeat performance in 2022 is open for debate as various risk factors churn on the macro horizon — including elevated inflation that’s proving to be more persistent than previously expected.

Meantime, know-nothing, flat-out risk-on remains a winning formula. The red-hot MOM score for G.B16 (see table above) suggests that the index will close out the year with its performance edge intact. ■