The ETF Portfolio Strategist: 16 APR 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

The broad trend for risk assets is running higher again. It’s a relatively mild trend, and one that’s arguably beset by a higher-than-usual set of threats. But judging by this year’s trading activity writ large, it’s getting tougher for skeptics such as yours truly to deny the undeniable.

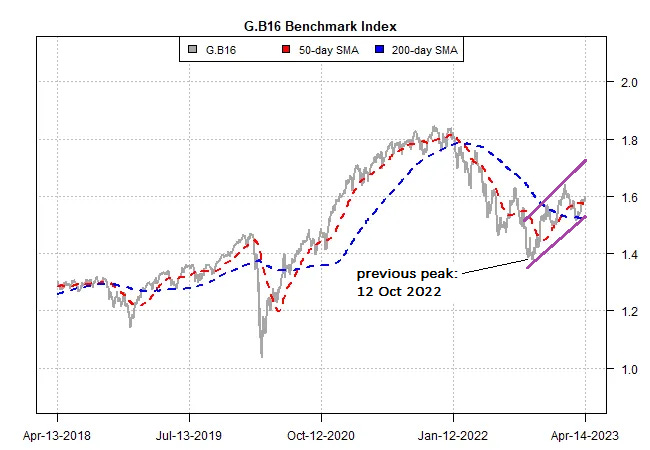

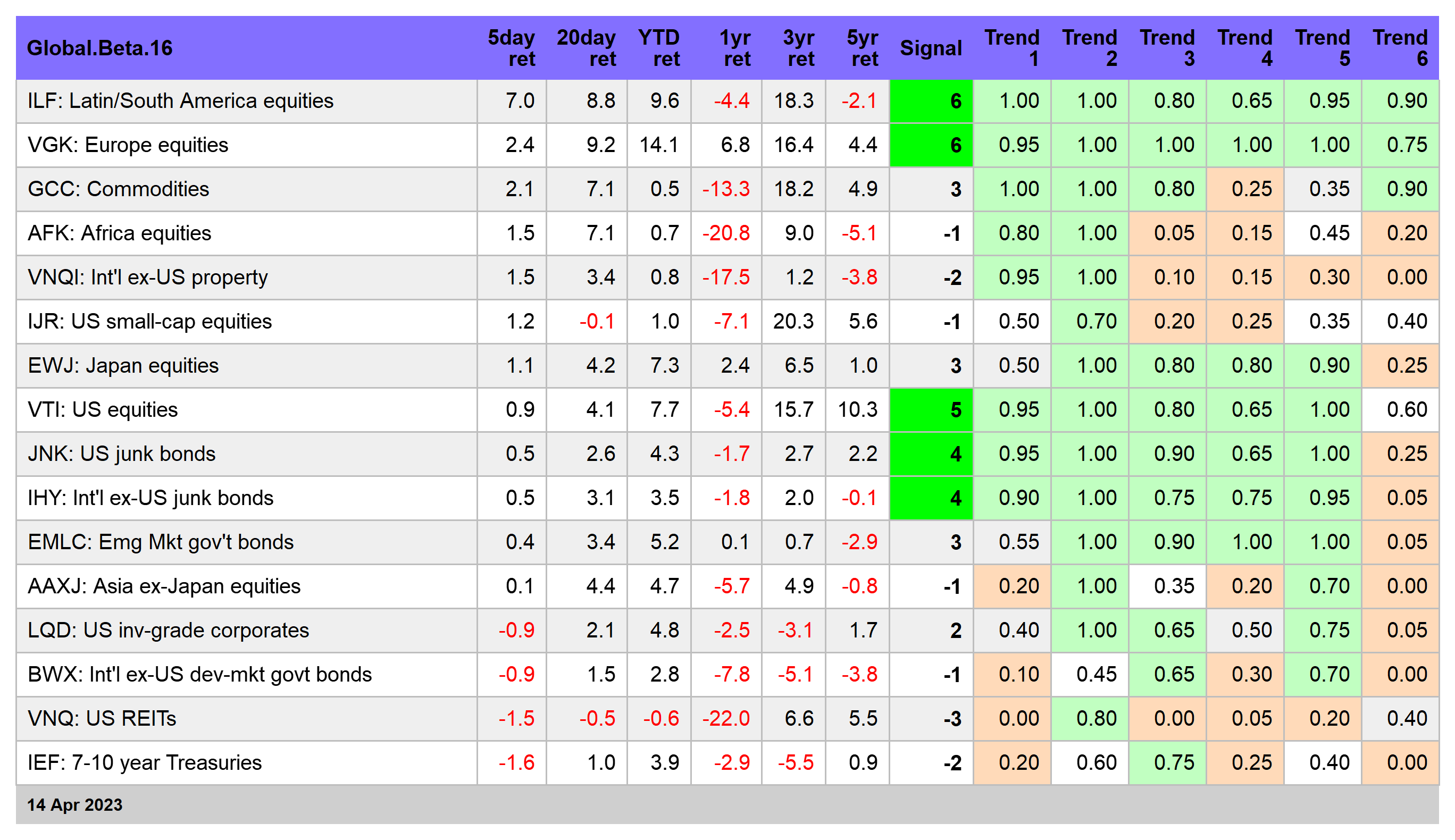

Exhibit A is the run of higher highs and higher lows year to date for a number of multi-asset-class benchmarks. For example, the trend is conspicuous for our homegrown G.B16 index, which tracks our global opportunity set of 16 ETFs. See this summary for design details on the strategy benchmarks.

After bottoming last October, G.B16 has been reviving. There have been two primary pullbacks since the bounce began. In the first case, markets posted a robust rally off the late-December retreat. The animal spirits peaked in early February, but the pullback ended in mid-March at a higher low vs. the late-December trough. So far, so good. But now comes the hard part.

The rally in risk assets that began a month ago is still rolling, or so it appears. A key question is whether there’s enough fuel to push G.B16 and similar benchmarks high enough to take out the previous peak in March and, more importantly, keep the momentum boiling? Here’s where my skepticism emerges on the state and strength of the this years’ re-risking run.

Minds will differ on whether the current rally will endure, but to my mind there are still too many potholes on the tarmac to convince me that a full-throttled takeoff is likely. Yes, I could be wrong, but in the current climate I prefer to be wrong by being late to the party.

