The ETF Portfolio Strategist: 24 MAR 2024

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Ride the wave.

That sums up the current state of affairs for global asset allocation strategies, which continue to mint positive returns. Meanwhile, contrarian-minded investors are struggling with the only game left on their side of town: Wait for a bearish catalyst.

There’s no shortage of possibilities — war, inflation, high levels of debt, take your pick. But from a US perspective, the one-two dance of AI-driven enthusiasm and no sign of recession on the near-term horizon is a tough act to beat.

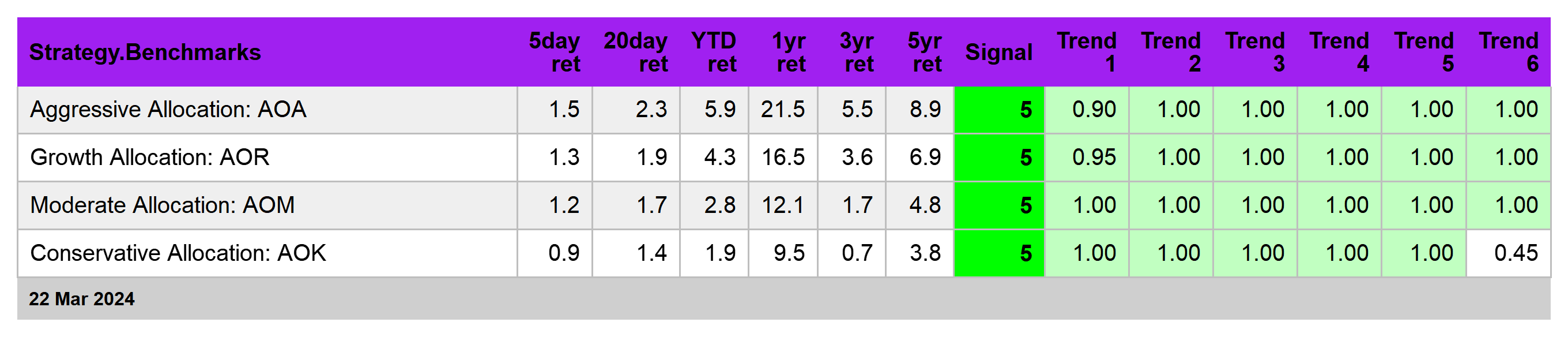

Last week certainly looked encouraging from a trend perspective as all four flavors of asset allocation strategy via the four ETFs listed below rebounded, and then some, from the previous week’s setback. With no red ink on the trailing windows for the time periods shown, the Signal score (which summarizes the trend bias in recent history) continues to print at 5, one notch below the highest bullish reading. See this summary for details on the metrics in the tables below.

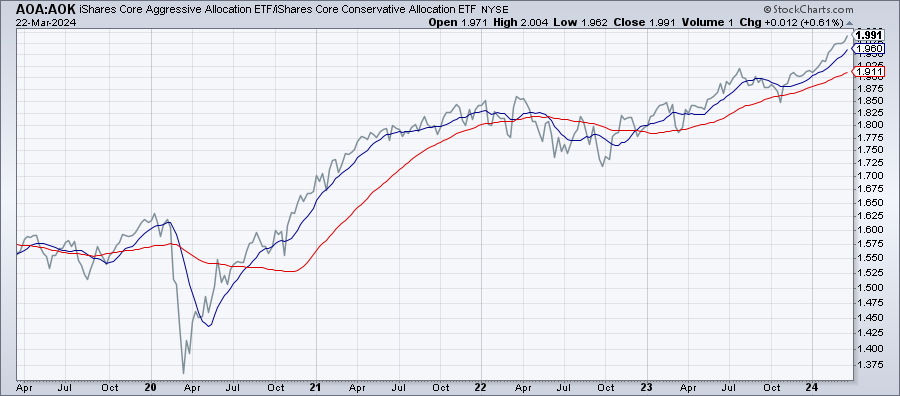

A quick glance at the iShares Aggressive Allocation ETF (AOA) reminds that the upside bias since last November is at once persistent and potent as the fund closed last week at a new record high.

Turning to the ratio of aggressive to conservative asset allocation strategies (AOA vs. AOK) highlights the acceleration in the relative strength of higher risk portfolios vs. their defensive counterparts.

The main takeaway: Global markets are on a roll and the implication is that the trend strength will continue until further notice. What the catalyst (or catalysts) might be that punch sentiment in the mouth is a popular talking point, but no one knows either why or when the crowd will abandon the bull run in progress. Indeed, by some accounts, its unclear why investors have been so bullish thus far.

Taking a more granular view of global markets reminds that the party from the 30,000-foot view is considerably more nuanced when you zoom in on the particulars. The weakest slices at the moment: foreign bonds in developed (BWX) and emerging markets (EMLC), the last of the net-negative Signal scores for this cycle.

At the opposite end of the spectrum: stocks in Japan (EWJ), US equities (VTI), including small caps (IJR), US junk bonds (JNK) and European stocks (VGK) are leading the charge for the bulls with red-hot 6 Signal scores.

Note, too, the recent recovery in commodities (GCC) has revived the positive aura for the asset class, which now sports a strong 5 Signal score.

Meanwhile, US Treasuries (IEF) continue to confound the crowd on the question of whether the bear market for government bonds has run its course. Hope revived earlier in the year in the wake a solid bounce off the low of late last year.

A key issue that’s keeping bond investors in a wait-and-see mode is the outlook for rate cuts, which earned a fresh round of optimism after last week’s somewhat bullish FOMC meeting, when Chairman Powell kept dovish policy forecasts on the table. Ditto for the new rate projections from Fed officials, who still anticipate rate cuts later in the year despite hotter-than-expected inflation data so far in 2024.

Using IEF as a proxy for bond-market sentiment, however, suggests that the crowd is still wary. IEF looks set to trade in a range until the outlook for policy and interest rates clears a bit. When and how that might happen is still a guessing game, in part because November’s election, with each passing week, is becoming a factor that’s muddying the waters.

Nonetheless, Fed funds futures are pricing in a roughly 75% probability that the Fed will cut its target rate at the June 12 FOMC meeting. But having been burned before with premature rate-cutting forecasts, the bond market doesn’t appear ready to go all-in on the current estimate, at least not yet. IEF, as a result, looks set to churn until there’s fresh news/analysis that changes the calculus.