The ETF Portfolio Strategist: 28 APR 2024

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Risk-on sentiment rebounded after three weeks of investors playing defense. It’s too soon to know if this marks the end of the red-ink run for risk assets. Another way to put it: It’s too early to make that forecast with a relatively high degree of confidence. I’ll explain why shortly, but first let’s take a look at the numbers.

Last week’s rally gave a strong lift to our suite of proxy ETFs that track global asset allocation strategies. The aggressive allocation fund (AOA) led the rebound with a 2.0% weekly advance. Three of the four allocation ETFs returned to a moderately bullish momentum profiles via the Signal score, per the table below. See this summary for details on the metrics in the tables below.

Last week’s bounce isn’t terribly surprising when we consider that even when markets are trending lower there’s always an intermediate rally. Notably, AOA rallied after hitting its 20-week average. A fall below this level via the 5-week average tends to reflect a net bearish profile, and so the fact that the 20-week average held suggests the crowd isn’t yet ready to go all-in on a bear market narrative. (To be clear, this is one of many metrics to assess the directional bias of markets/prices; in the interest of brevity, I’m highlighting one facet of a very large toolkit.)

Several of the major components of global markets also rebounded last week. As of Friday’s close, equities in Asia ex-Japan (AAXJ) are starting to look firmer after trading in a range for much of the past year-and-a-half. US stocks (VTI) also firmed up, moving back into a bullish posture, based on our Signal score (see table below).

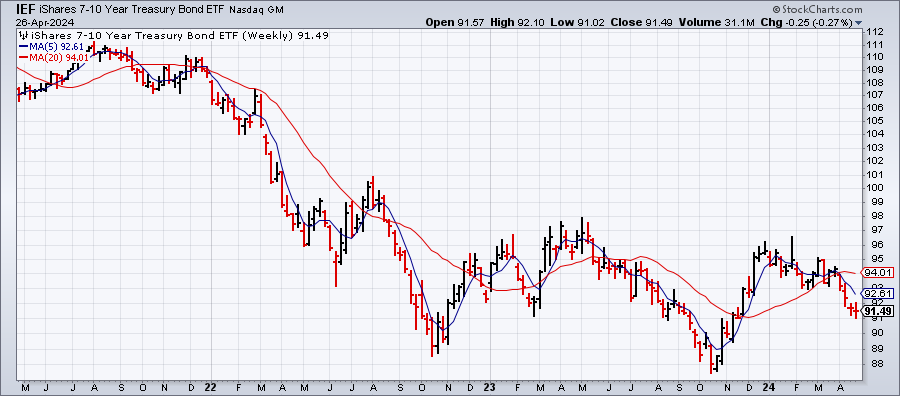

Among the stronger consistencies of late, at a time of mixed trend profiles for stocks near and far: the persistent bullish trend in commodities (GCC) and the a non-stop bearish reading for US Treasuries (IEF).

Although commodities (GCC) pulled back slightly last week (after four straight weekly gains), the trend still looks solidly positive. The question is what’s the catalyst that could drive commodities higher still? Geopolitical risk remains on the short list. Less compelling is the view that global economic growth is set to ramp up. I don’t see global output slipping into recession territory in the near term, but neither do I see it accelerating sharply from current levels. All of which pushes me toward a neutral outlook on commodities, despite the firmer trend of late.

By comparison, US Treasuries (IEF) are performing a similarly consistent dance, albeit with a negative bias. I don’t expect IEF to fall below its recent troughs (roughly 87-89), but until the ETF takes out its recent high (~97-98), I’m in no rush to dive in, at least from an ETF perspective. (Opportunistic buy-and-hold strategies for individual Treasury securities, to lock in the recent rise in yields, is another matter, but that’s another story.)

Stepping back and making an informed guess about what the near-term future will bring, I’m expecting trading ranges to prevail. Markets have a lot of mixed signaling to work through on the macro and geopolitical fronts, and that will take time. From a US perspective, the key economic variable that’s animating forecasts and expectations is the state of the inflation trend.

Last week’s data updates offered more support for the sticky-inflation scenario. I’m still in the camp that expects disinflation to continue, as I explain here, but the speed of this decline has slowed to a crawl. The next several months could reveal a modest rebound in inflationary pressures, but I expect by third or fourth quarter of 2024 it’ll be clearer that disinflation still prevails.

Markets, however, will struggle to digest recent history for the rest of Q2. Given the strength of the US economy without (so far) a clear sign that inflation is heating up (as opposed to flatlining of late), the trading-range scenario looks compelling as a near-term forecast.

Add in the fact that asset allocation ETFs are still churning near record highs and the main takeaway is that the case for going all-out defensive still looks premature. Taking some profits and moderately trimming risk exposure is reasonable at this point, but for now I’m reluctant to go much further until the signaling becomes clearer.