The ETF Portfolio Strategist: 15 Jul 2022

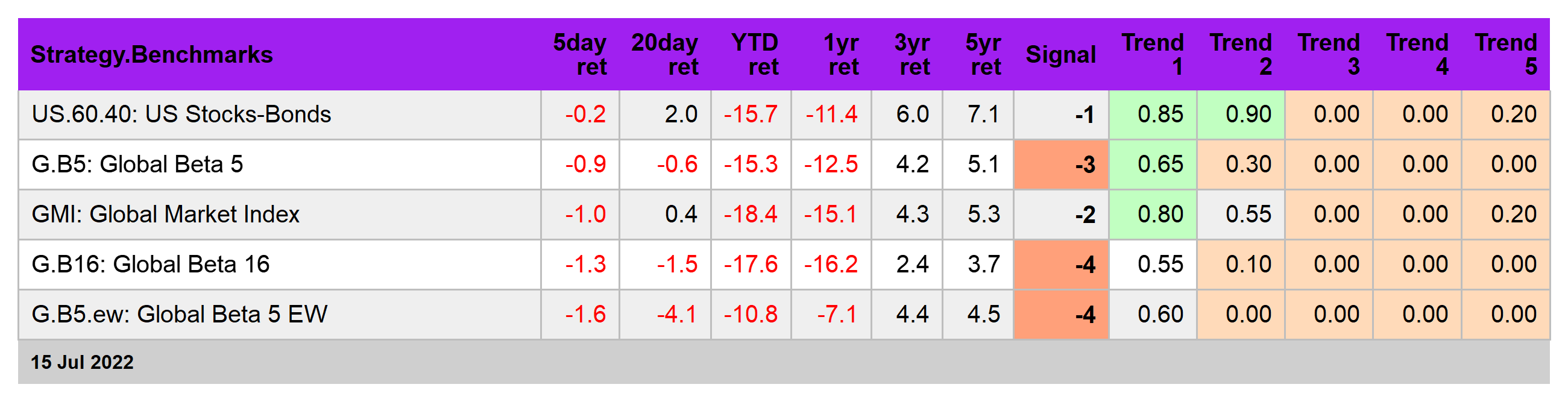

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Bonds are trying to recover, but the bounce this week in some corners of fixed income looks unconvincing.

Consider the best performer this week for our Global Beta 16 opportunity set: US investment-grade corporates (LQD). The 1.3% weekly increase marks the third time in the past four weeks that the ETF has rallied.

But as the chart suggests (supported by the Trend score in the table below), LQD’s a long way from signaling that there’s a sustained rally brewing. The best you can say is that the fund is consolidating after an extended correction. (For details on the trend scoring methodology below, see this summary.)

US Treasuries look a bit strong. The iShares 7-10 Year Treasury Bond ETF (IEF) are currently posting the highest Signal score: +1 (see table below). That may turn out to be an early clue the IEF is set to run. But until the Trend 4 data flips green, we remain cautious on the outlook for IEF.

The main headwind for bonds generally (still): the Federal Reserve remains on track to raise interest rates, perhaps by as much as 100 basis points at the July 27 FOMC meeting. Fed funds futures are also pricing in additional rate hikes in the months ahead.

At some point the bond market may be fully convinced that the central bank’s policy tightening will go too far and trigger a recession, which in turn could ignite a new bond rally. By some accounts, the Fed has already crossed that line. But it’s still unclear how soon a recession will start or how deep it will be. There’s also still room to argue that recession risk is low, depending on how you crunch the data. Until there’s deeper clarity, the uncertainty will probably keep the bond market churning in a range for the near term.

In fact, none of the ETFs in the table above are compelling buys. Based on a proprietary trend scoring, the outlook still looks bearish across the board. Bonds are closest to flipping to neutral, but we’re not yet ready to make that call.

Meantime, our portfolio strategy benchmarks continue to indicate more weakness ahead (see this sumary for the strategy benchmark designs). At some point the strong downside bias that weighs on most markets will run out of momentum. But that turning point still doesn’t appear likely for the near-term horizon. In fact, compared with last week’s update, the strategy benchmarks’ momentum profile continues to deteriorate. ■