The ETF Portfolio Strategist: 4 Mar 2022

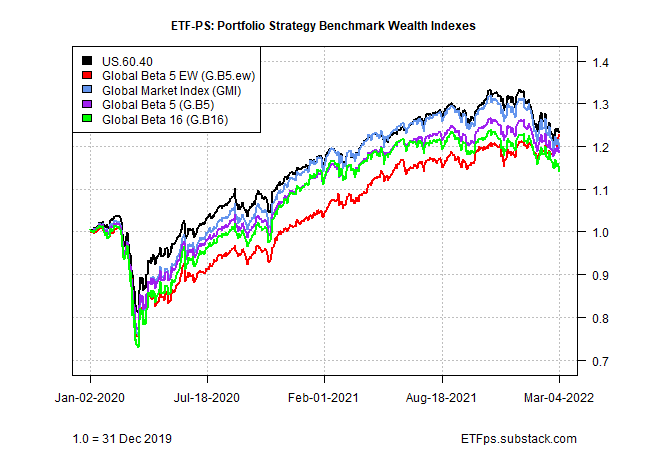

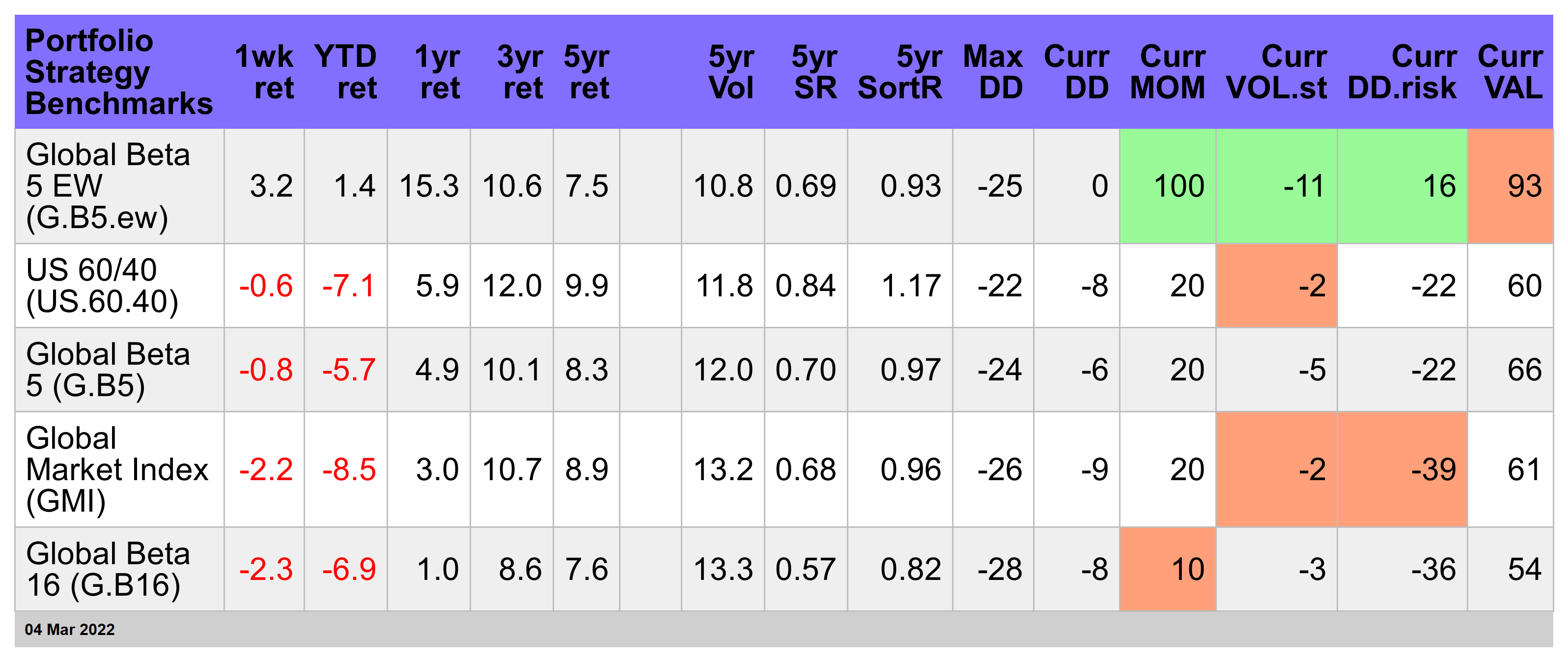

Portfolio Strategy Benchmarks

Commodities surge as war engulfs Ukraine

A strategy of equal-weighting the primary global markets pays off this week—big time

The peace dividend crashed and burned this week. Russia’s war on Ukraine became increasingly brutal and the West reacted with aggressive sanctions that convinced markets that commodities shortages would become the norm — for energy in particular — until further notice.

