The ETF Portfolio Strategist: 7 Jan 2022

Portfolio Strategy Benchmarks

Risk appetite takes a hit as interest rates rise, with some notable exceptions

Portfolio strategy benchmarks post sharp losses this week

Risk-off roils global markets, but not completely: Selling dominated the trading week through Friday, Jan. 7, but it wasn’t a complete rout. Broad market measures for equities and bonds suffered haircuts, but several key slices of stocks bucked the trend — value shares and emerging markets ex-China, in particular. Note, too that commodities rallied this week.

Let’s start with the big picture using our standard 16-fund global opportunity set. There was a wide range of results this week—more than a five-percentage point spread, with commodities leading the winners. For details on the return and risk metrics in the table below, see this summary.

WisdomTree Continuous Commodity (GCC) rallied 1.2%, lifting the fund to a level that’s near its highest since November.

The head of commodities research at Goldman Sachs sees an extended bull market brewing for raw materials, driven in part by shortages and a global economy flooded with liquidity. “The best place to be right now, particularly given the Fed pivot [to tighter monetary policy], are commodities,” says Jeff Currie. “We think you’re going to see another year of out-performance of commodities and real assets more broadly.”

Meanwhile, foreign shares offered valuable ballast to the US equity market selloff this week. Moderate gains were posted for stocks in Africa (AFK), Latin America (ILF) and Europe (VGK).

The price increases in foreign shares stand in sharp contrast to the sharp slide in US stocks this week. Vanguard Total US Stock Market fell 2.2%. That’s a hefty loss, but in the context of recent history it’s relatively trivial. The long-running upside bias for VTI may be fading, but it’s too early to make that call. Nonetheless, VTI is struggling to rise above its recent highs. It’s unclear if a period of consolidation will keep the fund in a trading range for the near term or the start of an extended correction. But given the extraordinary gains for VTI in recent history, a cautious outlook looks reasonable as the US market digests what appears to be a shift in Federal Reserve policy toward tighter monetary policy.

Note that when we break US stocks into growth and value components, the week delivered sharply divergent results. Notably, large-cap value stocks (IWD) rallied for a third week, gaining 0.8%. Large-cap growth (IWF), by contrast, tumbled nearly 5%.

Some analysts see a rotation to the value factor in progress, triggered by the Federal Reserve’s shift to combat higher inflation with a bias toward hawkish policy. “It’s not a one-day rotation; this is the beginning of potentially a six- to 12-month rotation from growth into value,” predicts Luca Paolini, chief strategist at Pictet Asset Management. “The market has made a reassessment of the risk of monetary tightening and I think the market now is right.”

Note, too, that emerging markets ex-China is looking stronger this week. The iShares Emerging Markets ETF (EEM) — with nearly a one-third allocation to China — continues to show a moderate downside bias (despite a fractional increase this week). Meantime, iShares Emerging Markets ex-China ETF (EMXC) rallied 0.5% and remains close to a three-month high.

Steering clear of China stocks (or at least minimizing exposure) is becoming a topical talking point these days in the wake of Beijing’s recent actions that take a harsh view of capitalism. By some accounts, nothing less than avoiding the country completely will do.

“China is uninvestible, in my opinion, at this point,” says Jeffrey Gundlach, founder of Doubline, a bond shop. “I've never invested in China long or short. Why is that? I don't trust the data. I don't trust the relationship between the United States and China anymore. I think that investments in China could be confiscated. I think there's a risk of that.”

Speaking of risk, bonds across the board took a blow this week. The iShares 7-10 Year Treasury Bond ETF (IEF), for example, suffered a 2.0% setback, cutting the fund to its lowest price since last April.

The catalyst, of course, is a growing sense that the Federal Reserve will raise interest rates, perhaps as early as the March FOMC meeting, according to Fed funds futures data. Reflecting the shift in sentiment, the 10-year Treasury yield jumped to 1.76% today — the highest in nearly two years.

The deepest loss this week for our opportunity set: US real estate investment trusts (REITs). Vanguard US Real Estate lost a hefty 4.3%. Keep in mind, however, that VNQ has been on a tear recently and so the market was probably looking for an excuse to take some profits. The prospect of higher interest rates did the trick for a corner of the market that’s prized for relatively high yields.

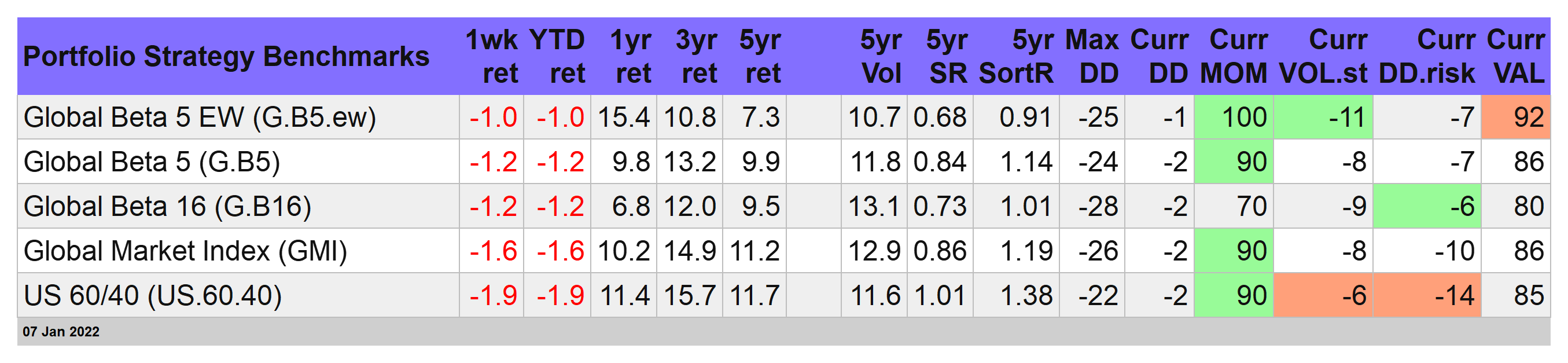

Portfolio strategy benchmarks sink: There was no mercy this week for our strategy benchmarks. Thanks to widespread losses in global markets, the benchmarks gave up 1.0% to 1.9% for the trading week. See this summary for an overview of benchmark rules.

Our standard benchmark — Global Beta 16 (G.B16), which holds all the ETFs listed in the table above — is starting to look wobbly, albeit on the margins.

A more pressing warning may be brewing in the US 60/40 stock/bond benchmark (US.60.40), courtesy of relatively week readings on volatility and drawdown (VOL.st and DD.risk, respectively). But for now, as long as the momentum score (MOM) is bullish (as it is at the moment), it appears that US.60.40’s latest setback is noise. Let’s see if that changes in next week’s trading and news cycle. ■