The ETF Portfolio Strategist: 2 JUN 2024

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Markets eased for a second week, but it’s too soon to read any strategic significance into the selling, which remains modest. The trend profile still suggests that the recent slide is within the parameters of the normal ebb and flow in what continues to look like an upward biased market.

Consider the iShares Aggressive Allocation ETF (AOA), which lost ground for a second straight week. The modest decline from its recent peak has yet to signal an end to the upturn that’s been unfolding since November.

Supporting the upwardly trending view for AOA is the moderately bullish Signal score of 3 for the ETF (matched for two of its counterparts in the iShares asset allocation suite of ETFs shown below). A fourth fund — the conservative allocation ETF (AOK) reflects the weakest trend, although it’s still net positive (above zero). See this summary for details on the metrics in the tables below. Note: the 5-day return in the table below differs slightly from latest weekly data in the charts on this page due to the holiday shortened four-day US trading week through May 31.

But with no shortage of risk factors bubbling around the world it’s hard to escape the question: Are we’re in the early stages of peaking markets? Possibly, but the market data suggests it’s too early to make such a diagnosis with any degree of confidence. Conservative investors may not care and therefore err on the side of caution and derisk their portfolios and take advantage of relatively high-yield cash.

Meanwhile, for those who prefer statistical support for moving closer to a risk-off decision a sign to look for that would lean into the view that a run of deterioration has started would be several weeks of AOA trading below its 5-week average. Beyond that, a more worrisome sign: AOA’s 5-week average dips below its 20-week counterpart. There are many variations on this form of analytics, but the basic concept is that it’s prudent to wait for comparatively persuasive signs of a breakdown in the trend before jumping to conclusions. On that basis, it’s still too soon to view recent market action as something more than short-term noise from the perspective of global asset allocation strategies a la AOA and its counterparts.

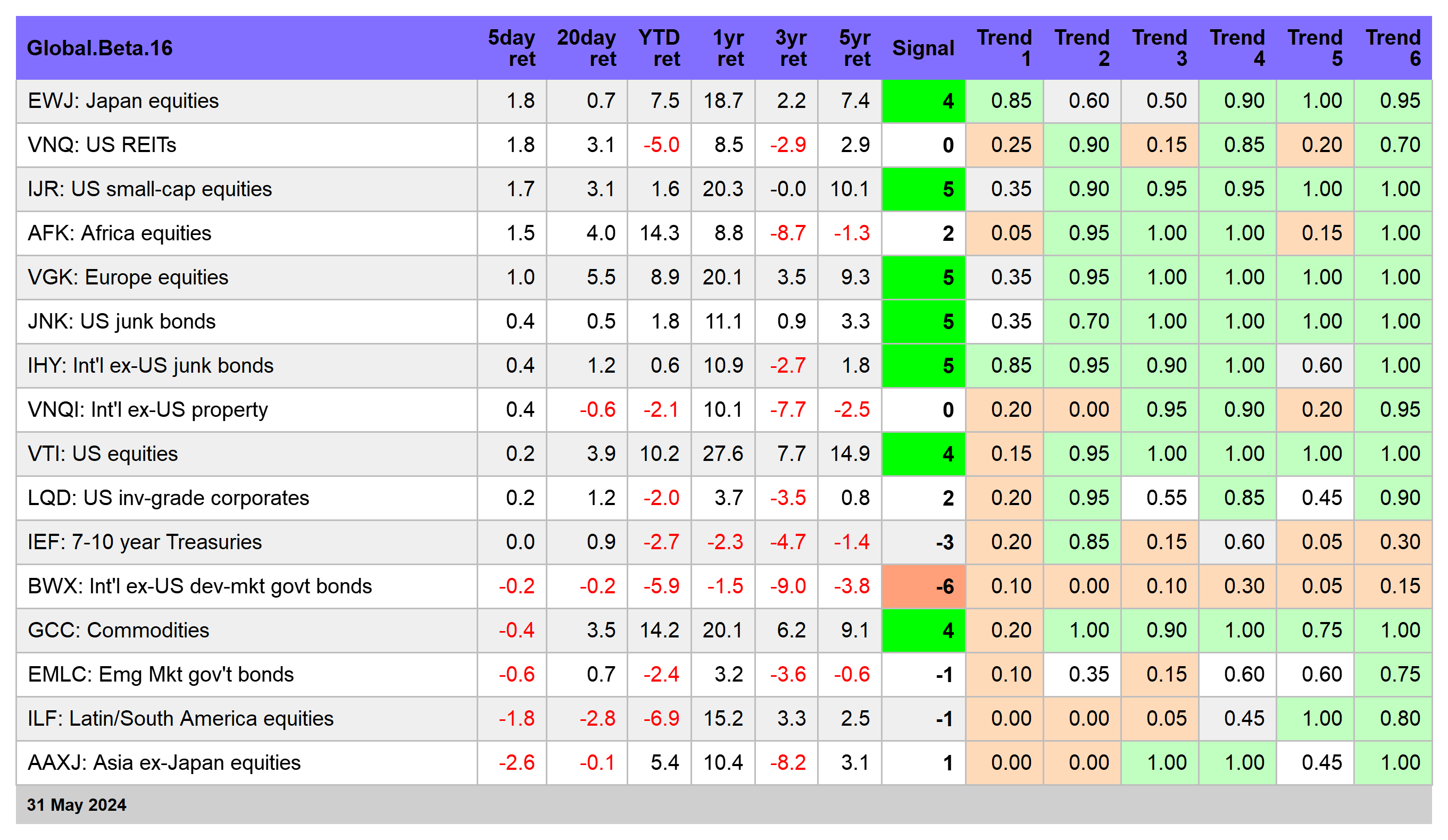

Another reason to reserve judgment on an early call in favor of bearish turning point: there’s still an upside bias for Signal scores among the major components of the world’s markets, per the table below. If and when trends start to crumble in a meaningful degree, the shift will become increasingly conspicuous via the retreat of green on the screen in the Signal scores below.

One market I’m watching closely: US Treasuries, which may finally be bottoming after a multi-year bear market. Here, too, it’s premature to make high-confidence predictions, but it’s encouraging to see that the iShares 7-10 Year Treasury Bond ETF (IEF) continues to trade in a middling rage this year and, for now, is trading above its recent low.

Hints that the US economy is slowing will likely provide support for Treasury markets as the possibility of softer output lifts the prospects for a rate cut in the near-term future. The crowd is still estimating the Sep. 18 FOMC meeting as earliest date for policy easing, but November or December are considered stronger possibilities, based on Fed funds futures.

A key focus for reassessing these assumptions is this week’s payrolls report for May, which economists are expecting will post a comparable level of hiring.

As discussed in this week’s edition of The US Business Cycle Risk Research Report, the latest numbers suggest that the macro trend is again pointing to deceleration rather than stabilization. Recession risk is still low, even if the economy’s downshifting is more likely than recently assumed. But if Friday’s update from the Labor Dept. (June 7) confirms this subtle but potentially crucial change in the economic trend bias, the bond market will likely receive a fresh boost that favors the forecast that the worst has finally passed for US Treasuries. If so, current yields will turn out to at or near high points for this cycle. ■