The ETF Portfolio Strategist: 27 Nov 2020

Déjà vu All Over Again: The trading week was pinched by the Thanksgiving holiday, but that didn’t slow the market leaders. For a second straight week, South American shares led the horse race, based on our ETF proxies for the major asset classes at today’s close (Nov 27). In second place, again: small-cap US shares.

The iShares Latin America 40 (ILF) surged 5.2%, its highest weekly close since early March – the eve of the coronavirus crash. ILF has been higher for four weeks in a row, although the nearly 20% year-to-date loss suggests the rally could have room to run.

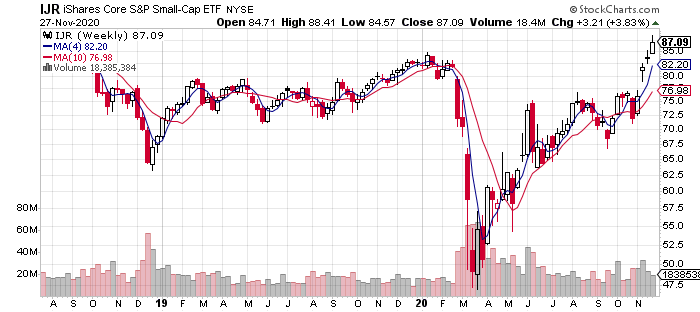

In second place this week: iShares Core S&P Small-Cap ETF (IJR), which jumped 3.8%. The rally lifted the fund to a new record weekly close, which suggests that this corner of the US equity market has caught fire and is poised for even greater heights.

Small-caps also continued to outperform the broad US stock market (VTI) for a third week. Year to date, US shares overall are well ahead of small caps. But the recent persistence in the small-cap rally is stoking the narrative that this corner of companies is gearing up for a strong 2021.

Speaking of upside momentum, all the main slices of global markets posted gains this week, or nearly so. The iShares 7-10 Year Treasury Bond ETF (IEF) was the week’s weakest performer, losing a scant 2 basis points vs. the previous Friday’s close—the only source of red ink this week. The fund has been drifting lower since September, although the dip to date has been a relatively sleepy, mild decline. Otherwise, markets near and far posted gains.

A Rising Tide Lifts All Boats (And Benchmarks): The broad-based rally once again provided a strong tailwind to our benchmark portfolios (For details on all the risk metrics as well as the strategies and benchmarks, see this summary.)

Tied for first place this week: the market-weight Global Market Index (GMI) and our spin on carving up that global market benchmark via all 16 ETFs in the chart above (G.B16). In both cases, the portfolio benchmarks rose 1.8% -- a gain that reflects a continuation and acceleration in the recent upside bias from the previous week.

Returns also improved for our proprietary strategies. Global Managed Volatility (G.B16.MVOL) and Global Managed Drawdown (G.B16.MDD) — each added 1.8% on the week. The low-key Global Minimum Volatility (G.B16.MINV) also managed to tick up 0.4%.

Note that G.B16.MVOL continues to reflect a full-out risk-on profile for its 16-ETF opportunity set (the same set of funds listed in the first table above). Ditto for G.B16.MDD, except for its ongoing risk-off position in iShares 7-10 Year Treasury Bond ETF (IEF). Otherwise, the strategy’s bullish across the board.

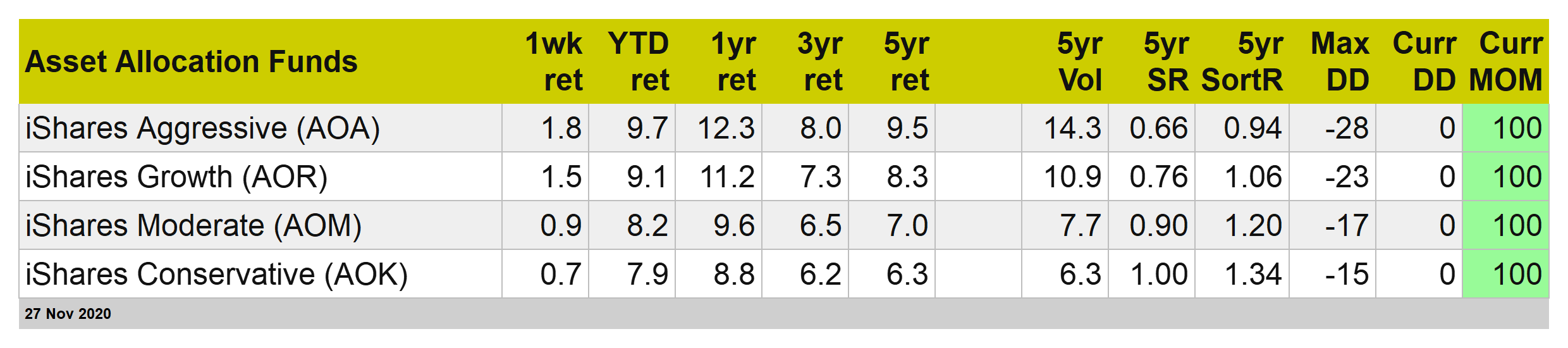

For BlackRock’s four asset allocation funds that are regulars here, results are relatively wide-ranging, from a 0.7% weekly gain for the conservative strategy (AOK) up to 1.8% for aggressive (AOA).

What’s driving risk assets higher? The crowd sees light at the end of the tunnel for the coronavirus crisis, courtesy of a number of vaccines that are reportedly close to rolling out to a small group of health care workers and other groups before the start of a wider distribution to the general public, perhaps at some point in 2021’s first half. But everyone’s buying on the rumor, which raise the awkward question: Is a correction brewing once the rumor becomes news?

The best-case scenario is that the global economy returns to something approximating the pre-pandemic era. But recall that the world before March was a low-growth/lowflation climate. Are risk assets pricing in something materially stronger? If so, that’s dicey. Repairing the damage from the pandemic will unfold far less rapidly than the US stock market’s rebound implies. To invoke the old saw, the market’s priced for perfection but we’re likely to experience something closer to a flawed recovery. ■