The ETF Portfolio Strategist: 15 Jan 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Markets are becoming more optimistic, but just when it looked safe(r) to start edging back into risk-on mode a new macro risk has emerged. Re-emerged would be more accurate, courtesy of the potential for another crisis of confidence over the US government’s decision to raise its debt limit. We’ll get to that shortly. But first, the good news.

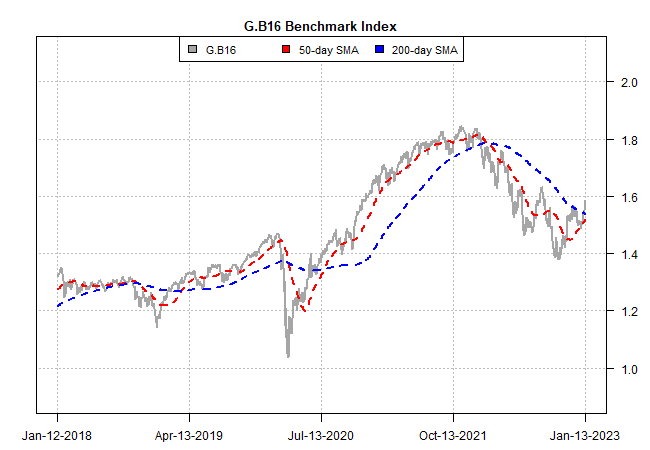

The broad sweep of our 16-fund global opportunity set, via the G.B16 benchmark, rose last week, punching decisively above its 200-day moving average for the first time in a year (there was a brief, fractional rise above this average in late-November/early December, but that turned out to be noise). It’s premature to see this as the start of a new risk-on period for multi-asset-class portfolios, but thinking that a signal change may be brewing is an intriguing possibility that, as of Friday’s close, looks plausible — more so than at any time since the bear market for bonds and stocks started a year ago. For details on G.B16 and other benchmarks cited below, see this summary

Drilling down into G.B16’s components highlights a revival in bullish readings, based on the Signal score. As shown in the table below, nearly all the ETFs held in G.B16 are posting bullish momentum profiles, which extends the broad, upward shift in the directional bias that started in the previous week. I’m reluctant to ring the all-clear bell, based on the data, but it’s possible that we’re looking at an early signal that moves the needle from risk-off to neutral, which in turn may soon lead to a high confidence risk-on signal. The next few weeks could be decisive on this front.

But while it looks safe(r) to go swimming in risky waters again, a new monster is emerging from the deep. This time it’s the debt-ceiling beast, which may be in the early stages of bedeviling markets anew.

On Friday, Treasury Secretary Janet Yellen warned that the US is on track to reach its ~$31 trillion borrowing limit at the end of this week. “Failure to meet the government’s obligations would cause irreparable harm to the US economy, the livelihoods of all Americans, and global financial stability,” she wrote in a letter to the new Republican House Speaker Kevin McCarthy. “I respectfully urge Congress to act promptly to protect the full faith and credit of the United States.”

The risk is that the hyper-partisan politics that now dominate Congress will create conditions that prevent a timely solution. As the chief economist at Moody’s Analytics notes: “The Treasury debt limit is suddenly a serious threat to optimism we can avoid recession this year. Unless lawmakers increase, suspend, or eliminate the limit, Treasury won’t have the cash to pay all its bills on time later this year. Financial markets and the economy will crater.”

Or to cite a more authoritative source on reversals that go bad:

Forecasting the odds of macro blowback that’s solely a function of political risk — perhaps determined by the votes of a handful of House members — is notoriously tricky. All the more so given the circus in Washington of late. Bottom line: it’s naive to discount the potential for extreme outcomes.

Until further notice, this risk factor will increasingly move to the fore for markets until a resolution arrives. Exactly how and when this risk (and its settlement) unfolds is anyone’s guess at this point. Meantime, let’s see how US markets fare at this week’s open on Tuesday, Jan. 17 for an initial test of sentiment tolerance (stock and bond markets are closed Monday, Jan. 16 for the Martin Luther King Jr. Day).

Till then, we can ponder the upbeat momentum profiles that now grace all our portfolio strategy benchmarks. The key question: what’s the shelf life for the upturn in the bullish bias? ■