The ETF Portfolio Strategist: 22 Apr 2022

Portfolio Strategy Benchmarks

Another rough week for much of the global markets landscape

US REITs are the lone upside outlier for our global ETF opportunity set

Global selloff takes a bite out of all our strategy benchmarks

Mr. Market’s capacity for shrugging off risk is wearing thin. Although the US stock market, to take the conspicuous example, remains close to its record high, this week’s decline — the third straight weekly setback — suggests that the crowd requires a bigger discount factor in the face of various risks swirling about.

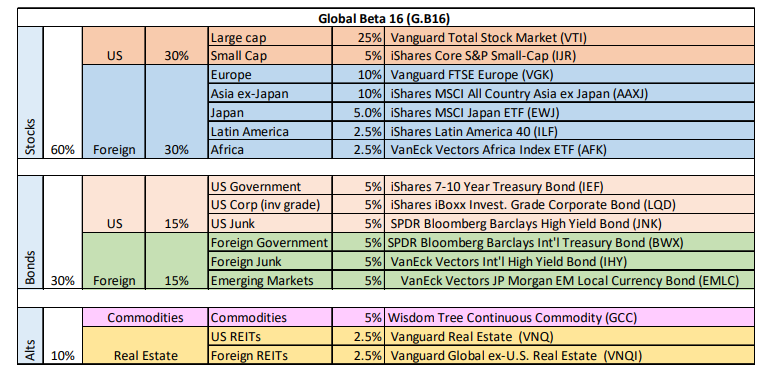

In a sign of the times, most of our opportunity set is now posting extreme bearish momentum scores (MOM column). The upside outliers have dwindled to US REITs (VNQ), commodities (GCC) and Latin America shares (ILF). For details on the metrics in the table below, see this summary.

Only one slice of our 16-fund global opportunity set posted a gain this week: US real estate investment trusts. Vanguard Real Estate (VNQ) rose 0.9%, which supports our recent view that this asset class is starting to look attractive again on a trending basis. The fact that VNQ was able to rise while the markets elsewhere fell is another hint that the fund’s upside potential may be anew.

Otherwise, losses across the board prevailed. The softest setback for our opportunity set: US Treasuries via IEF, which fell 0.7% this week. That’s a mild dip in relative terms this week, but it doesn’t change the strong bearish trend that remains in progress for IEF and comparable portfolios. Rising yields are the culprit, of course. As yields move up, the attractiveness of bonds increases for medium- and long-term horizons. Nonetheless, until we see signs that the bleeding stops (or at least stabilizes) for bond prices, it’s premature to buy the dip. That point is coming, but for now it’s best to avoid the risk of trying to catch a falling knife.

US stocks continued to sink. VTI lost altitude for a third straight week, reinforcing the suspicoun that equities, at best, will remain in a trading range for the forseeable future. Until there’s deeper clarity on the outlook for inflation, Federal Reserve rate hikes, recession risk and the war in Ukraine, strong headwinds will continue blow for the equities asset class generally. That’s a tall order and so we continue to manage expectations down for stocks in general.

The biggest loser for our opportunity set this week: shares in Africa. AFK gave up a hefty 6.4% this week, although the ETF continues to trade in a range. Let’s see if it can break above (or below) that range in the days and weeks ahead.

All our portfolio strategy benchmarks took a beating this week. In keeping with recent history, the equal-weighted mix of global stocks, bonds, real estate and commodities continued to outperform, but via losing less for this week. That still leaves Global Beta 5 EW (G.B5.ew) with a fractional gain on the year. For details on the benchmark designs, see this summary.

By contrast, the rest of the field is deep in the red. The unmanaged Global Market Index (GMI), which holds all the major asset classes based on market-value weights, has shed nearly 11% so far in 2022.

GMI’s hefty year-to-date loss suggests that aggressive, effective risk-management is probably the only thing standing between gains and losses for multi-asset-class portfolios this year. ■