The ETF Portfolio Strategist: 17 Jun 2022

Portfolio Strategy Benchmarks

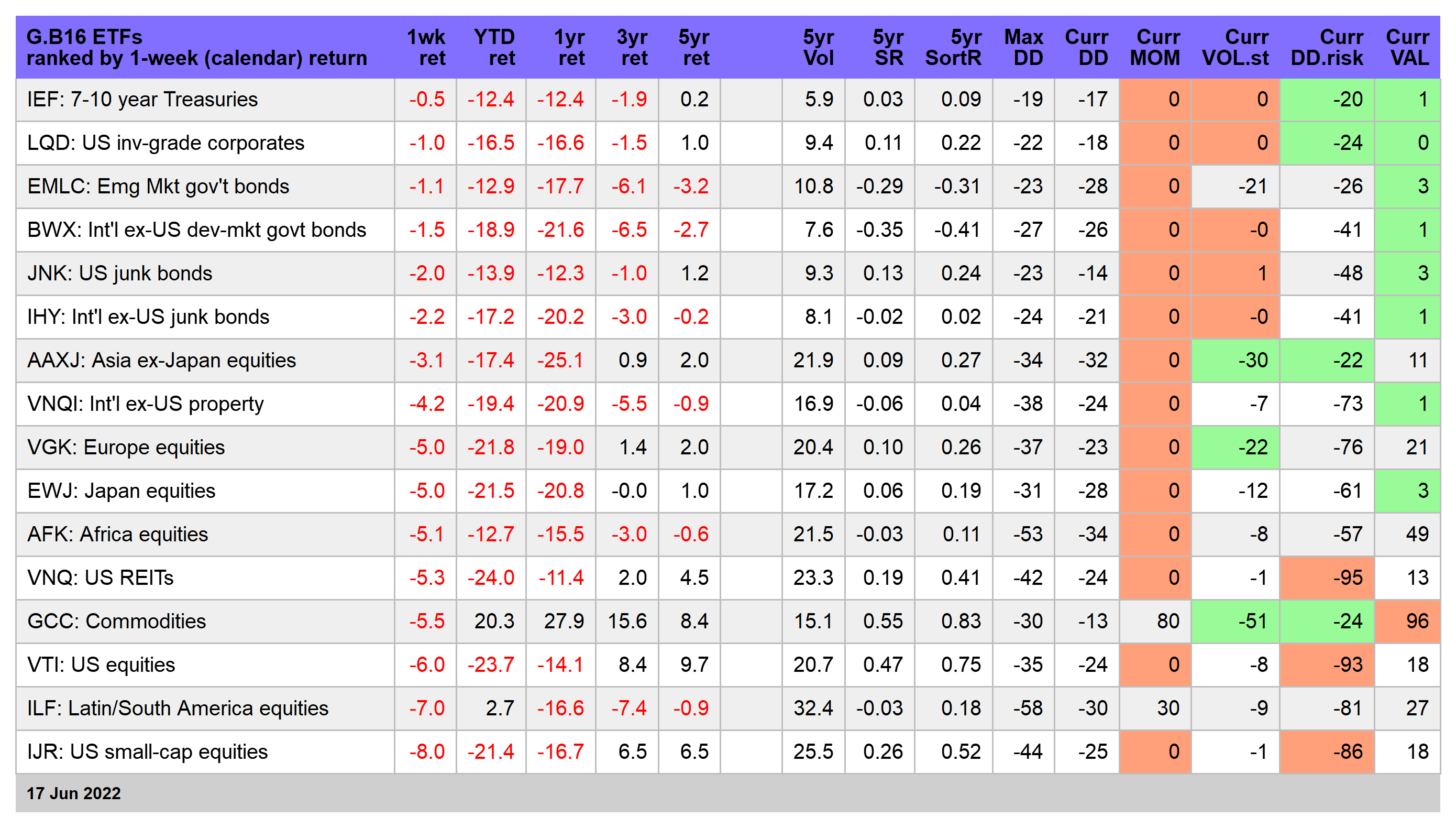

Losses swept across every slice of our 16-fund opportunity set this week

The pain deepens for our strategy benchmarks

Red across the board. It’s not often that every one of our target markets loses ground in a week, but it happens. Ususally there’s at least one outlier, but not this time. In a rough year, this week was the roughest yet, at least in terms of the sweep of red ink.

