The ETF Portfolio Strategist: 19 NOV 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Programming note: The ETF Portfolio Strategist is taking a holiday. The next issue will be published Dec. 3. Cheers!

As markets continue to rebound, my recent view that stocks will remain in a trading range, at best, continues to suffer. Is it time to throw in the towel and embrace what some are saying is the start of a new bull market? No, but if equities continue to push higher, and take out key levels in the days and weeks ahead, your editor will be forced to capitulate to the wisdom of the crowd.

Last week’s trading activity certainly favored the bulls—again. All four of our standard proxy ETFs for tracking various flavors of portfolio strategy posted robust weekly gains. In fact, the quartet is showing solid across-the-board gains for 2023. Meanwhile, the Signal scores are close to maximum bullish readings. See this summary for details on the data in the tables below.

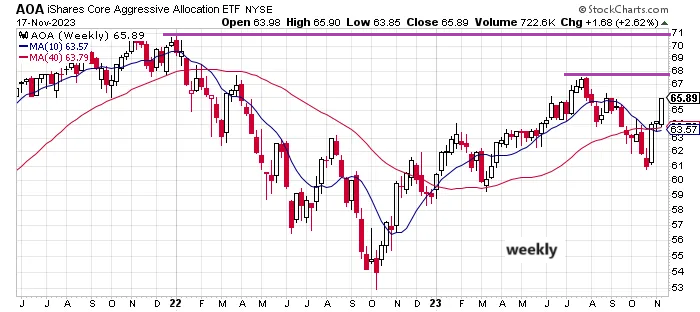

Using the iShares aggressive asset allocation ETF (AOA) as a guide, I’ll be looking for two key price developments (or lack thereof) in the days/weeks ahead. First, will AOA take out its previous high of near-68? If that level gives way, my cautious/defensive outlook recently will take another hit. When/if that occurs, the next target is ~71, the fund’s all-time high. If the ETF can decisively break above that mark, the case for caution may be on its last legs.

A similar profile can be applied to US stocks (VTI), which may also be poised to take out the summer highs as a prelude to setting a new all-time price.

Meanwhile, last week’s rallies were broad and deep enough to tip the odds in favor of the bulls. Indeed, all corners of global market posted gains:

The pushback is that recent market behavior is simply noise in a trading range, bounded by January 2022’s high and October 2022’s low for US stocks, to cite one set of numbers. I still expect that a trading range will will prevail for the rest of the year and into early 2024.

Why? The short answer: many/most of the headwinds that created 2022’s sharp correction are still bubbling, albeit in somewhat diminished degree. Risk markets will, as always, transition to a new regime, and this time is no different. My view, however, is that the transition will take longer than the bulls are forecasting.

Yes, I could be wrong. But in the current environment I still prefer to be late to the party rather than early. My reasoning: there’s still more risk bound up with the latter vs. the former.

A key counterpoint I’m hearing from some analysts: the Fed’s rate hikes are history and will soon start cutting. I agree with the former, but not the latter. For the moment, I still think sentiment has gotten ahead of itself in pricing in rate cuts. Yes, there’s a good argument for expecting cuts sometime next year. But the US economy continues to look on track to expand through the fourth quarter, albeit at a sharply softer rate vs. Q3.

A crucial part of the analysis is monitoring how the US economic activity evolves. As discussed in today’s issue of The US Business Cycle Risk Report, recession odds remain low, and look set to remain so through January. In turn, looking for rate cuts is premature. In fact, there’s a non-zero probability that the economy could surprise on the upside well into Q1 in terms of extending the current expansion.

For now, I’m focused on evaluating how the November economic profile stacks up — specifically, do the numbers corroborate the early signs in October that the expansion, although softer, is still intact? My analytics suggest the answer is “yes”. Until I see strong evidence to contrary, I’m still in the camp that thinks it’s too soon to talk about rate cuts, and perhaps even to close the book on one more rate hike.