The ETF Portfolio Strategist: 24 JUN 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

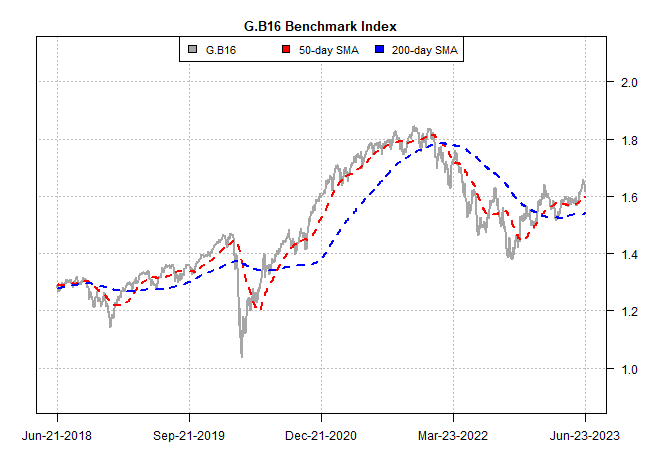

Global markets corrected this week, weighing on every slice of our 16-fund global opportunity set (G.B16). The selling was moderate and orderly, pulling the Global 16 benchmark down by 2.5%. That still leaves the index up a respectable 6.4% year to date. But uncertainty about inflation’s persistence still lurks, along with questions about what that means for policy decisions by central banks in the months ahead. It’s reasonable to assume that markets will consolidate recent gains and hold in a trading range for the near term until there’s a new catalyst for good or ill. See this summary for design details on the strategy benchmarks and this summary for how the metrics in the tables below are calculated.

Adding to the case for a pause in the recent rally is news that Russia is now struggling to suppress an internal rebellion launched on Saturday (June 24) by the shadowy Wagner paramilitary group. As of this writing, Wagner forces are heading to Moscow after reportedly taking control of military headquarters in Rostov-on-Don, a city 660 miles south of Russia’s capital. It too soon to know how this evolving situation will develop, or what it means for Russia, Europe and beyond. Meantime, until there’s clarity on this front the crowd may be inclined to remain defensive and extend last week’s selling.

The case for a pullback looked compelling a week ago. US stocks (VTI), for example, rallied for five straight weeks through June 16, posting a 15% year to date gain at that point after rising for much of the time since mid-March low. Against that backdrop, last week’s 1.6% slide for VTI is hardly surprising.

Signs that the US economy is cooling added to the sense that stocks got ahead themselves. The US Composite PMI (a GDP proxy) eased in June to 53 from 54.3 previously. That’s still above the neutral 50 mark, but this month’s dip aligns with other estimates that point to a modest expansion at Q2’s end. The Atlanta Fed’s GDPNow model estimates Q2 growth at 1.9% (seasonally adjusted annual rate). That’s an improvement over Q1’s 1.3% rise in GDP, but given the uncertainty of nowcasting it’s reasonable to assume that any pickup in next month’s GDP report will be marginal.

My guess is that markets will take a wait-and-see position in July as the crowd awaits new inflation numbers for clues on the Federal Reserve’s next moves for interest rates. Fed funds futures are still pricing in moderately high odds for another 25-basis-points hike at the July 26 meeting, followed by a pause at the subsequent announcemet in September. Let’s see if that changes after the US consumer inflation report for June (June 12) is published.

Meantime, the news from Russia will likely dominate news headlines and market activity for the immediate future. This fast-moving story has the potential to be a far-reaching event, for the war in Ukraine and within Russia itself. It could also fade quickly if Russia’s military reasserts control.

Meantime, Putin looks more vulnerable and world markets won’t be able to look away until resolution, one way or the other, emerges.