The ETF Portfolio Strategist: 6 November 2022

Trend Watch: Global Markets & Portfolio Strategy Benchmarks

A number of markets continued to recover last week, but big picture still suggests bear-market rallies are intact. Confidently calling the true bottom for the cycle is only possible after the fact and so staying defensive in real time until there are clear signals otherwise virtually assures that you’ll be late to the risk-on party. But that’s a calculated risk and one that informs the thinking on these pages.

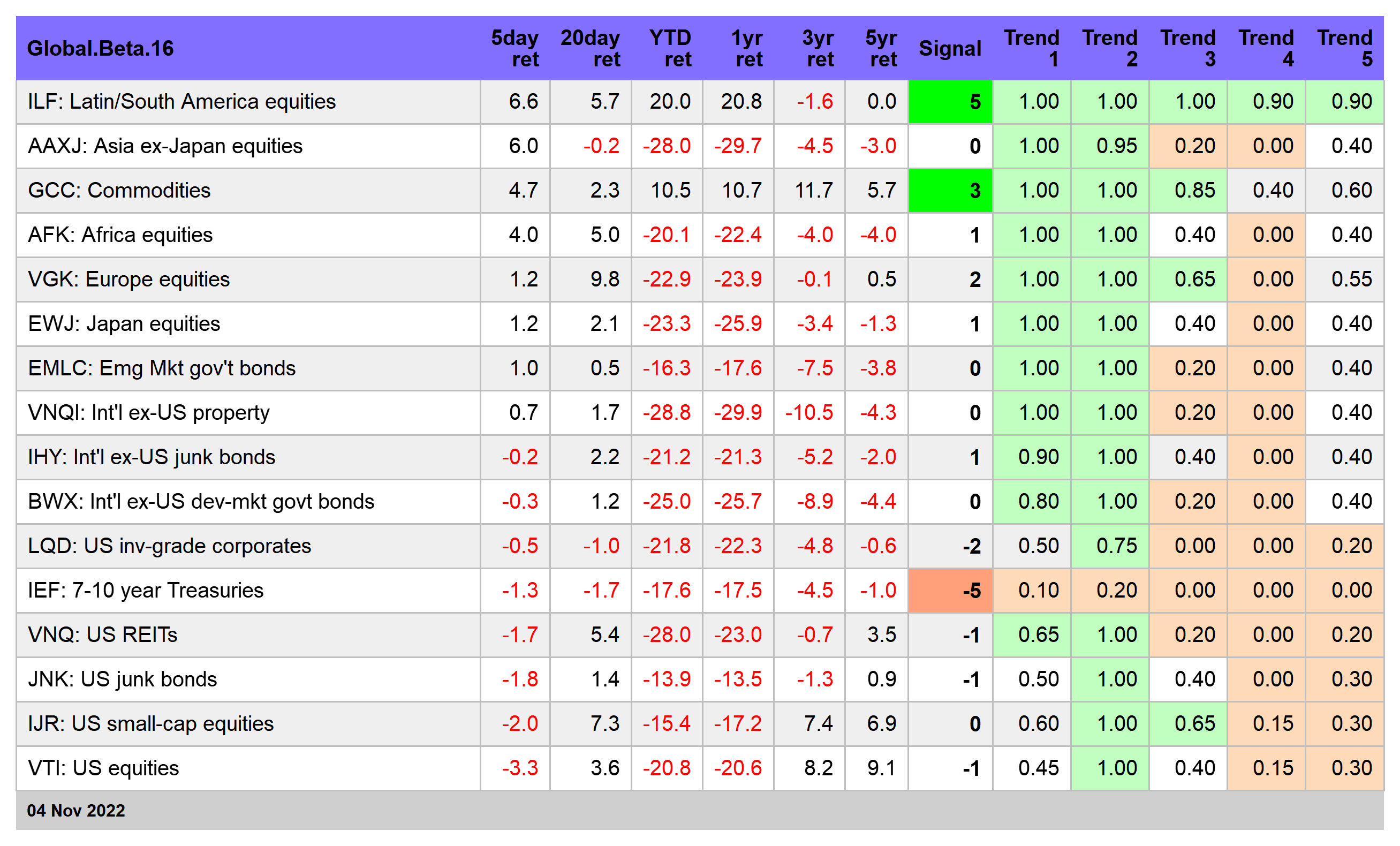

Against that backdrop, stocks in Latin America continue to buck the broad trend and posted the strongest weekly advance for our 16-fund global opportunity set.

The iShares Latin America 40 ETF (ILF) has been a familiar name in recent history as an upside outlier and the latest bounce reaffirms that status. ILF surged 6.7% in the trading week through Friday’s close, lifting the fund to its highest level since June. The rally pushed ILF’s Signal score to a maximum bullish score of +5 (For details on the Signal methodology, see this summary). The implication: there’s still room to run higher for ILF.

Meanwhile, the recent rally in US stocks faded. Vanguard Total US Stock Market (VTI) lost 3.3% last week, the deepest setback for the opportunity set listed above. The fund’s Signal score is a slightly bearish -1, which adds another clue for seeing the recent jump as another bear-market rally. It’s also telling that the weekly price chart for VTI continues to reflect a conspicuous downside bias. A key test: VTI can rally above its recent high of around $195. Equally important: Will the recent low of $180 give way in the next leg down? The answers will be telling for deciding if the bear market is ongoing or not. A number of analysts speculate that the selling is overdone and the correction is over, or close to ending. Maybe, but as long as the highs and lows keep sinking, as they continue to do so year to date, there’s still a good case to stay defensive.

For readers who are inclined to speculate otherwise, focusing on relatively strong markets offers better odds. ILF is one example, as noted above. Another: broadly defined commodities (GCC), which are showing a bit of strength again.

GCC is the third-best performer for the week, popping 4.7%, a second straight gain that lifted the ETF to its highest close since August. The fund’s Signal reading is moderately bullish at +3, which strengthens the possibility that GCC’s latest rally will continue. Part of the reason commodities are catching a bid again: expectations that China will soon ease or end its zero-Covid policy, which has kept a lid on the country’s economic growth and reduced global demand for commodities. But this is speculative thinking and it’s not obvious that a change is near. As a result, the bounce in commodities could easily reverse until/if China announces a formal policy shift. But after yesterday’s news that Beijing plans to continue its "dynamic-clearing" approach to managing the virus, the odds for a sustained run in commodities are wobbly at best.

The trend data for our portfolio strategy benchmarks is no longer uniformly bearish in the extreme, but that’s hardly a risk-on signal. See this summary for design details on the benchmarks. The good news: the Signal scores are now flirting with neutral readings, which is an improvement relative to recent weeks. But macro headwinds are still blowing hard (rate hikes and their aftermath in particular). Meanwhile, damage repair for trend behavior has a long way to go in the wake of 2022’s selling. The slide in multi-asset-class portfolios may be easing, or perhaps stabilizing, but it’s premature to turn off the warning sign. Let’s see if the benchmarks can at least hold their ground for a few weeks before assuming the worst has passed. ■