The ETF Portfolio Strategist: 17 NOV 2024

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

The election premium wilted last week, but it’s too early to see this as something more than noise. The Republicans officially secured a majority in the House and so that gives the GOP, which took back the Senate, control of Congress and the White House — a political trifecta that all but ensures that the president-elect’s pro-growth policies, via lower taxes and reduced regulations, will move forward in 2025. Tariffs and deportations, however, are wild cards. Trump’s plans to sharply raise import duties and deport immigrant workers could create economic headwinds for the American economy. But the trend data to date remains bullish and so the bears will remain on the defensive until there’s more than worrisome forecasts to chew on.

All four of our global asset allocation ETF proxies retreated last week, but solid year-to-date results endure. See this summary for details on the metrics in the tables.

The Global Trend Indicator (GTI), which summarizes the trends for the four funds above, took a hit last week, but a rising tide still dominates the overall profile and so it’s reasonable to dismiss the latest setback as noise.

A caveat for globally diversified portfolios is that the bullish aura is becoming increasingly dependent on US risk assets. As foreign economies come to grips with policy changes on track with a Tump 2.0 presidency, there’s an assumption that the price tag for America’s gain will come at the expense of trading partners around the world.

“Investors fear that Europe will be in the front line of the coming trade war,” says Chris Turner, global head of markets at ING. “In the absence of European fiscal stimulus, it looks like the support is going to have to come from the ECB.”

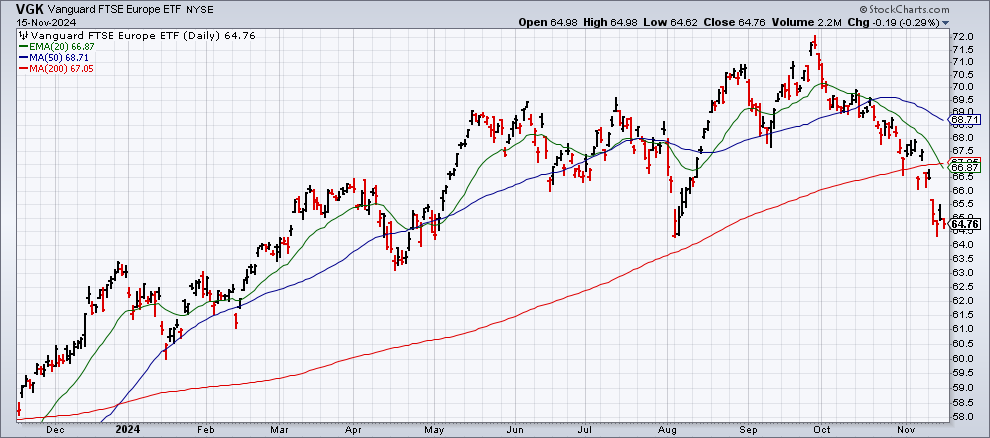

Consider the Vanguard FTSE Europe ETF (VGK). The rally that that was humming through the end of October has sharply reversed, cutting the the fund to its lowest level since August. It doesn’t help that Germany, Europe’s biggest economy, was already faltering before the US election and now looks unusually susceptible to Trump’s policy agenda.

“If the [US] tariff plans are implemented, it could cost us one percent of economic output in Germany,” says German Bundesbank President Joachim Nagel. “That is painful, especially since the German economy is not growing at all this year and will probably only grow by less than one percent next year. If the new tariffs are actually imposed, we could even slip into negative territory.”

The risk-off sentiment is hardly limited to Europe. Stocks in Asia and emerging markets have taken hits in recent days, in part due to the same Trump-related concerns.

The main focus on the trade front for 2025 is how the US-China relationship fares. “The Chinese are ready to negotiate and deal, and probably hope for early engagement with the Trump team to discuss potential transactions,” says Bonnie Glaser, managing director of the German Marshall Fund's Indo-Pacific Program. “At the same time, however, they are ready to retaliate if Trump insists on imposing higher tariffs on China.”

The potential for a trade war, in short, can’t be ruled out. Some observers dismiss such fears as exaggerated, citing the first Trump administration and noting that despite the tough language and increase in tariffs the global economy weathered the storm and arguably thrived. But “the impact on trade would likely be much larger than the trade war 1.0,” predicts Daniel Yi Xu, an economics professor at Duke University.

If there’s also a risk for the US economy in rising trade tensions, the fear has yet to show up in the US stock market. Although broad market benchmarks fell last week, our Signal scores for the equity sectors are still indicating a strong bullish bias overall.

But there are many moving parts to Trump 2.0, along with a myriad of feedback loops. As markets in the US and around the world continue to digest the regime change brewing for next year, the next several weeks will be a stress test for deciding how comfortable the crowd is with the new world order that will soon begin unfolding.

The early guesstimates are that the US will be a net winner and the rest of the world suffer. That’s a reasonable first approximation, but these are early days. The current outlook will almost certainly will be refined in some degree in the days and weeks ahead. ■