The ETF Portfolio Strategist: 23 APR 2023

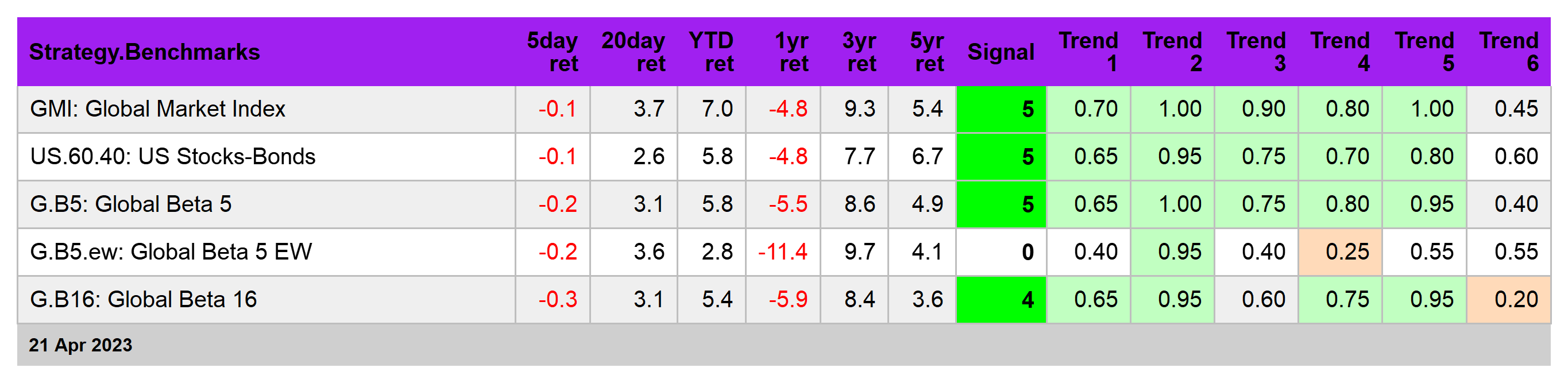

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Markets are looking for guidance, unsure of whether the near-term outlook skews bullish or bearish by more than trivial degrees. There’s a stronger case for expecting trouble, but investors writ large are reluctant to buy in to a gloomy forecast without clearer signals. At the same time, the crowd isn’t ramping up its risk appetite. The year-to-date rallies for most markets are intact, but the heavy lifting for the gains came earlier in the year and more recent trading is just coasting on previous rallies.

Debate about what comes next is keeping prices in a holding pattern. Consider US equities (VTI), which continued to churn in a tight range last week.

A similar story applies to US Treasuries (IEF).

Ditto for our 16-fund global opportunity set: the G.B16 benchmark is holding on to recent gains, but for the moment is going nowhere fast. See this summary for design details on the strategy benchmarks and this summary for how the metrics in the tables below are calculated.

European equities (VGK) are an outlier. Shares in this corner gained 0.6% last week and the technical picture continues to reflect an upside trend. Meantime, VGK is currently posting the strongest Signal score — an all-out bullish 6, per the table below.

