The ETF Portfolio Strategist: 29 Jan 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

The market is usually right. Is it right this time?

If it is, a new bull run has started, or so it appears. But it’s too soon to make that call with a high degree of confidence, although after another strong week of upside trading activity we’re a bit closer to ringing the bell.

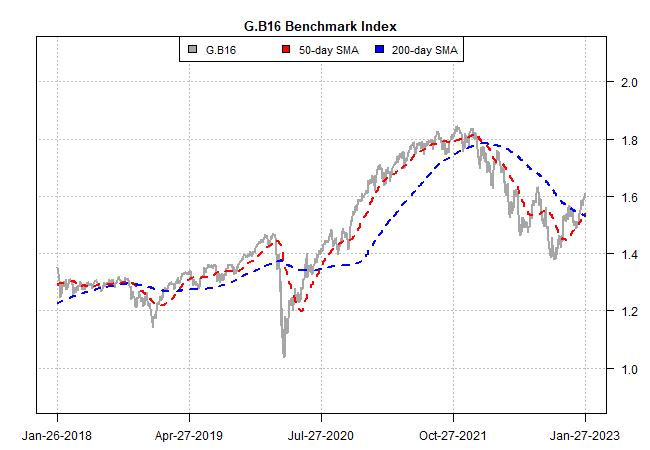

The trend change certainly strengthened to the upside for the G.B16 strategy benchmark, a quasi market-cap-weighted global mix of the major asset classes. Notably, G.B16 poked decisively above its 200-day moving average as of Friday’s close. Encouraging, but let’s see if the 50-day average follows suit, which would strengthen the bullish aura and move your editor closer to assuming that multi-asset-class portfolios will run hot for the near term. See this summary for design details on the strategy benchmarks.

For details on the metrics in the tables below, see this summary.

A key factor in the rebounding trend for G.B16 is the recovery in stocks ex-US. Shares in Asia ex-Japan (AAXJ), for example, rose for a fifth straight week. Note that AAXJ is up 13.1% for the year to date, the best performance for G.B16’s global opportunity set.

Despite the rebounds in many markets around the world in January, it’s too soon to rule out the risk that we’re in a bear-market rally. Given the length and depth of last year’s corrections it was all but inevitable that markets would bounce. The optimistic view is that markets are pricing in a mild recession, or perhaps nothing worse than a period of slow growth. That’s a plausible scenario, but it’s premature to rule out a deeper downturn, which would probably spoil the party currently in progress.

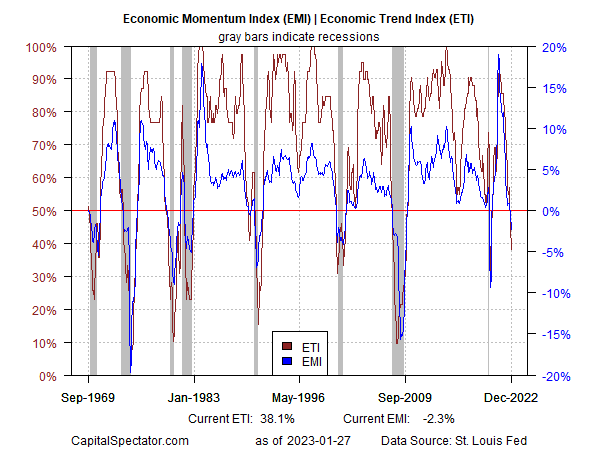

As I report elsewhere today (via The US Business Cycle Risk Report), the broad scope of macro numbers strongly point to an economic contraction that’s already unfolding for the US. A pair of proprietary, multi-factor indicators tell the story: ETI and EMI remain moderately below their respective tipping points that signal recession.

At this late date it’s unlikely that incoming data will bring upside revisions that wipe away the recession call for the US.

The best-case scenario is that the recession is so mild that it barely registers in markets. A test of that idea awaits in the week ahead, which is expected to bring news of another, albeit smaller Fed rate hike. Meanwhile, US payrolls for January are expected to slow — falling below +200k for private payrolls for the first time in two years.

If markets can rally again this week, even if economic news is bearish, that’ll be a sign that the crowd is set to run prices higher beyond January, which will send a collective signal that the worst has passed. That doesn’t mean the future can’t surprise us. But the longer the markets rally, the harder it is to be a contrarian. Your editor hasn’t given up this badge just yet, but a change in sentiment on these pages may be approaching. ■

Just joined your Substack and I’m loving the commentary. Helps me to navigate the markets and have an understanding of what’s going on in my retirement accounts.