The ETF Portfolio Strategist: 6 Nov 2021

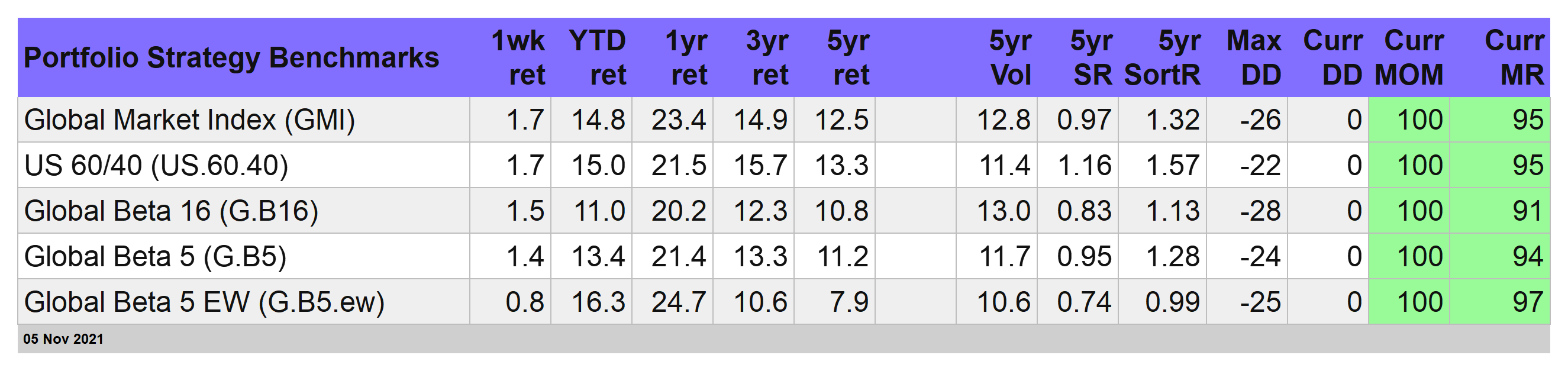

Portfolio Strategy Benchmarks

US small-cap stocks surge during a mostly risk-on week for global markets

A strong week of gains for our portfolio strategy benchmarks

They’re alive! After trading in a tight holding pattern for much of the year, small-company stocks in the US broke out of the trading range in stark terms during this week’s trading through Friday, Nov. 5.

The iShares Core S&P Small-Cap ETF (IJR) is this week’s big upside outlier after the fund soared 6.4% — a weekly advance that lifted the ETF to a record high that’s far above the previous levels of 2021’s high-end range. For details on metrics in the table, see this summary.

What’s the catalyst for the rally? The ongoing run higher in US stocks generally is certainly a factor. It helps that today’s US employment report for October posted a much-stronger gain than expected. My analysis on the fourth-quarter GDP outlook is also encouraging for the bulls.

Attractive valuations may be a bigger force. MarketWatch.com advised on Friday advised that small-cap shares are “a bargain you can’t ignore” because this slice of equities is “trading at their second-biggest discount in 20 years,” based the weighted forward price-to-earnings ratio for the S&P Small Cap 600 Index. If this week’s trading activity is a guide, no one’s ignoring this slice of stocks any longer.

Whatever the explanation, the crowd suddenly appears to be focused on the opportunities that have accompanied small-cap beta through history — opportunities that, in recent years, has been on hiatus in some degree as big-cap shares stole the show.

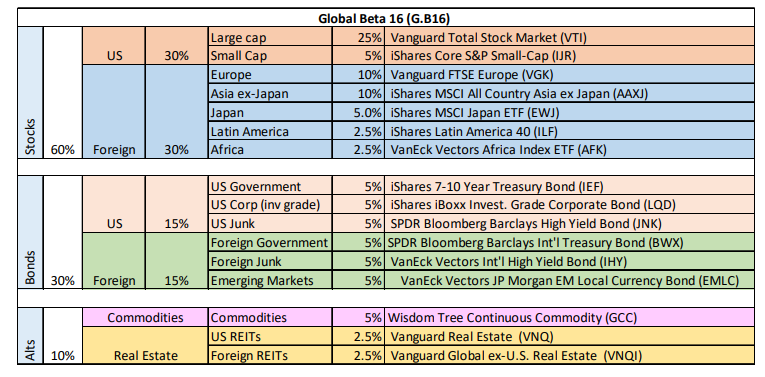

Has a new era of small-cap outperformance arrived? Maybe, although it’s too early to declare with high confidence that regime shift has arrived. Consider the next chart below, which shows the ratio of small caps (IJR) to large caps (VTI). When the line is rising (falling), small caps are outperforming (underperforming). On that basis, there was a extended run of small-cap outperformance in late-2020 into this year’s first quarter. But that leadership reversed over much of the past six months and its been in a holding pattern ever since. Are small caps again shifting to high gear for equity-market leadership?

One week of trading is hardly decisive, even a big week of upside action. Let’s see if there’s follow-through in the weeks ahead for IJR. Meanwhile, let’s not overlook that IJR is now the strongest-performing ETF year to date in our standard opportunity set (defined by the table above). In what might be called a stealth rally, US small-caps have quietly (and now suddenly) burst into the leadership role for risk assets in 2021.

Let’s also recognize that the week just ended was unusually kind to risk assets generally. The only losers on our list of global assets: Asia ex-Japan (AAXJ) and commodities (GCC).

AAXJ continues to suffer from a hefty allocation to equities in China. Analysts are debating if the country’s stocks have entered bear-market territory, but the market numbers for Asia generally (excluding Japan and including China) have already issued a verdict. Indeed, the momentum score (MOM in the table above) for AAXJ continues to reflect a deeply bearish profile. The ETF’s trend line in the chart below doesn’t disagree.

A burning question is whether avoiding China’s equities is timely. For investors inclined to make this bet, there are several ETF choices to consider, including iShares MSCI Emerging Markets ex China ETF (EMXC). Not surprisingly in the current climate, EMXC is outperforming AAXJ and a broad emerging markets fund (VWO) this year.

Commodities are this week’s other loser via WisdomTree Continuous Commodity Index (GCC), which shed 1.0%. But the trend line here still looks productive. Although GCC has fell for three straight weeks, the setbacks are mild and, for the moment, nowhere near signaling a reversal in the upside trend. GCC’s red-hot MOM score agrees.

In other words, GCC appears to be going through a healthy correction that may set it up for greater heights. Much depends on how quickly inflation fades and, perhaps more importantly, the evolution in the strength and persistence of the economic recovery. On both counts, the numbers still point to a favorable backdrop for commodities.

Bottom line: the odds still look encouraging for expecting that GCC’s rally to resume and lift the fund to new highs before this cycle runs its course.

Up, up and away: The rising tide of market betas lifted all our strategy benchmark boats this week.

Although there’s a fair amount of variation in the year-to-date results, it’s clear the risk continues to be priced higher with a high degree of upside momentum. Indeed, the MOM score for all our benchmarks remain pinned to 100, the highest reading.

Note, too, that all the benchmarks are again enjoying zero drawdown. Ill advised or not, markets are generally pricing in sunny skies ahead. There are countless reasons to question the logic, but for the moment the crowd continues to vote with its money and the implied forecast remains unmistakably bullish.

Rock-ribbed contrarians with a high tolerance for risk (and tracking error) may be inclined to think (and act) otherwise. Ditto for investors with a low tolerance for risk. For everyone else, taking a bit of money off the table seems reasonable in moderation, but it’s (still) not obvious that the party’s about to crash. ■

Great stuff, well covered.