The ETF Portfolio Strategist: 15 Apr 2022

Portfolio Strategy Benchmarks

Commodities keep winning while most other markets continue to slide

US small-cap stocks are still trading in a tight range

Equal weighting a globally diversified multi-asset-class portfolio remains a winning strategy this year

A mercifully short week splashes more red ink across most global markets. The Good Friday holiday probably spared Mr. Market what would have been even deeper losses. Even so, there was no shortage of sliding prices for the trading week yesterday’s close (Thursday, Apr. 14).

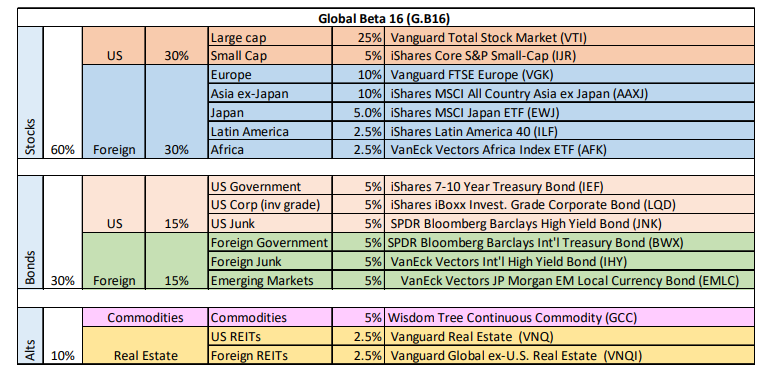

Our 16-fund opportunity set that spans global markets was once again (mostly) overwhelmed with selling. There were also a handful of gains, but those were the outliers by far. For details on the metrics in the table below, see this summary.

The winner once more: commodities. WisdomTree Commodity Index (GCC) rose 3.2% this week, providing fresh support for assuming that prices of raw materials are still in an upswing. A key factor that’s driving prices higher is pinched supply. “Inventories across energy, agricultural and metals are critically low everywhere,” advises Tracey Allen, commodities strategist at JPMorgan Chase.

Softer demand may starting offsetting the impact of tight supplies, if economic growth slows enough, perhaps to the point of a tipping into a new recession, as some analysts predict. But for the moment, overall demand is still relatively strong, or at least strong enough to have minimal effect on the supply contraints. As a result, a potent tailwind is (still) blowing in the commodities space.

Small-cap US stocks edged up this week, but a look at the chart for iShares Core S&P Small-Cap (IJR) suggests the ETF remains firmly in the grip of a holding pattern with a slight downside bias. In short, not much to see here.

A similar story applies to the only other winner this week: shares in Africa via VanEck Vectors Africa (AFK), which edged up 0.4%.

The rest of the field lost ground this week, including US stocks (VTI) and US Treasuries (IEF). With the exception of Latin America stocks (ILF) — and possibly US real estate investment trusts (VNQ) — most of this week’s losers also look weak on a longer-term basis. Consider, for instance, this week’s biggest loser: Asia stocks ex-Japan (AAXJ). Gravitiy continues to tell us to stay away.

The advantages of equal-weighting a globally diversified multi-asset-class portfolio continue to shine. Yes, a big chunk of the shining is linked to the equal weighting of commodities (GCC), which tend to be minimized if not overlooked entirely in conventional portfolio strategies. But as our equal-weighted portfolio-strategy index reminds this year, overlooking raw materials can impose a hefty price tag at times. For details on the benchmark designs, see this summary.

We are, of course, in one of those time periods. Global Beta 5 EW (G.B5.ew) rose 0.3% this week (the only portfolio strategy in our wheelhouse with a gain) and is up 1.8% for the year (vs. losses elsewhere). ■