The ETF Portfolio Strategist: 18 JUN 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

The bull run for global investment portfolios enjoyed another winning week. I should be celebrating, but I can’t shake a nagging feeling that the markets are setting me up for a head fake. But for the moment numbers speak louder than behavioral ticks.

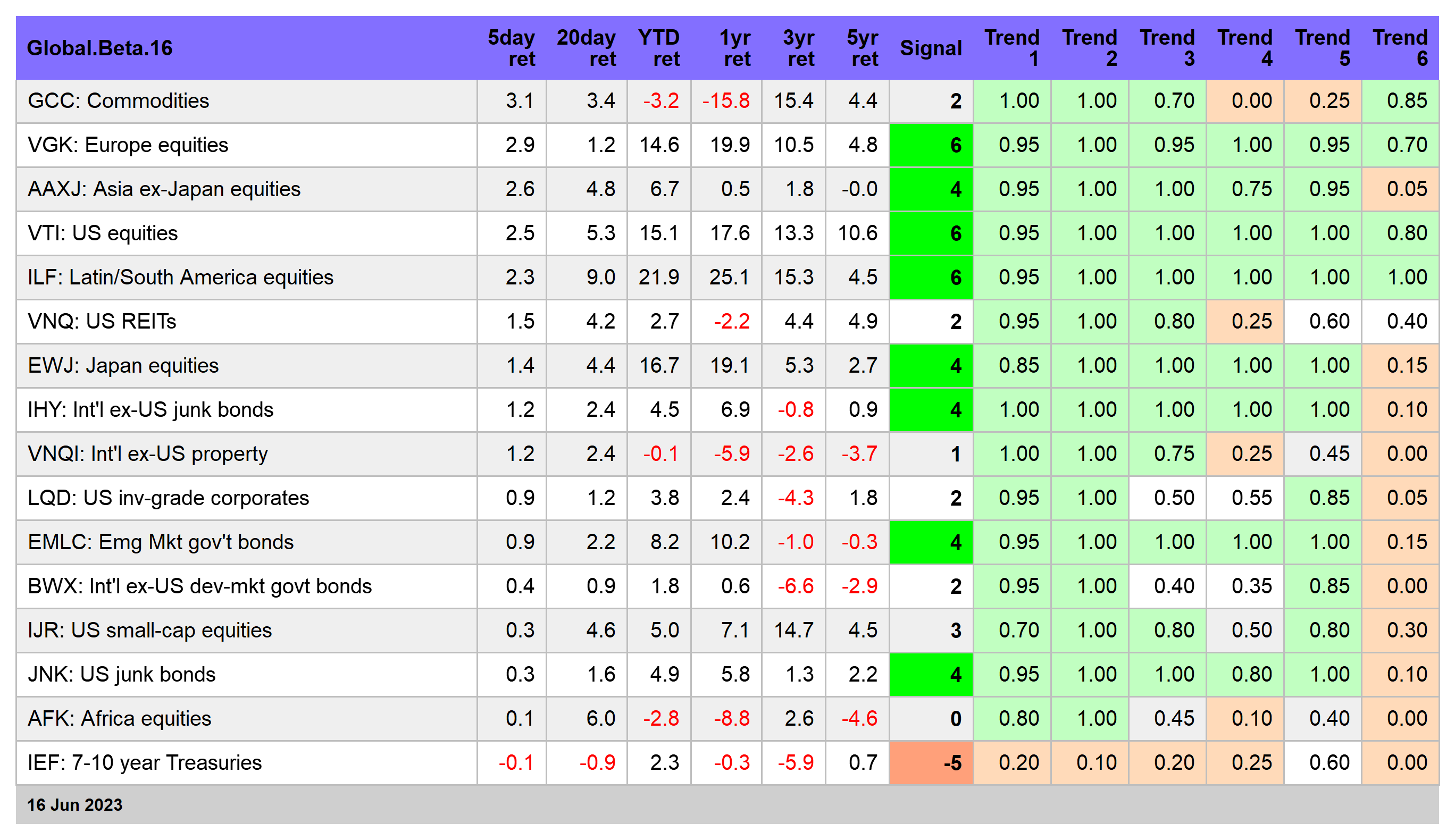

Our standard global opportunity continued to push higher last week, closing up 1.7%. For the year, G.B16 is now ahead by nearly 9%. Given that it’s only June, that’s a stellar run for a passive multi-asset-class portfolio that’s globally diversified.

This year’s red-hot rebound is, of course, unsustainable and probably due for some backfilling at the least. If we’re lucky, markets will digest the latest rally by treading water for a time. See this summary for design details on the strategy benchmarks and this summary for how the metrics in the tables below are calculated.

Meanwhile, G.B16’s technical profile certainly looks encouraging. After the latest runup, the strategy benchmark cleared its previous highs, which implies that new heights await.

The question is whether G.B16’s current upswing will soon reclaim its former all-time high set in early 2022? Similar questions apply to various asset classes, including US equities. Vanguard Total US Stock Market Index ETF (VTI) rallied for a fifth straight week, a winning streak last seen in late-2021, when the crowd’s outlook had yet to be dented by the war in Ukraine, Fed rate hikes and other risk factors that continue to threaten in varying degrees. But while the near-term outlook looks encouraging from a momentum perspective, returning to the early 2022 peak is still nowhere on the near-term horizon.

Some are labeling the current rally a new “bull market” for US shares by virtue of the 20%-plus rally off the October low. Maybe, but until the record peak of early 2021 is taken out, debate will swirl on whether this is the genuine article or just an extension of a bear market rally.

As a thought experiment for what may be coming, it’s useful to map out how US stocks could push substantially higher from here and reach a new record high. The short list of possible/likely catalysts included:

The US economy avoids a widely expected recession in the near term and instead extends the modest expansion of late

Inflation continues to ease to a degree that encourages the Fed to extend its rate-hike pause, or at worst lift interest rates one last time for this cycle at the next month’s policy meeting

Light at the end of the tunnel emerges in the war in Ukraine, if only on the margins

The US and China make headway in dialing down geopolitical/geoeconomic risk that continues to weigh on relations between the world’s leading economies and military powers

Corporate earnings grow faster than expected and keep equity market valuations from rising even as share prices climb, which in turn gives the bulls some leeway for bidding up stocks to new heights

Each of these items comes with a more than a trivial risk of disappointing the bulls. But it’s reasonable to assume that at least one of these scenarios kicks in. The more likely wins are the first two: economic growth rolls on, and perhaps strengthens, while inflation continues to slide.

Let’s assume both scenarios unfold. Is that enough to keep the bull engine humming? Probably, but that’s assuming that the other three risk items don’t deteriorate relative to current conditions. I’m not ruling out that triple play out, but at the very least it’s likely that any bull run from here on out is a relatively precarious beast lest something goes wrong.

But even if we avoid the aforementioned pitfalls, there’s always another joker lurking in the deck these days. The latest addition: government shutdown risk, the new edition. Per The Wall Street Journal today:

House Speaker Kevin McCarthy’s latest pledge to cut spending—intended to again mollify hard-right members of his party—has put Congress on a collision course with a potential government shutdown later this year.

To become House speaker in January, the California Republican promised deep spending reductions. To reach a debt-ceiling deal with the White House, he tacked to the middle, agreeing to smaller constraints than conservatives wanted. Eleven Republicans revolted this month, withholding procedural votes and bringing the House to a halt. That prompted the speaker to promise another crack at cuts, this time in the appropriations process now getting under way.

Or as Al famously laments, “Just when I thought I was out, they pull me back in.”