The ETF Portfolio Strategist: 17 SEP 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

The broad trend for globally diversified portfolios using multiple asset classes is still positive, but upside progress has ground to a halt recently. It’s still unclear if this a pause that lays the foundation for new highs in the near term or a peak that will confirm that 2023’s rebound is a bear market rally.

The debate centers on the usual suspects that have been bubbling for months, including: Has inflation peaked? Are the Federal Reserve’s interest rate hikes history? Is recession risk low or just delayed due to pandemic effects? And here’s one that promises to draw an ever bigger crowd in the days ahead: Is political dysfunction in America set to go ballistic, again, via the threat of government shutdown on Sep. 30?

No one knows the answers at this point and neither do markets, which is why prices have been caught in a tight trading range in recent weeks. The churning looks set to continue until one or more events break the stalemate, for good or ill, and provide animal spirits with a new sense of motivation and direction.

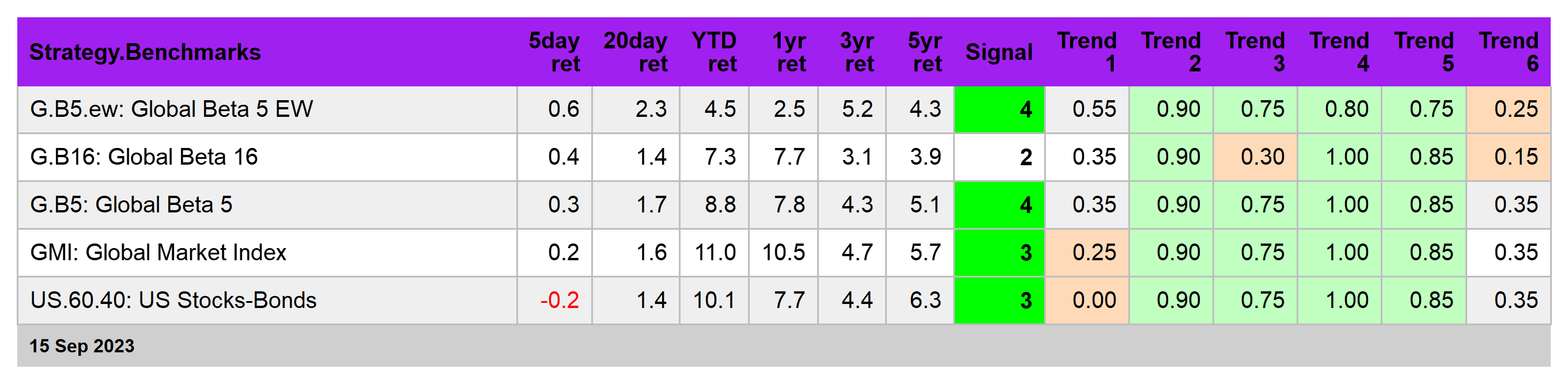

Meanwhile, the latest move was up for most of our portfolio strategy benchmarks. The Global Beta 16 Index (G.B16) rose 0.6% for the week and is higher by a moderate 4.5% for the year. See this summary for design details on the strategy benchmarks and this summary for how the metrics in the tables below are calculated.

Commodities (GCC) are still posting the strongest upside momentum profile for the G.B16 components (see table below). As noted last week, the asset class appears to be flirting with a bullish shift in trend after more than a year of trading in a range following a sharp loss in mid-2022.

Several other market corners are skewing bullish, but the headwinds of late for risk assets generally is still difficult to overcome. Notably, US stocks (VTI) are churning in a tight range that’s just below the summer peak.

A similar story applies to equities in Japan (EWJ), which is trying to top recent highs.

On the flip side, US Treasuries (IEF) still reflect a bearish bias even after stabilizing in recent weeks. IEF’s Signal score is a deeply negative -5 per the table above and the technical profile in the chart below doesn’t look any better.

In search of new clues about what comes next, the bond market will be focused on this week’s Federal Reserve policy meeting (Wed., Sep. 20). Traders are still pricing in high odds for no change in the target rate via Fed funds futures, but there’s still plenty of deliberation about whether rates have peaked for this cycle. Accordingly, markets will be keenly reviewing the new Fed forecasts scheduled for release on Wednesday, along with Chair Powell’s press conference.

For some analysts, the question is no longer about rate cuts or hikes. Rather, “We expect the committee to continue shifting to a message of ‘higher for longer’,” predicts Oscar Munoz, chief US macro strategist at TD Securities. The upcoming forecasts and comments from Powell “might have a hawkish flavor to them as Fed officials aren’t likely to fully close the door to additional rate increases”, he advises.