The ETF Portfolio Strategist: 30 JUL 2023

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Investors have been conditioned in the last several years to adopt a healthy degree of skepticism on matters economic and financial. In a world that’s reintroduced pandemic and war, inflation and political risk to formerly sanguine masses, the revival of optimism must surely be a head fake.

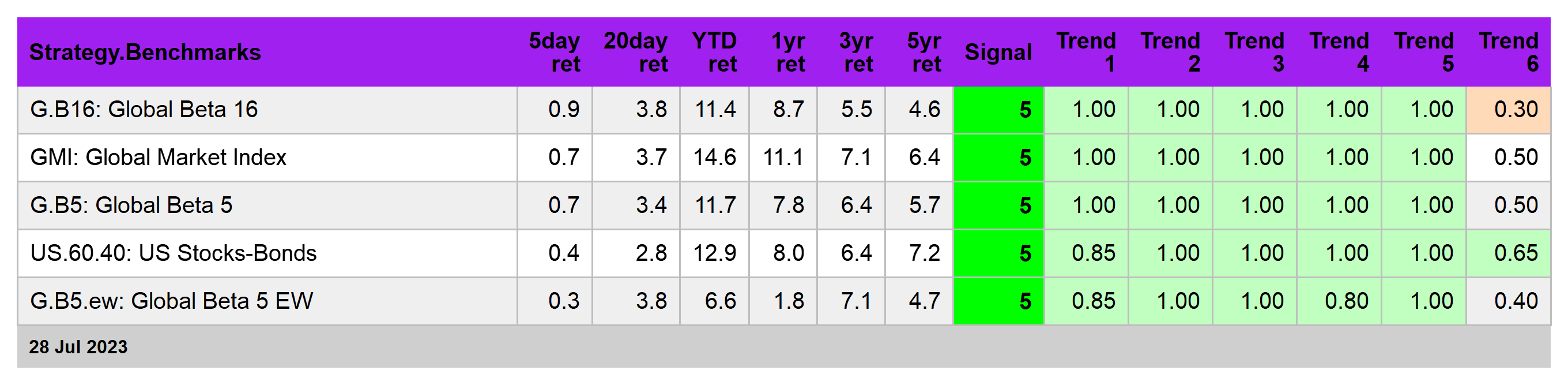

And so it may turn out to be, but for now the global markets continue to price in better days ahead. Our multi-asset class benchmark, G.B16, rose again last week as it continues to claw back 2022’s loss. There’s still a ways to go before markets fully erase last year’s head smack.

The last few miles could be rough, or perhaps further into the future than the recent rally suggests. But for now the momentum looks solid and set to persist. See this summary for design details on the strategy benchmarks and this summary for how the metrics in the tables below are calculated.