If my calculus is misguided, the comeuppance will likely be revealed in the next month or two. The telltale sign of my miscalculation will be G.B16 rallying ~3% from its Friday close and then pushing higher still. Recent momentum suggests that’s plausible, perhaps even likely. The Signal score for G.B16 is moderately bullish at a reading of 3, per the table above, and so no one can rule out this possibility. For details on how the metrics in the tables above and below are calculated, see this summary.

Nonetheless, I’m still in the neutral camp. I don’t expect a new wave of selling (short of news and risk factors that aren’t already widely known). I find it hard to rationalize how markets can further discount a number of more-than-trivial macroeconomic and geopolitical threats swirling in the background.

A trading range, in other words, is my bet for the path of least resistance ahead. Perhaps by the early summer the outlook will evolve for the better. Meantime, the broad rally in global markets that’s unfolded since last October strikes me as a recovery from the darkest points in 2022, when expectations of catastrophe were front and center.

As it turns out, the worst fears weren’t realized, at least not yet. If you’re an optimist, you can argue that the global economy has dodged several bullets relative to the worst-case forecasts. But animal spirits need another feeding and it’s not obvious to this observer that there’s a potent catalyst (or three) waiting in the wings.

Perhaps a pause in rate hikes by the Federal Reserve will suffice. Peace in Ukraine would be a stronger stimulant, as would a discernible ratching down of US-China tensions and/or signals from Washington that a solution is in the offing for the US debt-ceiling crisis that may come to a head in July. I’m carefully monitoring all these possibilities, and more, but for now I’m (still) not holding my breath. ■