The ETF Portfolio Strategist: 3 Apr 2022

Active Risk-Managed Strategy Benchmarks

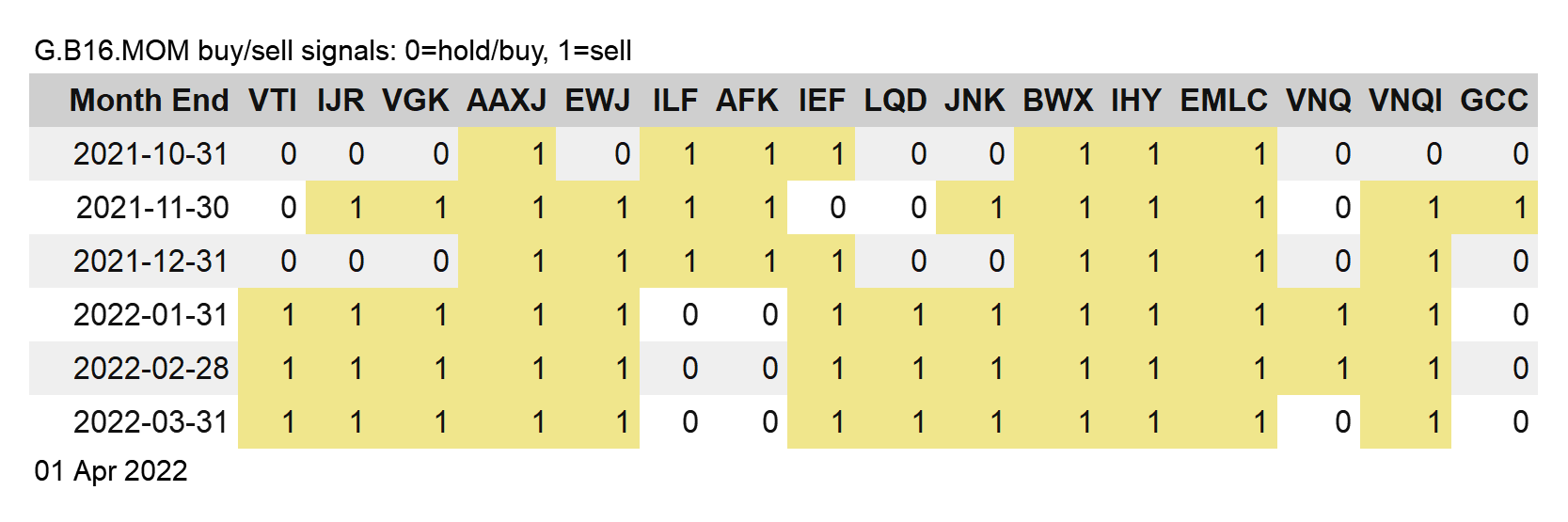

Unmanaged beta risk rebounded last week, giving our trio of risk-managed strategy benchmarks a run for their money. Global Managed Volatility (G.B16.MVOL) managed to hold steady with the benchmark, Global Beta 16 (G.B16). Otherwise, risk management fell short. For details on the strategy rules and metrics in the tables below, see this summary.

Year to date, all three active risk-managed benchmarks are still adding value, albeit by losing less money than the benchmark. For the longer term (3- and 5-year trailing periods), two of the three risk-managed benchmarks still trail.

This year will likely be a stress test for risk management generally. To wit, if you can’t add value when market volatility and geopolitical risk spike, it’s hard to imagine what type of conditions would offer an advantage for second-guessing Mr. Market’s asset allocation. ■