The ETF Portfolio Strategist: 22 September 2021

Introducing Fortis and Altus -- A Pair Of Active Asset Allocation Strategies

And now for something completely (or at least partially) different: The ETF Portfolio Strategist herewith rolls out two actively managed strategies that will be periodically updated and discussed on these pages. Why would we do that? So glad you asked.

First, this is primarily an academic exercise to keep the little grey cells (as Hercule Poirot liked to refer to his wetware) in tip-top condition in matters of portfolio strategy analysis. The routine of thinking through why you would add or remove an asset (or assets), change the weights, rebalance (or not), etc., is valuable as a workout for maintaining a certain skill level for managing asset allocation. The real-time challenge of rationalizing portfolio shifts also toughens up the defenses in matters of keeping behavioral risk at bay as it applies to the little grey cells.

Even if your investing plan is 100% quantitative and rules-based, the markets are forever testing your mettle to stay the course (or not). Working through an ongoing set of actively run portfolio challenges helps maintain an edge and provides feedback and perspective — or at least that’s the plan.

Second, Mr. Market’s criticism is the raw material for upping one’s game. There’s an old saying that the only way you ever learn anything is through mistakes.

The intention, of course, is to never make mistakes. Don’t hold your breath. But I expect that there will be enough successes to report a slight edge through time with the pair of portfolios outlined below. Of course I’d say that. Only time will tell.

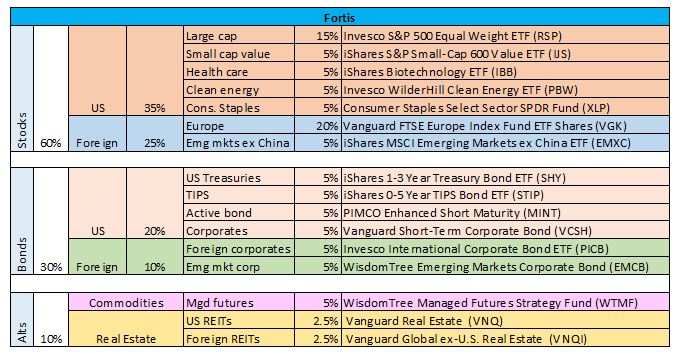

Meantime, allow me to announce Fortis and Altus. Fortis is relatively defensive, taking risks where the potential payoff looks reasonable, and otherwise pulling back and favoring defense in some way.

Altus, by contrast, is more aggressive and expects to suffer deeper drawdowns and otherwise take us on a roller-coaster ride at times. The plan is that the rougher short-term rise will pay off over the longer run.

The benchmark in both cases is our standard Global Beta 16 portfolio (G.B16). For details, see this summary. Neither Fortis or Altus will be constrained by G.B16’s asset mix and weights, but the benchmark will provide context for deviating from the “standard” asset allocation, which both strategies will do frequently. On that note, here’s how G.B16’s target weights stack up:

The main tools for delivering the goods via Fortis and Altus will be 1) adjusting the big-picture asset allocation — US stocks vs. US bonds, for instance; 2) venturing further afield from G.B16’s opportunity set (per the tickers above) into ETFs that slice and dice global markets on a more granular level; and 3) shifting to “safe” assets in a relatively aggressive manner when/if the need arises.

G.B16, of course, is a forever risk-on benchmark that holds a static set of ETFs and rebalances to the target weights every Dec. 31.

Fortis and Altus will be under no such restraints. But every strategy has to start somewhere. Let’s start with the following allocations, which apply as of today’s close (Sep. 22, 2021) — the inception date.

Why these allocations and these weights? We have our reasons, and it all boils down to expectations that the two portfolios strike us as attractive for achieving the objectives of capturing most of G.b16’s return (if not outperforming) with substantially less risk (via Fortis) while substantially outperforming G.B16 with similar (or lesser) risk (via Altus).

Going forward, I’ll provide more detail on the rationale for the funds, along with any portfolio changes as the unfold. Meantime, best wishes to Fortis and Altus as they take the first step down the market’s yellow brick road. But be careful boys: lions, tigers and bears are everywhere these days. ■