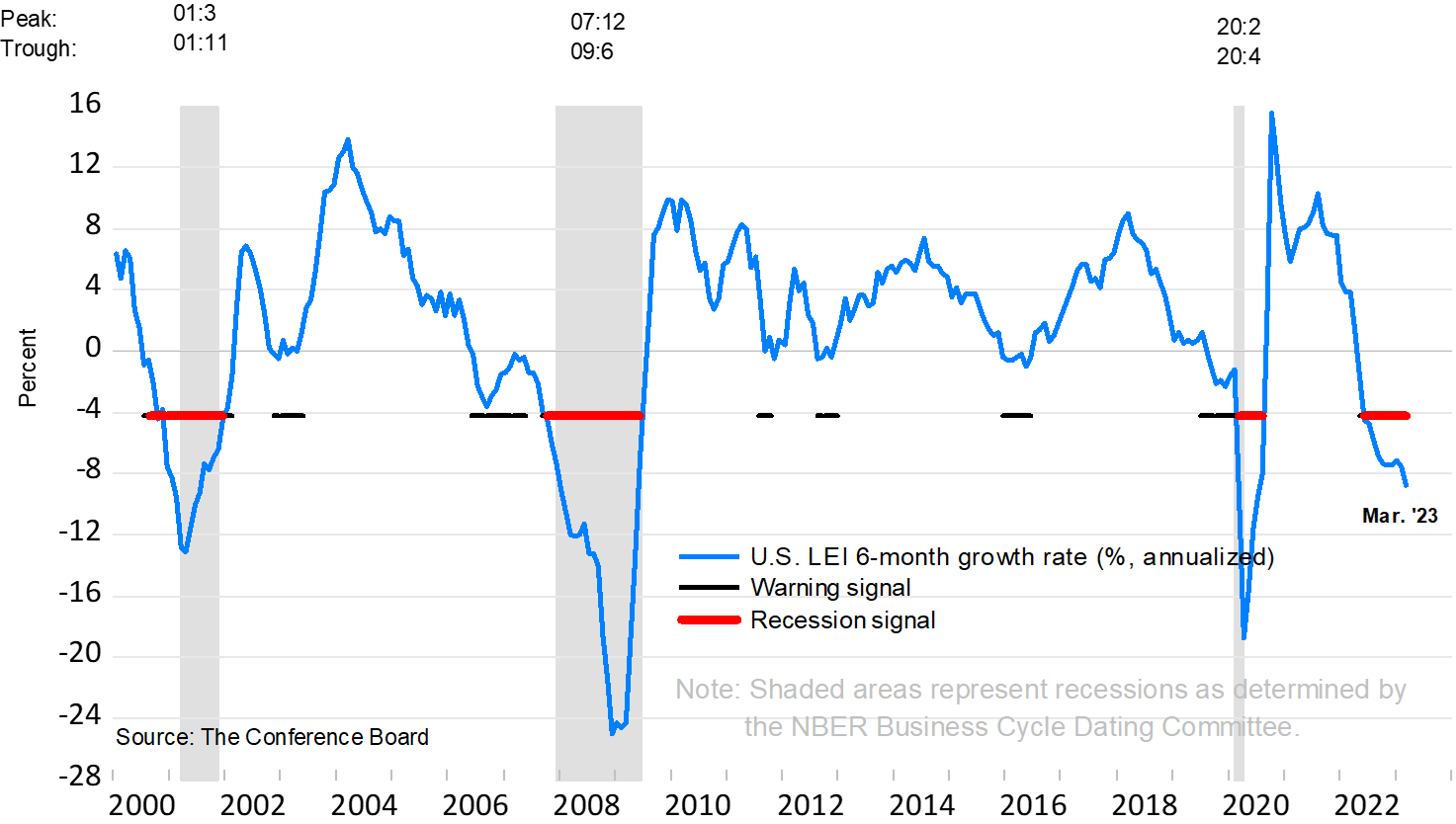

But if there’s a reason to stay defensive, the mixed messages re: the US economy are at the top of the list. The Conference Board reports that its Leading Economic Index continued to slide deeper into the red in March, signaling elevated recession risk.

But the view is decidedly brighter based on survey data for April, according to S&P Global Flash US Composite PMI. “Stronger demand conditions support sharper growth in April” while inflation momentum eased, the consultancy said of its GDP proxy.

The incoming data will soon declare one side or the other the winner… or will it? The possibility that the economy continues to sidestep a recession with modest and perhaps stall-speed growth is a plausible alternative scenario. Let’s see if this week’s first estimate of Q1 GDP changes the calculus. The consensus forecast sees output downshifting to 2.0% from 2.6% in Q4. That’s in line with my current median Q1 nowcast (drawn from several models), per today’s update for The US Business Cycle Risk Report.

Meantime, the Federal Reserve is still expected to raise interest rates by a quarter point at the upcoming FOMC meeting on May 3. Fed funds futures are currently pricing in a near-90% probability that the modestly hawkish policy stance will become a bit more so next week.

The Treasury market, by contrast, is still erring on the side of peak rate hikes and that the expected increase on May 3 will be the last. That’s the current implied view of the 2-year yield, which is widely seen as a proxy for policy decisions. Of course, the 2-year yield recently predicted a peak was near only to learn that the Fed heads didn’t get the memo and continued raising rates. Will it be different this time?

While we’re asking questions, add this one to the list: Is it time go risk-on in more than a trivial degree? I’ll take a pass, again. There are too many non-trivial uncertainties swirling for my money and so I’m still comfortable with a defensive bias. I’m starting to rethink the case that a US recession is near and that instead we’ll see a drowsy expansion stumble on. That may be enough to convince the Fed to pause, but it’s not yet compelling enough for your editor to go risk-on. ■