The ETF Portfolio Strategist: 2 APR 2023

Is it risk-on yet? By some accounts, yes, and it has been for a couple of months, advocates in this camp advise. For skeptics, including your editor, last week’s rallies throughout most global markets aren’t doing yours truly any favors on the oracular front.

The goal on these pages, however, is less about forecasting the next turn in markets (which is nigh impossible, especially for mortals such as your editor) vs. assessing the current risk profile for the broad sweep of betas and deciding what the results imply for asset allocation over the intermediate term.

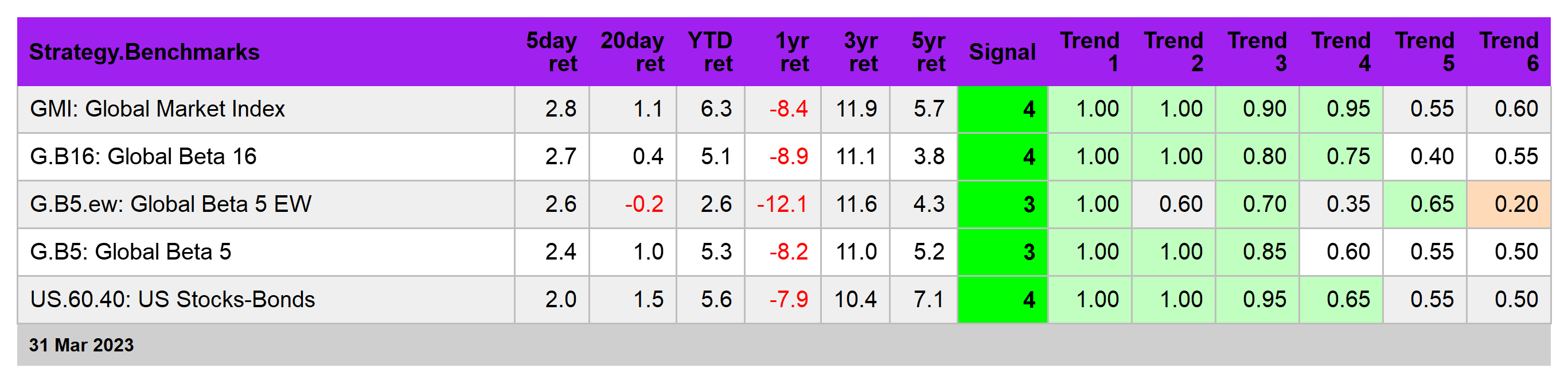

By that standard, the broad sweep of market activity continues to trade in a gray zone. The G.B16 strategy index, for example, continues to hold on to most of its recent gains, but appears to be stalling into a trading range. Absent the current lineup of geopolitical and macro risks the prospects for risk-on would look more compelling. But in the world as it exists, the recent bounce in G.B16 (and its various counterparts) still looks like a recovery from a steep decline vs. newly reanimated animal spirits fueled by substantially brighter growth prospects. See this summary for design details on the strategy benchmarks listed below.

Nonetheless, markets are feeling cheery again. All of our strategy benchmarks posted substantial gains last week. An added boost: the aggregate Signal score rose to bullish terrain. If the Signal scores can stay green for a few weeks, it may be time to rethink our cautious outlook. For details on how the metrics in the tables above and below are calculated, see this summary.

Some of the components in the G.B16 opportunity set are looking especially strong lately. Stocks in Europe (VGK) stand out and may be poised to break above the resistance line at roughly $60.

A similar story applies to bonds issued by governments in emerging markets (EMLC).

US stocks (VTI) are also flirting with a possible upside breakout.

The trends for some markets are looking friendlier, but the macro backdrop remains cloudy. Investor sentiment still needs to work through a number of potential hazards, including the path ahead for the Federal Reserve’s monetary policy.

The critical variable, of course, is inflation. Although pricing pressure has clearly peaked, the operative question is whether inflation will decelerate fast enough to satisfy the Fed and convince it to pause on rate hikes? Friday’s update on PCE inflation wasn’t particularly helpful for reading this cup of tea leaves.

Core PCE, the Fed’s preferred inflation benchmark, eased on a year-over-year basis to 4.6% and matched December’s pace as the softest increase since Oct. 2021. Progress, but the slide is starting to look a bit sticky, which casts doubt on the idea that the Fed will soon declare victory on taming inflation.

Perhaps, then, it’s no surprise that Fed funds futures are pricing in 50/50 odds for another rate hike at the next FOMC meeting on May 3.

A critical variable that may decisively tip the scale, one way or the other, for the Fed’s expectations and actions: the evolution of US economic activity. On this front, too, there are solid arguments (with supporting data) for both sides of the debate.

In other words, there’s still a bit too much flux in the outlook to convince this observer to say that the odds lean heavily in favor of risk-on. To be fair, we’re no longer in the defensive camp and have upgraded expectations to neutral. In other words, our current guesstimate is that markets will churn in a trading range until a bit more clarity emerges. How and when that clarity arises is as unclear, but at some point the haze will break. ■

I look forward to this every week. Thank you!

Excellent commentary, as always