The ETF Portfolio Strategist: 21 May 2021

Portfolio Strategy Benchmarks

In this issue:

Mostly meandering markets

US assets take a back seat to global asset allocation this week

A mixed week for markets as US stocks continue to dip: There was more meandering that trending this week, but in some corners the fading of the bullish sentiment appears to be gathering strength.

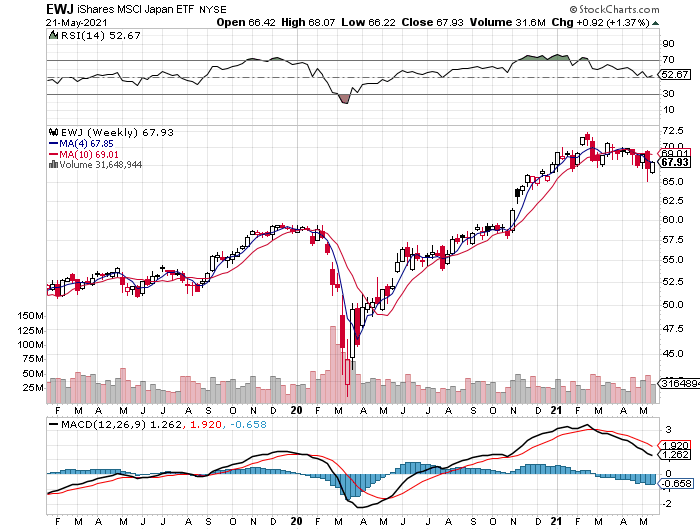

Take this week’s top performer for our global 16-fund opportunity set (a proxy for the world’s major asset classes): equities in Japan. The iShares MSCI Japan ETF (EWJ) led the gainers with a 1.4% weekly advance through today’s close (May 21). Nice, but the rally doesn’t look convincing as recent history suggests the fund is rolling over after a potent rally off of last year’s low. Indeed, EWJ’s momentum ranking (MOM column in table above) remains at 50, which is the midway mark between bearish and bullish biases. Perhaps tipping the scale to darker side in the weeks ahead is today’s news via PMI survey data that shows Japan’s economy slipped back into contraction this month. For details on all the strategy rules and risk metrics, see this summary.

US shares look firmer, although Vanguard Total US Stock Market (VTI) retreated for a second week, slipping 0.3%. But in contrast with EWJ, VTI’s MOM score remains at a red-hot 100 — the strongest bullish print — and so it’s not yet obvious that American stocks are due for an extended correction.

Meanwhile, the 10-year Treasury yield continues to tread water and was unchanged for the week at 1.63%. Inflation may be on track to run hotter, or so we’ve heard. But for now, the bond market’s done pricing in that risk beyond the back-up in rates that’s already baked in.

The flatlining for rates translated to similar behavior for iShares 7-10 Year Treasury Bond (IEF), which ticked up this week but continues to trade in tight range.

This week’s biggest decline: iShares Latin America 40 (ILF), which fell 1.8%. Despite the setback, the fund still appears to be trending higher and ILF’s strong 90 score for MOM doesn’t suggest otherwise.

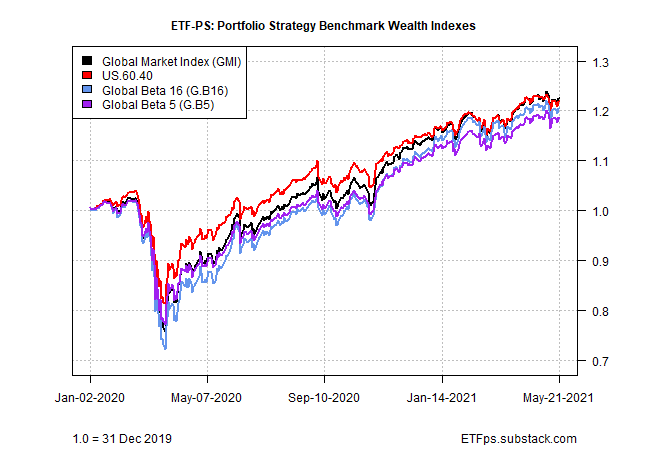

A slight edge for global asset allocation: Owning markets far and wide delivered a slight premium this week. Granted, the edge was thin, but perhaps it’s a sign of things to come. In any case, our global benchmark portfolios avoided a loss, which is more than you can say for the standard US 60/40 stock/bond strategy (US.60.40).

For a second week, US.60.40 retreated, albeit gently, posting a slight 0.1% weekly decline.

Meantime, Global Market Index (GMI) and Global Beta 16 (G.B16) were neck and neck with 0.1% gains. Note, however, that G.b16 continues to hold a comfortable lead year to date over its competitors via a 7.1% gain.

The 100 MOM scores for all the strategy benchmarks implies that the party’s not over. What might derail the festivities with a surprise shock? Inflation risk is probably at or near the top of the list these days. But the bond market’s calm demeanor of late suggests this is a risk that’s faded a bit as a real and present danger. ■