The ETF Portfolio Strategist: 25 MAY 2024

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

After four weeks, the latest rally ran out of road. It’s premature to say that the bull run has hit a wall. A safer view, for now, is that the rally is digesting its recent gains, as technical analysts like to say.

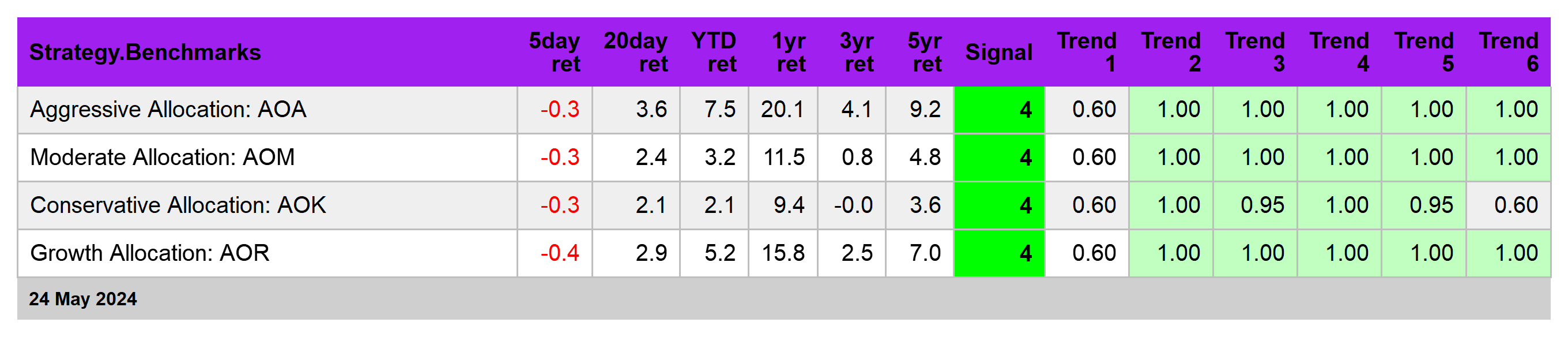

For those who favor trend signals, there’s certainly a case for keeping the faith. Our proprietary momentum scoring ticked lower for a set of global asset allocation ETFs through Friday’s (see table below), but continue to print at a moderately bullish 4 reading. See this summary for details on the metrics in the tables below.

Nonetheless, the trend still looks solid. Consider iShares Aggressive Allocation (AOA). Although it eased 0.3% for the week, the upside bias continues to impress.

Green also dominates the major components of the world’s markets via our Signal score, per the table below.

Digging into the weeds a bit, the trend bias looks quite strong for several markets, including the recent recovery for stocks in Africa (AFK).

International high-yield bonds (IHY) reflect a milder bull run, but one that arguably appears more stable (and therefore enduring?) as the fund trades near a 2-year-plus high.

It’s also too early to count out US stocks. Although Vanguard Total US Stock Market ETF (VTI) ticked lower for the trading week (the first weekly decline since the sharp mid-April selloff), the trend still looks friendly in this corner as well.

The bond market, by contrast, is still the problem child, US Treasuries in particular. The recent rally fizzled last week as economic data suggested the US economy remains resilient. PMI survey data reported that output in May rose at the fastest rate in more than two years, helping raise fresh doubt that the Federal Reserve would be able to cut interest rates in the near term.

Fed funds futures are currently pricing in odds that equate with a coin toss for the first cut to arrive at the Sep. 18 FOMC meeting, but bond investors decided it was timely to discount the rate-cut prospects a bit more. In any case, the recent rally for iShares 7-10 Year Treasury Bond ETF (IEF) never looked convincing even before last week’s downshift. IEF has yet to break out of its path of lower highs and lower lows — a trend that’s prevailed for much of the past four years.

What would change the bond market’s fortunes and reverse its long-running slide? Two factors top the list: inflation and recession. Although disinflation is still intact, the pace of inflation’s taming has yet to fully convince the Fed (or bond investors) that a return to the central bank’s 2% target is near (or even invetable, to cite the more extreme bond bears).

To be fair, the April reading of consumer price inflation was mildly encouraging in favor of disinflation and so there’s still a case for cautious optimism. But most analysts expect that further progress on inflation will be slow at best, which isn’t likely to snap the bond market out of its gloomy mood any time soon.

A recession, on the other hand, would likely boost bond prices in a way that the recent disinflation trend hasn’t. But economic data still signals moderate growth for the near term and so the bond market will likely struggle to rally based on a dramatic shift the economic trend. The Atlanta Fed’s GDPNow model, for instance, is currently projecting second-quarter growth will accelerate to 3.5% (seasonally adjusted annual rate), more than double Q1’s sluggish 1.6% increase. If correct, Q2 will mark the first quarterly acceleration in economic activity in a year.

If anything close to that pace is accurate, the best the bond market can hope for at this stage is treading water. Then again, given the severe bear market that fixed-income securities have suffered over the last several years, going nowhere would be progress. All the more so if buy-and-hold investors clip coupons by loading up on, say, a 1-year Treasury Note, currently yielding 5.21%, or roughly half the stock market’s long-run return.