The ETF Portfolio Strategist: 17 March 2021

Trend Watch

In this issue:

Treasuries continue to bleed

Housing construction slowed in February, but housing stocks didn’t notice

Is the gold selloff ending?

The bond trend remains bearish: The benchmark 10-year Treasury yield rose to yet another one-year-plus high today: 1.63%. The rise came despite the Federal Reserve’s comments today that reaffirmed its commitment to hold rates steady – near zero percent for the Fed funds target rate. But if that was supposed to help keep longer rates steady, today’s results were disappointing.

The iShares 7-10 Year Treasury Bond ETF (IEF) certainly took it on the chin today and traded down, decisively breaking lower and signaling that the bearish slide has room to run.

While the Fed remains on track to keep rates lower for longer, it’s notable that the central bank upgraded its economic growth and inflation forecasts for 2021. US gross domestic product (GDP) this year is now expected to increase 6.5%, a sharply higher gain vs. the previous 4.5% forecast. Headline PCE inflation is also projected to increase at a higher rate in 2021: 2.4% vs. 1.8% in the December estimate.

Faster growth, higher inflation and keeping monetary policy aggressively dovish inspired the bond market to do what the central bank won’t: raise interest rates by way of selling bonds. For the moment, it’s not obvious what forces will soon intervene to end or at least stabilize IEF’s decline. Look out below!

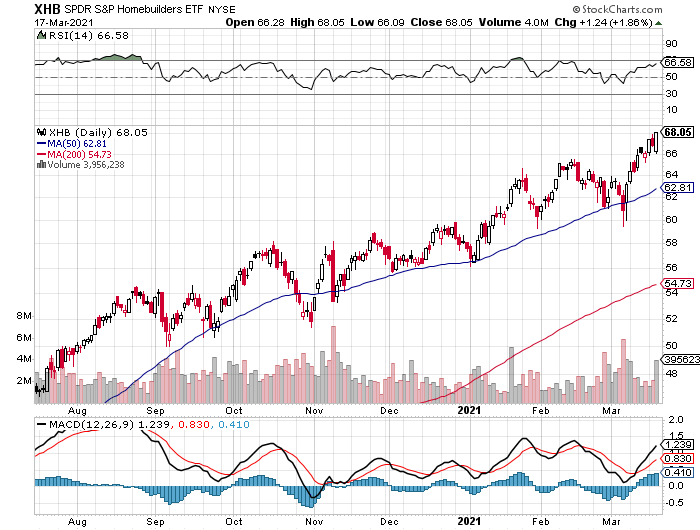

Blame it on the weather: The government today reported a sharply lower level of US residential housing construction in February vs. what economists were expecting. If that was a sign for a selloff in homebuilder stocks, investors didn’t get the memo.

The SPDR S&P Homebuilders ETF (XHB) rose a solid 1.9% to a new record high today. Par for the course for the fund, which has been trending higher persistently following the coronavirus crash a year ago.

It’s interesting to note that homebuilder sentiment, in yesterday’s update for March, also fell, albeit moderately and after setting record highs.

What accounts for the ongoing optimism in XHB? The bullish spin is that the speed bump in housing activity last month is temporary, due to unusually harsh winter weather.

Maybe, but there are other headwinds to consider. “While the desire to build more homes is there, it’s constrained by high costs for materials such as lumber, a dearth of affordable lots, and costly regulations,” says First American deputy chief economist Odeta Kushi.

Based on XHB’s price action of late, those setback are expected to be minor headaches in a market that shows no sign of cooling, at least when viewed through the prism of housing shares.

Is gold starting to rebound? The world’s favorite precious metal has had a rough ride since last August. Although there have been several rallies, SPDR Gold Shares (GLD) has been caught in a tenacious slide for much of the past seven months. Given that backdrop, it’s curious that GLD rallied again, for a third straight day.

I say “curious” because interest also rates pushed higher again today. As noted above, the 10-year Treasury yield ticked up to a new one-year-plus high. Higher rates tend to be a challenge for gold since a zero-percent-yield monetary asset (as some refer to metal) becomes less competitive the higher rates go.

Real (inflation-adjusted) rates are a better comparison to judge the relative attractiveness (or lack thereof) of gold. With real rates (based on inflation-indexed Treasuries) comfortably in sub-zero terrain over the past year, gold’s allure has been unusually compelling. But that began to change with this year’s rise in nominal rates, and the commensurate rise in real rates, which are still negative but less so for some maturities.

But an interesting divergence between 5- and 10-year real TIPS rates bears watching. While the 10-year real yield has been inching higher in recent weeks, the 5-year real yield has been ticking lower over the past week and today dipped to -1.78% -- close to a record low for this maturity.

Is the recent uptick in GLD picking up on the renewed decline in the 5-year real yield, which implies a higher gold price? Maybe. Or perhaps this is another false rally. The next week or so could provide a decisive answer, one way or the other. Meanwhile, watch those real yields, particularly at the 5-year maturity. ■