The ETF Portfolio Strategist: 30 MAR 2025

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Global asset allocation is looking resilient this year. Although most strategies took a hit last week, the year-to-date results continue to show relative stability in an increasingly uncertain investment environment.

An ETF proxy for aggressive asset allocation (AOA) is posting a modest loss so far in 2025, but its three less-risky counterparts continue to post slight gains. A ho-hum result overall, except when you consider what’s going on in equities — US stocks (VTI) are down 5.3% year to date and small-caps (IJR) are in the hole by nearly 10%.

The catalyst for the selling: a growing recognition that tariff risk is non-trivial and will accentuate the headwinds from sticky inflation and slowing economic growth — a combination that suggests stagflation is becoming more likely in some degree.

The Commerce Department on Friday reported core PCE inflation (a metric that’s closely monitored by the Federal Reserve) rose at a higher-than-expected 2.8% annual rate in March. That’s still a middling pace vs. recent history, but the fact that this key measure of pricing pressure is ticking higher at a time of slowing growth doesn’t inspire confidence that the Fed will cut interest rates. Not a good look for the optimists at the start of a global trade war, which officially begins on Apr. 2, when President Trump’s tariffs are scheduled to launch.

For the moment, global asset allocation has contained much of the damage. Despite last week’s late-week selloff in stocks, only the short-term trend has turned negative for our regular set of global asset allocation ETFs. The next question: Will the red ink spill over to the medium- and long-term metrics as the tariff war kicks off?

The first line of defense for global strategies may be tested in the days ahead. Using the Global Trend Indicator (GTI) for reference, the 50-day average looks set to slip below its 100-day counterpart. (GTI aggregates the technical states of the four ETFs listed above.) If that support gives way, the trend profile will suffer. Keep in mind, however, that the 50-day average briefly fell below the 100-day average last August, a slide that turned out to be noise. The difference this time is that a significant macro risk factor hangs over the global economy in the form of trade risk.

Note, however, that GTI’s current drawdown is still a moderate -2.9%. As setbacks for global asset allocation strategies go, the damage so far has been only slightly worse than the median peak-to-trough decline since 2008.

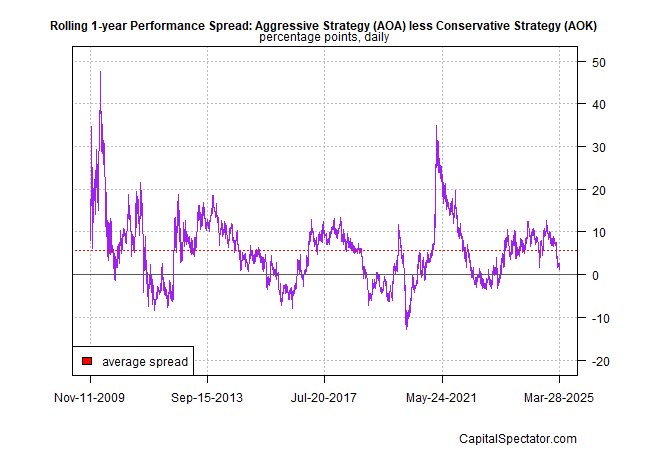

A similar risk profile emerges via the 1-year return spread for aggressive allocation (AOA) less its conversative counterpart (AOK). Although the gap is now well below the historical median for these ETFs, a mildly positive spread still prevails in favor of the aggressive mix.

The resilience of global asset allocation in the current environment is a function of widely different returns this year for the main sub-categories of the major asset classes. Notably, stocks in Europe (VGK), Africa (AFK) and Latin America (ILF) are still posting strong results year to date — 12.3%, 13.4% and 13.7%, respectively. US Treasuries remain comfortably in positive terrain for 2025 via the iShares 7-10 Year Treasury ETF (IEF), which is up 3.5% in 2025. Another moderate winner so far this year: commodities (GCC) with a 3.6% increase.

The acid test, however, still lies in the future, and the deciding factor will be tariffs. Given Trump’s mercurial habits, deciding how all this plays out is difficult in the extreme. Difficult or not, so-called Liberation Day is set to start on Apr. 2, when a new set of tariffs is scheduled to commence.

How long they last, and in what form, is open for debate. Trump has hinted that he’s open to the idea of renegotiating on the other side of Apr. 2. Then again, he’s also said that the tariffs are permanent.

Some forecasters say there’s a high risk that tariffs will push the US economy into recession, but that’s still a guesstimate whereas the hard data published to date continue to reflect a low risk that a contraction has started, as detailed in the current issue of The US Business Cycle Risk Report.

There’s also another significant variable in the mix: responses from other countries, along with second-order effects, starting with how Trump interprets the reactions. The potential for a spiraling crisis is a non-trivial threat, or so Trump’s comments last week imply:

If the European Union works with Canada in order to do economic harm to the USA, large scale Tariffs, far larger than currently planned, will be placed on them both in order to protect the best friend that each of those two countries has ever had!

The week ahead, in short, will be revelatory. Expectations for what’s revealed and how the revelations influence the outlook for markets and the economy, by contrast, is no clearer today than it was a week or a month ago.

All of which suggests that there’s still a strong case for staying diversified across asset classes and avoiding hefty bets one way or the other. ■