The ETF Portfolio Strategist: 17 DEC 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Programming note: This is the last issue for 2023. We’ll return on Jan. 7, 2024. Happy Holidays!

Last week’s across-the-board rally in global markets dealt another blow to your editor’s cautious outlook for risk assets. The summer high for the iShares Aggressive Allocation ETF (AOA) gave way, leaving the fund’s record high of roughly 70.5 (purple line in chart below) as the final frontier before upside momentum breaks free of the trading range that’s prevailed for much of the past two years. When/if that hurdle falls, the case for defensive postures in portfolio design will collapse, at least from the perspective of using trending behavior.

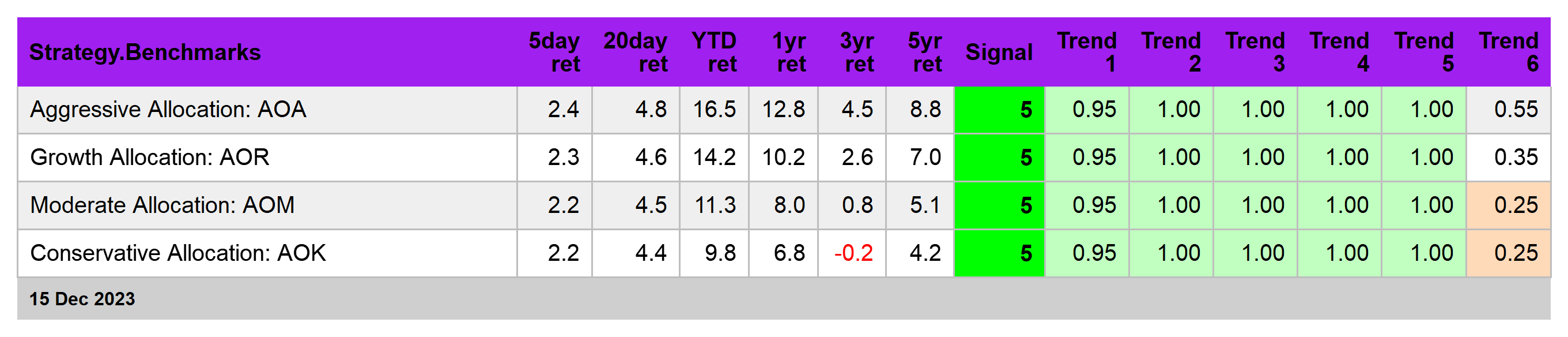

Note that our proprietary Signal score for all four asset allocation ETFs is strong 5 for a third week in a row. Trend alone isn’t a guarantee of the future, but it’s accurate enough of the time to make contrarian bets a hazardous affair. See this summary for details on the data in the tables below.

The full house of 5s in the table above suggest that globally diversified strategies are on track to post new record highs in near term. Ditto for several slices of global markets. US stocks are certainly posting strong results lately. Vanguard Total Stock Market Index Fund (VTI) continues to enjoy a 6 Signal score, the highest bullish reading possible for this indicator. Ditto for iShares Latin America 40 ETF (ILF).

The only markets in the table above that aren’t participating in the party: US Treasuries (IEF), Asia stocks ex-Japan (AAXJ), commodities (GCC) and Africa stocks (AFK). But a rising tide lifts all, or at least most boats, and so it’s unsurprising that even this quartet of laggards has popped recently.

A key catalyst: Rising confidence that the Federal Reserve’s rate hikes are history and rate cuts are near following last week’s dovish news from the central bank’s policy meeting. As Kristina Hooper, chief global markets strategist at Invesco, aptly sums up the revised sentiment bias: “Higher for longer is dead. [Fed Chairman] Powell wrote the epitaph [this week].”

Fed funds futures are pricing in a ~63% probability that Powell and company will cut rates at the March FOMC meeting. That’s a moderate probability, but it’s striking relative to recent history, when rates cuts were thought to be an event that would arrive much later in the year if not in 2025.

Having reset trend expectations, markets must now deliver the goods. Although it’s recently become the consensus view, or very close to it, that markets will soon be setting new highs, failure to do so in due course would deliver a striking counterpoint and a warning sign.

Keep your eye on US stocks as the leading avatar of the new-bull-market crowd. The S&P 500 Index is now less than 2% below its all-time high and topping that peak will further energize already overstimulated animal spirits. An inability to crack that ceiling and, more importantly, hold ground above it would be no less a potent signal.

What might keep markets from seizing higher ground in the weeks ahead? What risk factors might spoil the party? One or more of the following come to mind: Premature assumptions of victory on taming inflation; a reversal of fortunes in highly concentrated tech leadership that’s supporting the stock market indices; surprises on the geopolitical risk front that temper recent oversight masquerading as optimism re: potential blowback; political risk in what promises (threatens) to be an unusually volatile election year for the US in 2024.

The crowd yawns at such worries, and perhaps rightly so. But in a still-risky world where markets are increasingly priced for perfection, the possibility of glitches and defects in assumptions about the morrow aren’t so easily dismissed.