Yes, there were rallies in some assets on Friday, but from a weekly perspective the trends still look bearish. Most markets around the world have been struggling for much of the year and this week’s trading suggests that digging out of this hole will take time.

The main issues of uncertainty should familar at this late date: investors are still trying to digest how rising interest rates, high inflation and elevated geopolitical risk vis-a-vis the war in Ukraine will influence risk appetites and economic conditions in the months ahead. For details on the metrics in the table below, see this summary.

Two days after raising interest rates by 3/4 percentage point on Wednesday, the Federal Reserve told Congress in a report today that its “commitment to restoring price stability — which is necessary for sustaining a strong labor market — is unconditional.” Translated: the central bank appears intent to do whatever it takes to reverse the inflation surge of late. Stand back until there are compelling signs that the work is resonating by slowing/reversing pricing pressure.

Meantime, everyone’s pondering how long and how far will rates rise? A key factor is how quick and far the economy slows in response to tighter monetary policy. The forecasts are all over the map, which tells you a lot. Markets, meanwhile, are likely to remain volatile until some degree of clarity arrives.

For now, the bias to sell now and analyze later probably still has room to run. The trend in US stocks certainly remains bearish. Vanguard Total US Stock Market tumbled 6.0% this week. Today’s close reflects the wipeout of more than a year of gains.

Fears of recession are keeping Mr. Market on the defensive. Although the odds for an economic downturn in the immediate future still look low, macro sentiment has turned dark and it’s not obvious that an attitude adjustment is on the horizon.

“I think that we need to work on the basis that the macroeconomic and investment environment will remain potentially very fragile,” advises Christian Nolting, Deutsche Bank’s private bank global chief investment officer. “Recovery will not be simple and, even on the most optimistic assumptions -- for example, on Chinese economic reopening -- issues such as supply-chain disruption will take time to fix.”

Then again, the Treasury market may be starting to price in demand destruction, albeit at a very early stage. Although the benchmark 10-year rate rose for a third straight week, it pulled back in each of the last three days of the week, ending at 3.25%. The theory is that if recession risk is rising (or at least if growth is destined to slow for the forseeable future), demand for safe havens will revive. Maybe, but the Fed is still on track to raise interest rates for the next several meetings and so the battle between these opposing forces will continue to play out.

Don’t underestimate the influence of Fed tightening. A number of models still suggest that interest rates should be substantially higher. Meanwhile, it doesn’t take a rocket scientist to recognize that with headline consumer inflation running at nearly 9% vs. a Fed funds target rate at a range of 1.5%-1.75% after Wednesday’s hike implies that the central bank remains far behind the curve. Economic growth is slowing, and may slip into recession at some point later in the year or in 2023. But until the case for recession looks more compelling for the immediate future, the interest-rate-hiking influence will probably drive sentiment in the bond market.

Nonetheless, this is still a fluid situation and so today’s wisdom may be tomorrow’s garbage. Meanwhile, the forecasts are flying every which way and economists are furiously revising expectations. By some accounts, the revisions have nowhere to go but down.

"More than two months ago we forecasted that the U.S. economy would tip into a recession by end-2023," Deutsche Bank Chief U.S. economist Matt Luzzetti wrote in a note to clients on Friday. "Since that time, the Fed has undertaken a more aggressive hiking path, financial conditions have tightened sharply and economic data are beginning to show clear signs of slowing. In response to these developments, we now expect an earlier and somewhat more severe recession."

Strategy benchmarks continue to sink. The bearish pall is strengthening as all our strategy yardsticks tumble deeper into the red. Nothing’s working at the moment in terms of broad beta exposure and so there’s nowhere to hide. Even commodities, broadly defined, are now taking it on the chin. For details on the benchmark designs, see this summary.

Perhaps the main question is whether all the pandemic premia will soon evaporate? We’re about halfway there and it’s not obvious that the other half is safe. Staying defensive, in other words, still looks like the best deal in a rotten deck. ■