The ETF Portfolio Strategist: 5 Sep 2022

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

Every slice of our 16-fund global opportunity set took a hit last week. In the previous update there were some corners that looked mildly upbeat vs. the rest of the field, but these thin counter-trends gave way in the latest round of selling. In addition to losses for all measures of risk assets in the Global Beta 16 universe, all are now posting decisively bearish Signal scores. For details on the methodology, see this summary.

Bonds of various stripes offered a degree of relief, in relative terms. Fixed-income securities issued by emerging markets governments (EMLC) edged down a comparatively modest 0.5% last week. Useful, but it’s weak tea since EMLC is still reflecting a strong downtrend that looks set to roll on.

The deepest loss for our opportunity set last week: US small-cap stocks (IJR), which suffered a sharp 5.2% decline. The price deterioration overall is comparatively light this year, based on eyeballing its chart. But our deeply bearish Signal score for IJR (-4) suggests there’s still more trouble ahead.

US stocks overall don’t look much better (-3): VTI stumbled for a third straight week and the trend continues to forecast further losses to come.

Meanwhile, US Treasuries appear set to test the lows of summer in the weeks ahead after the iShares 7-10 Year Treasury Bond ETF (IEF) slumped 1.3%.

What might clear out the dark clouds that are gathering anew over markets near and far? Encouraging numbers on next week’s US consumer inflation report for August (Sep. 13) would help by taking off some of the heat tightening at the Sep. 21 FOMC meeting. Fed funds futures are estimating a 60% probability for a 75-basis-points hike. CPI data that strengthens the case for seeing peak inflation in the rear view mirror would cheer the markets, if only on the margins by leaning more toward a 50-basis-points increase.

Even in the best of circumstances there’s still a rough road ahead. A number of models and forecasts of late put the terminal Fed funds rate at roughly 4%, which is still well above the current 2.25%-to-2.50% range. According to one strategist, history advises that the Fed funds rate has to fall below the year-over-year pace of headline CPI before the central bank starts to ease up on policy tightening. Given that CPI is running at 8.5% through July, looking for a bottom in markets still feels premature.

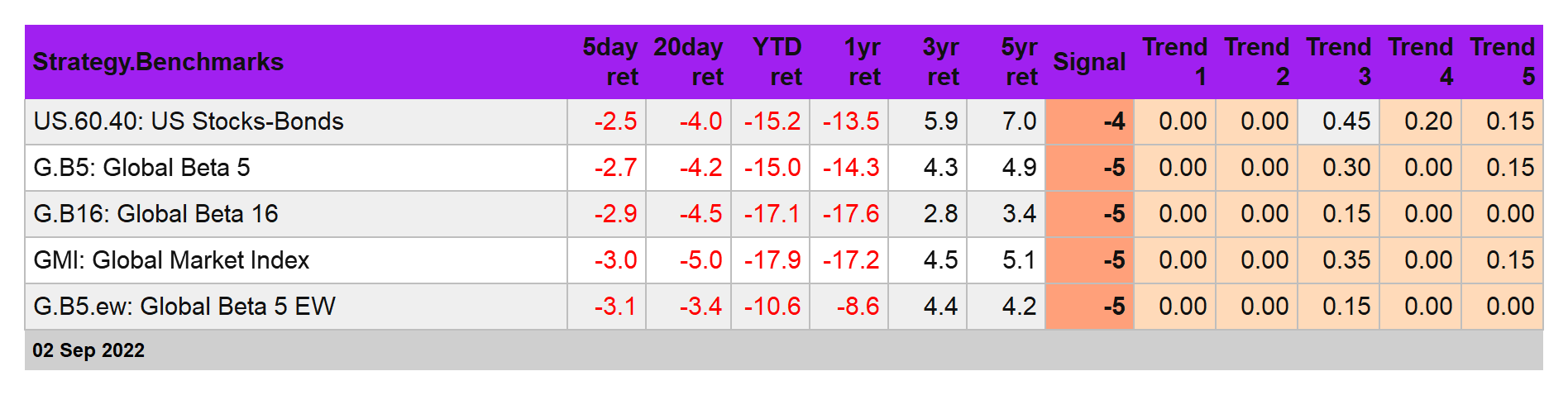

That’s also the message in our portfolio strategy benchmarks, which continue to lose ground (see this summary for design details). There will be rallies ahead, but in the search for a high-confidence estimate of a major trough these are still early days. ■