The ETF Portfolio Strategist: 26 Jun 2022

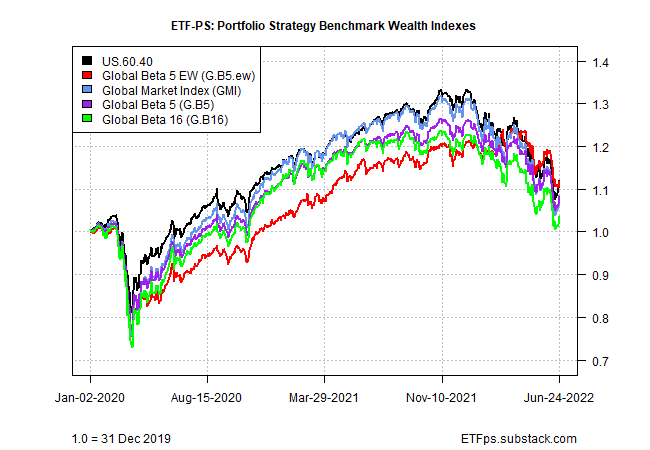

Portfolio Strategy Benchmarks

Most global markets rebounded last week

All our strategy benchmarks jumped too

It was a week of relief. Whether it’s more than a temporary pop in an ongoing bear market remains to be seen. But for the moment there was more upside than downside for the trading week ended Friday, June 24.

Some of the hardest-hit slices of global markets this year posted the biggest gains. At the top of our 16-fund global opportunity set: US real estate investment trusts (REITs). For details on the metrics in the table below, see this summary.

Vanguard Real Estate (VNQ) surged 6.8%. Impressive, but it doesn’t change the bearish outlook for the fund, at least not yet. Perhaps it’s the start of better days ahead for the ETF. But you can’t tell much from one week, even a week with a stellar rally.

US equities also posted a sharp bounce last week, but a similar caveat applies. Vanguard Total Stock Market (VTI) roared higher by 6.7%, but it’ll take time to determine if we’ve seen the bottom.

The future’s always uncertain, but staying defensive still looks prudent until: 1) there are clearer signs that inflation’s peaking; 2) the Fed considers pausing if not reversing its rate-hike policy; 3) recession risk stops rising or there’s more support for thinking that an economic downturn would be relatively mild and brief. On all of these fronts, it’s still early for making high-confidence forecasts in favor of calling the recent equity market low as the trough for this cycle.

Meanwhile, there’s no shortage of analysts advising that the latest bounce in stocks should be viewed within the context of an ongoing bear market. They could be wrong, of course, but if you that’s your view then it’s important to understand their reasoning and explain (if only to yourself) the case for thinking otherwise. For example:

“We believe that bounce in U.S. equity markets over the past three trading days has been a bear market rally off deeply oversold conditions,” writes Wolfe Research’s Chris Senyek. “While there may be some additional near-term follow through, we believe that our intermediate-term bearish base case remains intact and that the next leg down is going to be driven by rising recession risks and downward earnings revisions.”

Meanwhile, the formerly high-flying commodities sector has hit turbulence. WisdomTree Commodity Index (GCC) fell sharply for a second straight week, tumbling 3.4%. If recession risk is rising, as it is, demand for commodities will weaken. How far it weakens depends on how deep and long the recession runs. There’s a case for reserving judgment about whether a US recession is baked in or not, but commodities now appear to be pricing in the risk at a higher level. Unless you’re0 confident that demand destruction will be minimal, taking some profits after a two-year-plus bull run in raw materials looks compelling.

Rebounds in most global markets lifted all of our strategy benchmarks last week, in some cases sharply. The markets-weighted Global Market Index (GMI) led the way with a stellar 4.4% weekly advance. The weakest bounce was in Global Beta 5 EW (G.B5.ew), which equal weights global stocks, bonds, REITs and commodities. For details on the benchmark designs, see this summary.

Note that all of benchmarks remain significantly in the red year to date. For the moment, it’s reasonable to assume that the selling wave is in remission. A cure, by contrast, still lies ahead. ■