It was, in short, a bad week diplomacy, the rule of law and the interests of stability and order on the global stage. For commodities, by contrast, it was a bull market on steroids. For details on the metrics in the table below, see this summary.

WisdomTree Commodity (GCC), a diversified mix of raw materials, surged by an astronomical 13.5% for the week through today’s close (Friday, Mar. 4). The stellar gains of late will almost certainly reverse, and dramatically so, with the slightest whiff of a ceasefire. But there’s no sign that doves are about to fly as we write. And so commodities — and most shares related to raw materials — continue to run hot.

There are scattered reports that Russian forces are retreating in some areas of Ukraine, but for now it appears that any pullback is just a lull before new assaults are waged. As far as we can make out, the Kremlin shows no signs of abandoning its invasion.

As for GCC and commodities generally, we’re inclined to start thinking about taking some profits. We’re clueless on what happens next in Ukraine or how long the conflict lasts or what it ultimately means for markets, economies and geopolitical risk. What we do know is that massive upside spikes that are highly dependent on tomorrow’s headlines are a fragile creature and so what Mr. Market gives he can quickly take away. Caveat emptor.

Another winner this week: Latin America shares via ILF. As regular readers know, we’ve been cautiously optimistic on this fund for much of the past month or so and there’s no reason to change tack now. Indeed, ILF rallied 3.5% for the week just ended, providing some welcome ballast for the red ink that dominates most markets elsewhere. The ETF’s strength is hardly mysterious as the portfolio’s largest holdings are in the high-flying materials and energy sectors.

With war dominating the headlines this week, it’s no surprise that the the safe-haven trade for Treasuries has revived — sharply. The iShares 7-10 Year Treasury Bond ETF (IEF) jumped 2.0% this week, reversing four weeks of loss in one fell swoop. Inflation risk is still lurking, and probably more so than before, but for now the safety factor takes precedence. But beware of a dramatic reversal on this front, too, once there’s light at the end of the war tunnel, at which point Mr. Market will resume his nail-biting over inflation and related worries, perhaps with a vengeance.

The biggest loser on our 16-fund opportunity set this week: equities in Europe. No wonder — the Continent is next door to the hostilities and, if you’re prone to darker thoughts, there’s a non-zero risk that war in some form could spill over into one or more countries of the European Union. Pricing in this risk, or worse, is tricky, to say the least, but the crowd made a stab this week by giving Vanguard FTSE Europe (VGK) and hefty haircut via a 10.2% decline for the week, leaving the fund at its lowest close in more than a year.

Unfortunately, there may be more to come, depending on what happens in the days ahead. Buckle up. At some point, VGK’s dive will look attractive from a bottom-fishing perspective, but not yet. Your editor, at least, needs more encouragement that events in Ukraine appear to be moving in the right direction. For now, that point looks far off, but let’s see how the news compares at the start of next week’s trading. Suffice to say, this is a fast-moving situation and today’s logic can age at lightening speed as events on the ground evolve.

Another rough week for portfolio strategy benchmarks, with one glaring example. Our equal-weighted mix of the world’s primary asset classes — stocks, bond, real estate/REITs and commodities — continues to shine. In stark contrast with the rest of our strategy benchmarks, which take a more conventional approach to allocating across global markets, Global Beta 5 EW (G.B5.ew) posted an unusually sharp gain this week. For details on the benchmark designs, see this summary.

G.B5.ew surged 3.2% and for the year is up 1.4% through today’s close. None of the other portfolio benchmarks even come close. The reason, of course, is the use of equal weighting. Giving commodities a 25% strategic allocation (with year-end rebalancing) has become a huge winner this week.

G.B5.ew had been showing strength vs. the rest of the field in recent weeks, largely due to commodities, but the edge went into overdrive over the last several days. As with commodities, however, G.B5.ew is vulnerable to a sharp reversal of fortunes when and if peace begins to re-emerge on Europe’s far-eastern border.

Meantime, the case for considering (or at least tilting toward) equal weighting with asset allocation just became quite a bit more topical in discussions related to portfolio design. ■