The ETF Portfolio Strategist: 27 May 2022

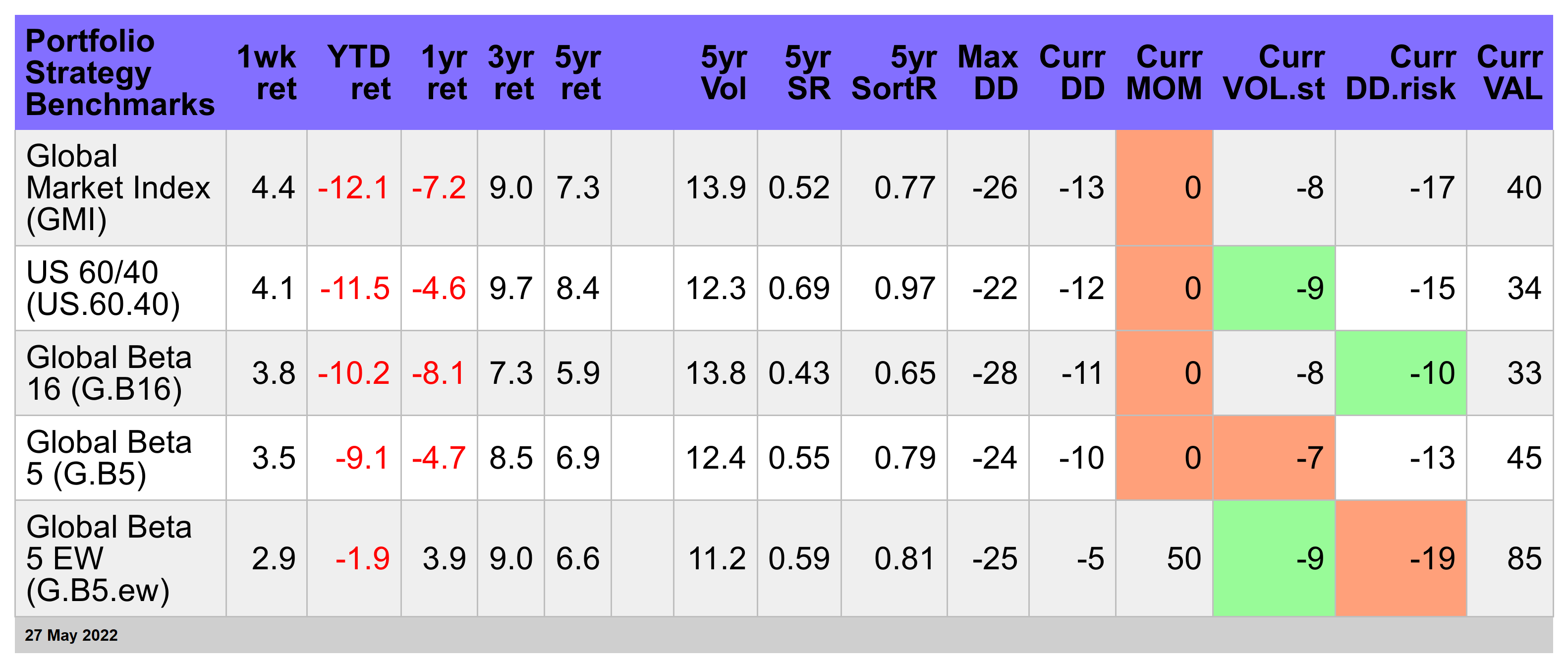

Portfolio Strategy Benchmarks

Programming note: Your editor is set to embark on a holiday excursion and so The ETF Portfolio Strategist will be on hiatus for the next two weeks, returning to the usual routine on Friday, June 10.

US stocks rally, posting first weekly gain in two months

All our strategy benchmarks popped this week

It happened… finally. US equities ended the week on an up-note. For those keeping score, this is the first rise in eight weeks.

Encouraging, but one week a trend does not make. Is the correction over? Hold that question as we wait for something resembling a persuasive answer. Meanwhile, US stocks go into the long holiday weekend in America with a reason to celebrate. Come Tuesday, the question returns: Is the bounce a sign of things to come or just noise in an ongoing slide? Unclear for now, no matter how many hot dogs and hamburgers you consume over the next several days in honor of Memorial Day. For details on the metrics in the table below, see this summary.

Looking at a broad proxy for US shares (VTI) suggests it’s premature to conclude that the downside bias has run its course. A 6.5% surge takes some of the sting out of the last several months, but the techinical tea leaves still leave room for doubt that it’s all sunshine and candy from here on out.

But hope is alive and kicking. “We have come a long way down pretty fast and if we can stabilize here then the declines we’ve seen might be all that’s needed, or something close to that,” says Tom Martin, senior portfolio manager at Globalt Investments.

Meanwhile, a minor milestone arrived with everything rallying this week, based on our 16-fund opportunity set in the table above. That includes the recovering Treasuries market: iShares 7-10 Year Treasury Bond ETF (IEF) jumped for a third week, rising 0.6%.

The optimistic view that’s partly driving the bond rally: inflation has peaked and so the pressure on the Federal Reserve to lift interest rates will ease in the weeks and months ahead. The latest round of support for going down this rabbit hole comes via the April numbers on consumer spending and income, which includes so-called PCE inflation. Core PCE (reportedly the Fed’s preferred inflation measure) eased for a second straight month for 4.9% year-over-year pace.

There are hints at peak inflation from other sources, including the Dallas Fed’s trimmed mean PCE, which is also reflecting a degree of deceleration.

There’s also growing evidence that the economy is slowing, despite expectations for a rebound after the first-quarter’s contraction. Some economists see a soft landing in the cards rather than a recession, but either way there’s a new narrative for bond bulls to chew on.

A slowdown rather than recession might deliver the best of all worlds for stocks and bonds. But the idea that the economy can cool while avoiding a contraction, take the edge off inflation and convince the Fed to ease up on tightening monetary policy is asking for a lot. The first stress test arrives with next week’s payrolls data for May. Right on cue, economists expect a softer pace of hiring, but not enough to juice recession fears. Let’s see if the numbers play along.

Across-the-board gains for our strategy benchmarks: The unmanaged, market-weighted Global Market Index (GMI) rose the most for our portfolio yardsticks, surging 4.4%. GMI is still in the red this year by 12.1%, but this week’s rally clawed back a decent chunk of the loss.

The equal-weighted Global 5 EW (G.B5.ew) also rose, but the equal-weighted edge that’s been so helpful in recent history couldn’t compete this week. G.B5.ew added 2.9%, the softest gain for the strategy benchmarks. Then again, G.B5.ew continues to post the lightest loss year to date — less than 2%. The more traditionally weighted counterparts may or may not be poised to recover lost ground in the months ahead, but whenever the rebound arrives they’ll have a long road ahead to pull even with G.B5.ew. ■