The ETF Portfolio Strategist: 30 Apr 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Betwixt and between risk.

The case may be weak for expecting last year’s bear market to reassert itself with clarity, but assuming that the bulls will soon back in force feels a bit premature too. That leaves your editor to inhabit the space between the two opposites and so I remain Mr. Neutral until I see more reasons to lean heavily one way or the other.

Our G.B16 benchmark, which tracks global markets via 16 ETFs, is also favoring a middle path lately. After partially recouping 2022’s steep loss, G.B16 continues to trade in a range. There are hints that it may be poised to push above recent highs, which would strengthen the bullish view. But with so many threats swirling in macro and markets I don’t feel the time is yet ripe to abandon a still-cautious outlook. Given the absence of follow-through of late for G.B16’s recent strength, I suspect that I’m not alone in preferring to wait for more data. See this summary for design details on the strategy benchmarks and this summary for how the metrics in the tables below are calculated.

But let’s be clear: my cautious stance, albeit one that’s slowly if reluctantly giving way to a bullish bias, runs counter to the data. As the tables above and below indicate, there’s more green on screen these days as more markets reflect upside momentum conditions. Downplaying the change in sentiment could incur a significant opportunity cost down the road, but I remain reluctant to throw in the towel on staying defensive until/if markets start to break above recent resistance levels. That point may be near, but not yet.

A leading counterpoint to my hesitancy to go all-in on a bullish position: stocks in Europe. Vanguard FTSE Europe ETF (VGK) ticked higher last week, marking the sixth straight weekly advance. The fund is probably ripe for a period of consolidation, but there’s no denying the upward strength that’s been unfolding for the better part of the past six months.

The recent rally in US stocks is softer by comparison, but the optimistic spin is that American shares are now set up to signal a clear path higher. The 5 print on the Signal Score for Vanguard Total US Stock Market (VTI), per the table above —second only to VGK’s 6—certainly leaves room for optimism. But with a Federal Reserve policy meeting on tap this week (May 3), and one that’s expected to reveal another 1/4-point rate hike, I’m (still) in no rush abandon my defensive posture. Perhaps Fed Chair Jerome Powell will convince me otherwise in his press briefing that follows Wednesday’s policy announcement.

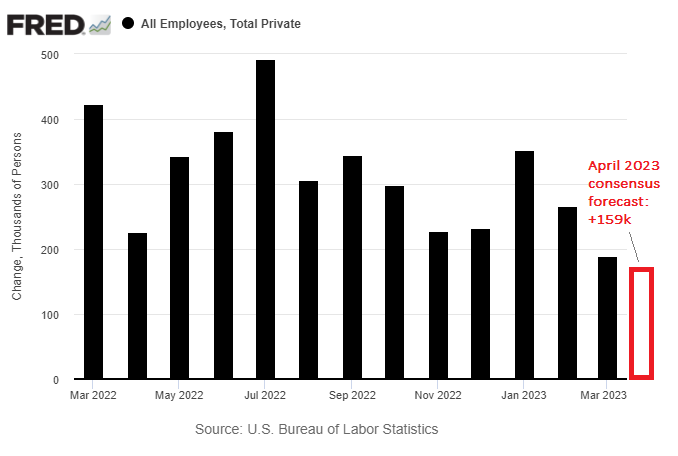

Another reason to play the wait-and-see game: April payrolls data scheduled for Friday (May 5) is expected to highlight another slowdown in hiring. The key question: If the forecast is correct, will the market interpret a weaker number as a signal that a recession is now, finally, a high-probability event in the near term? Alternatively, will the crowd see a softer payrolls number as a reason to amp up risk-on positioning on the assumption that the Fed will read the data as a reason to cease and desist with rate hikes, and perhaps start cutting sooner than recently expected?

I, for one, don’t have a good sense of how market sentiment will break. What I am expecting is that the week ahead will be a roller coaster as investors digest a Fed meeting and crucial payrolls data at a time of ongoing uncertainty re: the elephant in the room — rising risk from a possible debt-ceiling crisis at some point in the summer.

The immediate question: Will the debt-ceiling bill passed by the GOP in the House last week survive in the Democratic-controlled Senate? Probably not, but the stakes are sky high for the US economy and so nothing’s certain at this point. The impasse will be solved at some point and so the government will eventually secure a higher debt ceiling to pay the bills and keep the Treasury market away from a crisis. But getting from here to there is rife with hazards and it’s too soon to rule out an 11th-hour fix that keeps markets on edge.

One more reason that persuades me to err on the side of caution with risk exposure until the future looks, if not exactly clear, less precarious. It’s hard to say exactly what would mark such a change, but like Supreme Court Justice Potter Stewart, who famously admitted he couldn’t define obscenity, I’ll know it when I see it. ■