The ETF Portfolio Strategist: 20 May 2022

Portfolio Strategy Benchmarks

Treasuries rally for a second week

Our main portfolio benchmark managed to eke out a gain this week

Here’s something we haven’t seen in a while: back-to-back weekly gains for the US bond market. The last time that happened we were deciding whether to have another slice of pumpkin pie at Thanksgiving dinner.

The question is whether fixed income’s painful correction that’s been running for much of this year is fading (or ending)? Too soon to know. For now, put me down as skeptical, but the possibility is stronger that we may be in a trading range for the near term. For details on the metrics in the table below, see this summary.

What is clear is that the bleeding has stopped. The iShares 7-10 Year Treasury Bond ETF (IEF), for example, rose 1.2% for the trading week, building on the previous week’s gain.

Animating the rally: forecasts that the US economy is headed for a recession. Maybe, although that still looks like a low risk for the near term, as I outlined earlier today. The macro trend is slowing, but gradually and so the earliest you can reasonably forecast that an NBER-defined recession will start is late-Q3/early Q4 (assuming you’re unusually bearish on the economy). I’ve read some forecasters at large banks saying a 2022 recession is likely. One intrepid dismal scientist expects a contraction to start in late-2022. To his credit, he didn’t cite a specific day.

The problem, of course, is that looking much beyond two or three months is beyond the capabilities of mere mortals and so if you don’t see a recession brewing in the near term (and I don’t), looking further ahead is really just guessing. Why? Let’s just say that stuff happens, for good or ill, and a lot of it tends to surprise the crowd. My preferred methodology: look forward on a rolling 2-3 month basis, per the format in The US Business Cycle Risk Report. But I digress.

The stock market seems to be pricing in rising recession risk via the bond market and so Treasuries’ historical role as a safe haven is back in vogue. How long will this last? It depends on how disappointing the incoming economic data is. Next week’s numbers, however, don’t look sufficiently dark to make a strong case that the economy’s fallling off a cliff. Quite the contrary: PMI survey data for May is expected to show that while growth is slowing, the slowdown isn’t strong enough to raise warning flags for the summer.

To be fair, our relatively upbeat view of the economic outlook assumes that inflation has peaked and that the growth slowdown will be enough to convince the Fed to rethink ongoing and aggressive rate hikes. But if inflation hasn’t peaked, or it doesn’t begin pulling back in a convincing degree, all bets are off. History, after all, suggests that ending inflation without a recession is a high bar. So, the critical question: Will inflation cooperate by easing without the Fed going whole hog on policy tightening? The answer is unknown, but it’s near.

Which brings us to the next question: Why is the stock market tumbling? Vanguard US Total Stock Market (VTI) slumped 2.8% this week, marking the seventh straight weekly loss. Softer-but-still positive economic growth isn’t helping, but the haircut in US shares still looks more like a victim of Mr. Market deciding that an increasingly risky world with high inflation and rising interest rates deserves a bigger discount rate. By contrast, the correction to date doesn’t appear to be a clear-cut case of Mr. Market pricing in an imminent recession. It may turn into that at some point, but not yet.

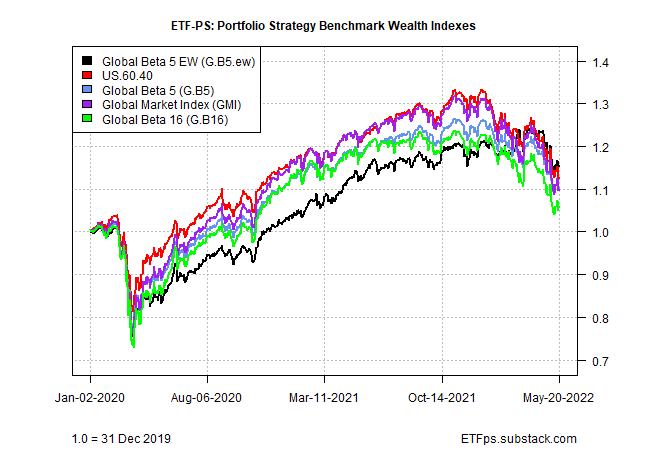

Signs of life for our global-opportunity-set portfolio: A fractional gain arrived after weeks of non-stop loss for Global Beta 16 (G.B16), which always holds all the ETFs listed in table above (in weights shown below. A 0.1% increase for the week is hardly convincing evidence that the future will be kinder and gentler, although it beats the usual routine of late.

But it’s still best to remain cautious. Indeed, the other strategy benchmarks we track continued to lose ground. Is G.B16 an early sign of revival ahead? Or is it an outlier? Hard to say at this point. Accordingly, it’s best to treat the slight gain as noise. Let’s see if the next several weeks offer a different perspective.

That said, a run of consolidation for the near term wouldn’t be surprising. What would treading water presage? To be determined. Whatever coming’s, the second act of this drama is about to start, albeit with a still-murky narrative going through the final edits. ■