The ETF Portfolio Strategist: 20 Oct 2021

Trend Watch

Does your bond allocation need more diversification? The question comes to mind in a year when many of the usual suspects in fixed income are nursing losses.

Yes, bond investing is supposed to be “safe,” but there was always fine print to parse. Overlooking the details has been easy in recent decades, thanks to a generally declining trend in interest rates. That trend may or may not be over. (Lacy Hunt, economist at Housington Investment Management with a stellar track record thinks rumors of disinflation’s death are greatly exaggerated — but we digress). Regardless of what’s coming, it’s certainly been a bumpy year so far for assuming rates only decline and bond investments only dispense gains. But a funny thing happened on the way to fixed-income nirvana: reality intervened… again.

Sure, the diversification effect of owning stocks and bonds is widely cited as a tool forged through low and negative return correlations for the two asset classes. But those low and negative correlations can bite, for stocks and bonds, as investors are (re)discovering this year.

At least we know where to place blame. The recent rebound in interest rates is roiling so-called “conservative” bond strategies, including a core portfolio of US investment-grade fixed income.

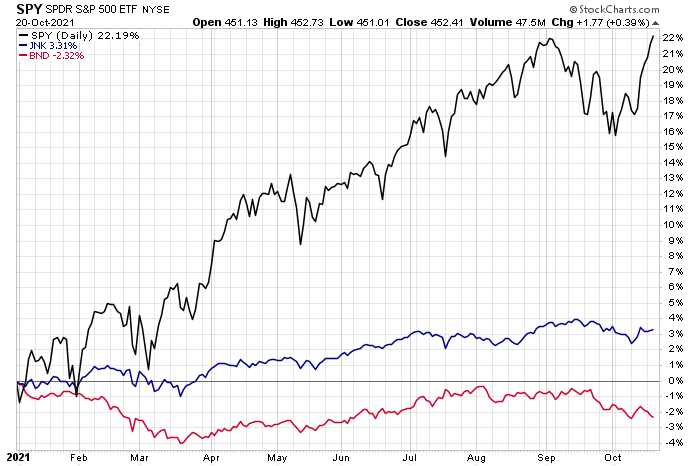

Vanguard Total US Bond Market ETF (BND) is in the red by 2.3% so far this year through today’s close (Oct. 20). The US stock market, by contrast, has rebounded sharply from its latest slide and is up a strong 22.2% year today through today’s close (Oct. 20).

Diversification, in other words, works, although this year’s run may not be what some investors expected.

But Mr. Market’s wisdom, if we can call it that, is a strange and mysterious force of nature. Case in point: so-called junk bonds continue to outperform investment-grade debt by a wide margin year to date. Indeed, SPDR Bloomberg Barclays High Yield Bond ETF (JNK) is sitting pretty this year with a 3.3% gain.

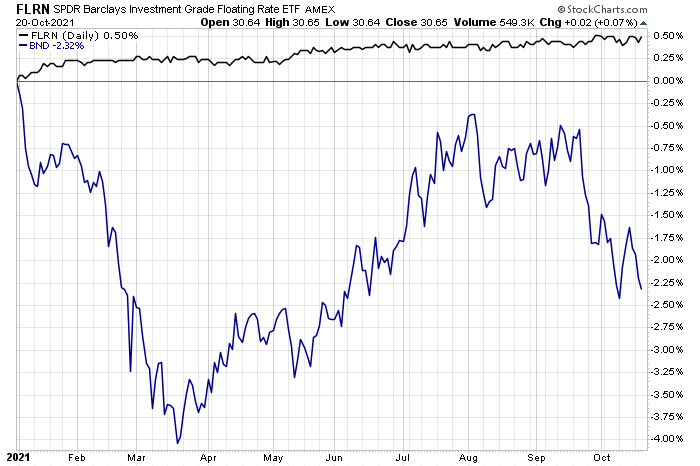

JNK’s rally is no mean feat in a year that’s given much of the rest of the bond world a haircut in varying degrees. Junk’s diversification payoff may be surprising given the off-again-on-again yield increases. On the other hand, no one should be shocked to find floating-rate bonds posting gains in 2021. Designed to exploit rates that reset higher, SPDR Barclarys Investment Grade Floating Note (FLRN) has logged a modest 0.5% year-to-date gain, providing a relatively smooth (and so far) profitable bit of diversification to the core strategy via BND.

The key source of headwinds for most conventional bond strategies is the great reflation trade — a trade that’s lit a fire under inflation-indexed Treasuries via TIP, which is posting a solid 4.0% rise this year. Standard-issue Treasuries (IEF), by contrast, are under water by a similar degree.

The reflation bias has been running hot lately, based on signs of trend persistence via a rough proxy of the inflationary bias by way of the ratio of commodities (GSG) to bonds (BND). As the chart below shows, GSG:BND has been red hot this year and the current technical profile suggests there’s more to come.

The inflation-is-transitory outlook isn’t dead, but the peaking process is extending further into the future than recently expected. Ongoing supply bottlenecks are a proximate cause. Unfortunately, it’s not obvious that the bottlenecks will end soon.

The big question (and mystery) is how or when the Federal Reserve reacts? “If inflation does remain more than moderately above 2 percent, be assured that the FOMC has the framework and the tools to address it,” says Randal Quarles via prepared remarks for this week’s Milken Institute Global Conference.

Rate hikes are still nowhere on the near-term horizon, based on probability estimates via Fed funds futures. But the central bank may be close to starting the process of tapering its bond purchases, which would be a prelude to rate hikes and a signal to the bond market that the policy regime is shifting toward a (slightly) more hawkish stance.

The wild card is the ongoing slowdown in US economic growth, which appears to be decelerating at a stronger pace ahead of next week’s third-quarter GDP report. If so, any plans by the Fed to start shifting to a slightly more hawkish posture may end up on ice, if only temporarily.

For now, however, the bond market is inclined to sell first and ask questions later. The selloff in Treasuries cut the iShares 7-10 Year Treasury Bond ETF (IEF) to its lowest level in nearly five months.

But the bond market still has to work through what will be a difficult question: Will a slowing economy take the air out of the reflation trade and revive the great bond bull market of the past four decades? ■