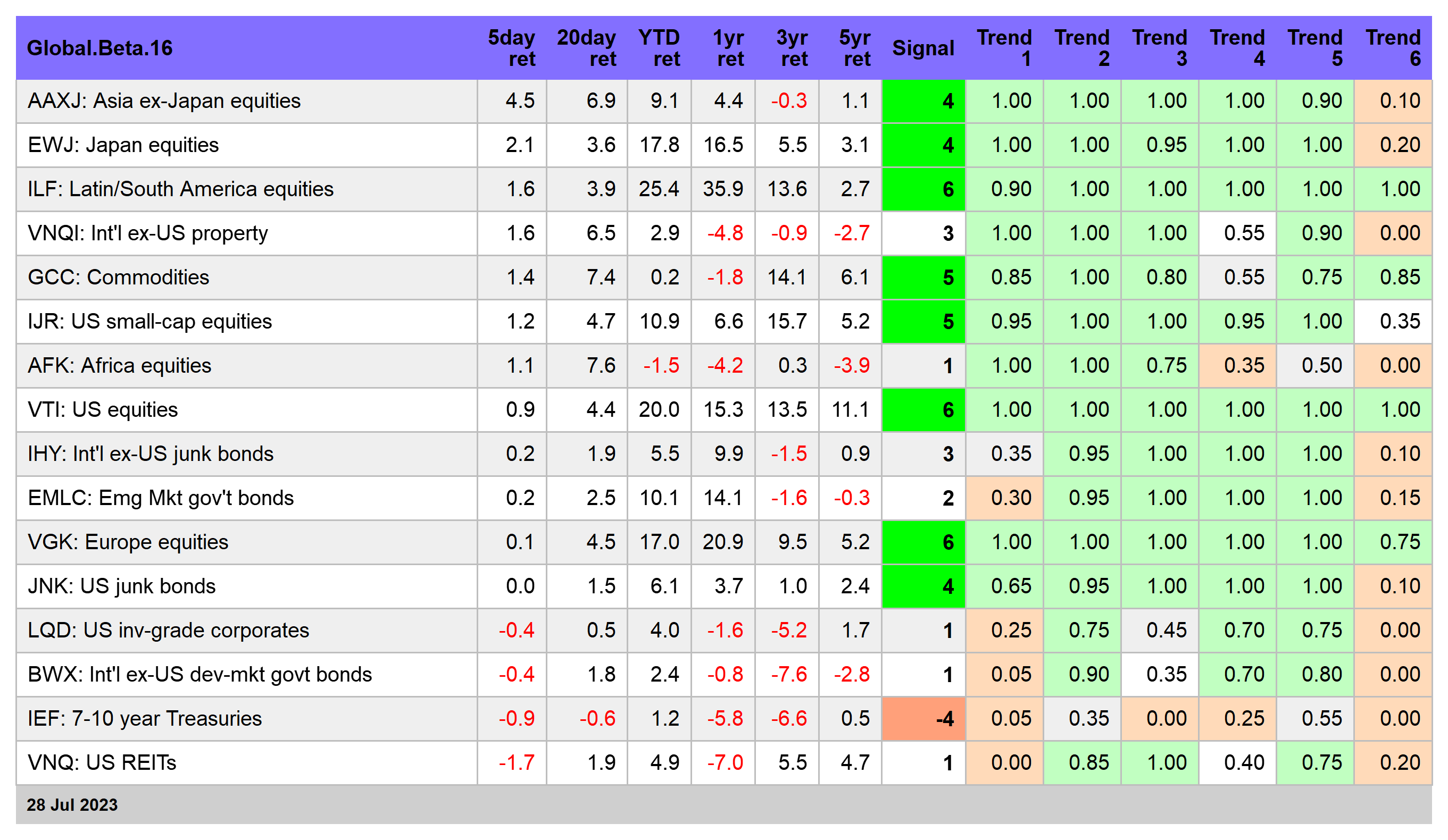

The acid test will be a decisive retaking of the previous highs, which varies from late-2021 to early 2022 prices, depending on the market or benchmark. Your editor is still persuaded that a test of those heights is near, but even so the markets are due for a breather. G.B16 is up a sizzling 11.4% year to date, or more than twice it’s trailing 5-year annualized return. Impressive and welcome, but unsustainable and so caution remains the watchword for the near term.

Ditto for US equities (VTI), which are up a sizzling 20% this year. What might drive stocks higher still? Another dose of encouraging inflation news would help, which in turn would strengthen market expectations that the Federal Reserve announced its final rate hike for this cycle last week. Fed funds futures are on board with that outlook — the current implied probability for holding pat at the current 5.25%-5.0% target range is a healthy 80%.

Avoiding a recession in the US would be a plus for equities too, assuming it doesn’t gin up higher inflation, which at the moment seems to be a reasonable forecast. Last week’s second quarter GDP report delivered the news that growth picked up while inflation eased.

Can markets have their cake and eat it too? So far, yes. The months ahead will probably be a bit tougher on delivering a Goldilocks scenario, but for now the markets are pricing in exactly that. The trick is keeping the good news rolling.

👍