The ETF Portfolio Strategist: 18 Feb 2022

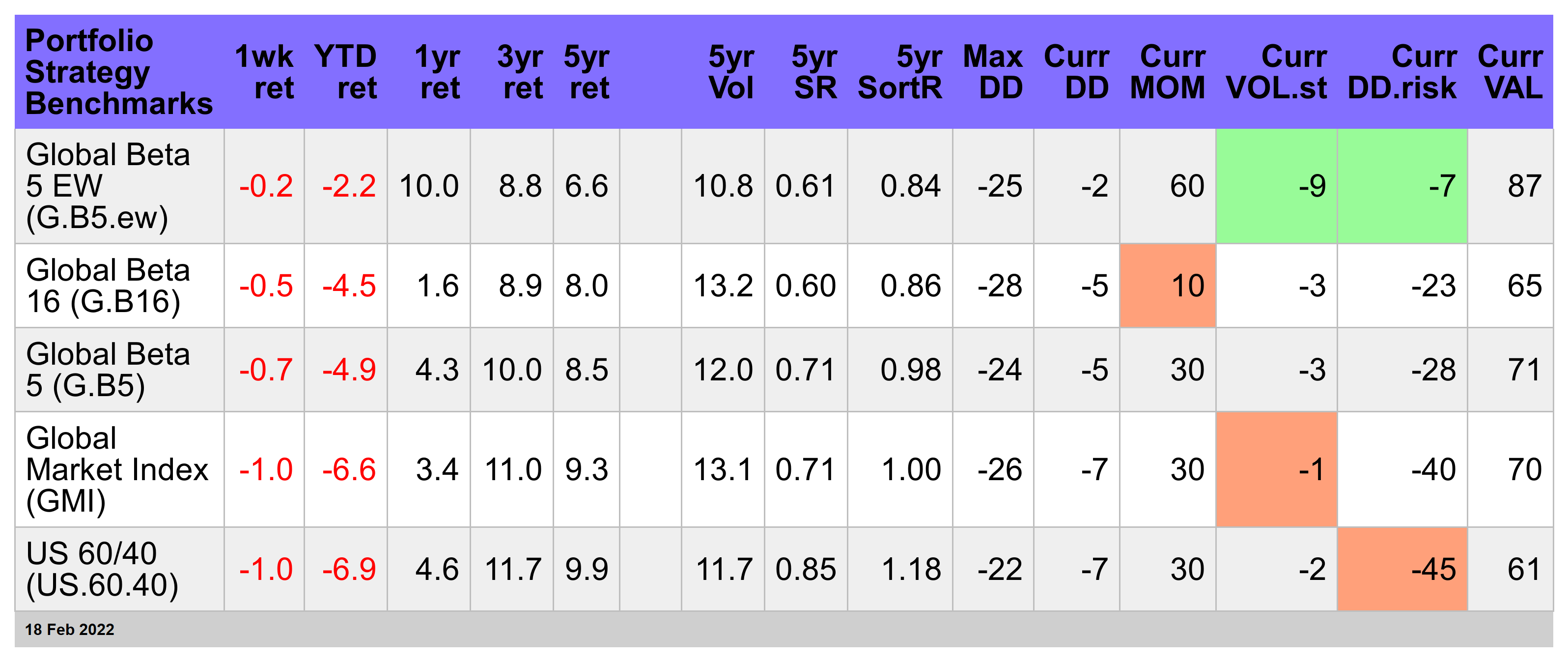

Portfolio Strategy Benchmarks

Global markets were mixed this week as Russia-Ukraine risk continues to simmer

Emerging markets bonds are still posting a modest upside bias

Selling continues to weigh on US stocks and US REITs

Another week of losses for our portfolio strategy benchmarks, but equal weighting global assets continues to offer a relatively strong defense

The threat or war, or at least rumors of war, continue to hang over markets. There was a bit of risk-off trading that lifted safe-haven assets in the trading week through Friday’s close (Feb. 18), but the momentum for reversing the recent downdraft in bonds doesn’t look convincing. For details on the metrics in the table below, see this summary.

Convincing or not, the iShares 7-10 Year Treasury Bond ETF (IEF) eked out a slight gain this week. Nonetheless, the uptick hardly changes the calculus for the near-term trend, which remains bearish. Betting on higher Treasury prices (and lower yields) is plausible, assuming you’re in the camp that thinks Russia’s intimidations directed at Ukraine will persist if not escalate. Given the headlines in recent days, it’s easy to assume no less. Then again, using Putin as a basis for deciding how much to allocate to Treasuries is a tough way to make a living.

Absent the Russia-Ukraine factor, the slide in Treasuries would probably roll on. But as this flavor of geopolitical risk doesn’t look set to abate any time soon, IEF may continue to catch a bid in the near term. But if diplomacy succeeds, gains could evaporate quickly.

As for our 16-fund opportunity set covering global markets, emerging markets bonds continue to show an upside reversal. VanEck Vectors JP Morgan EM Local Currency Bond (EMLC) rallied 1.0% this week and closed near its highest level in three months. It’s premature to call this the start of a new bull run, but the recent strength is intriguing and worthy of close monitoring and deeper analysis.

Meanwhile, commodities continue to push higher. A perfect storm of elevated inflation and geopolitical risk a la Russia and Ukraine is helping keep WisdomTree Coninuous Commodity (GCC) trending up. The rally looks set for a breather, if not a correction, but with the possibility of war lurking it’s possible to see a string of new highs.

By some accounts, there’s a long way to go for raw materials prices. Gary Schlossberg, global strategist at Wells Fargo Investment Institute, sees a “super cycle” for commodities brewing, in part due to under-investment in recent years.

The general tide of selling continued to weigh on our portfolio strategy benchmarks. Once again, however, the equal-weighted Global Beta 5 EW (GB5.ew) is showing the strongest defense. For details on how the benchmarks are designed and managed, see this summary.

The decision to give commodities equal weight with global stocks, bonds and real estate continues to reap rewards. This edge is especially conspicuous for the trailing one-year window: G.B5.ew is up 10.0% over the past 12 months, far ahead of its competitors that embrace conventional asset allocation rules.

Can equal weighting’s edge persist? The answer depends in part on whether Schlossberg’s super-cycle forecast for commodities is accurate. ■