The ETF Portfolio Strategist: 7 May 2021

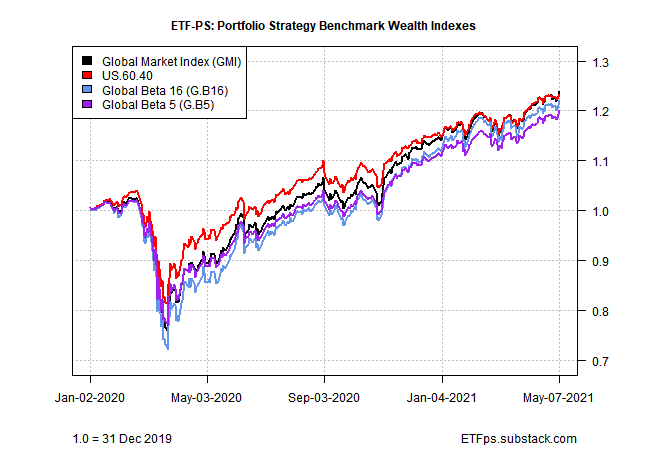

Portfolio Strategy Benchmarks

In this issue:

Big miss for US payrolls today, but it spurs widespread rallies

Across-the-board gains for the portfolio benchmarks

Disappointing payrolls data sparks risk rally: The crowd was looking for close to a 1-million increase in jobs for April in this morning’s update from the US Labor Dept. Instead, jobs rose by a relatively modest 266,000 last month. As downside gaps go, that was a monster. But if dramatically weaker-than-expected growth was an excuse to run for cover, the evidence was thin in today’s generally upside trading session (May 7).

The renewed risk-on reasoning seems to be that if the labor market is recovering at a pace that’s slower than expected, the Federal Reserve can be patient with rate hikes for longer than expected. Whether that proves to be true or not, markets generally read today’s employment news as another excuse to buy.

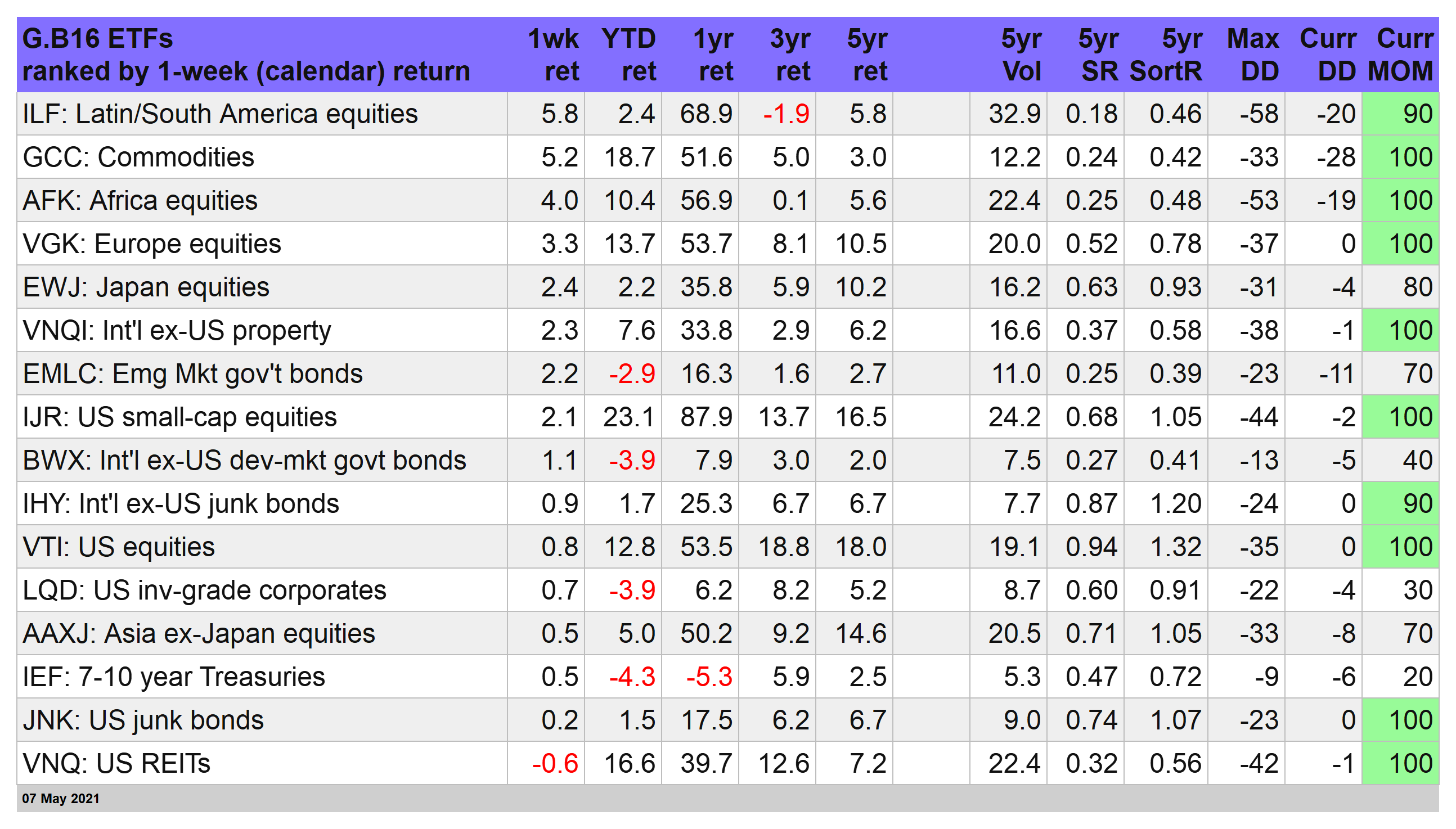

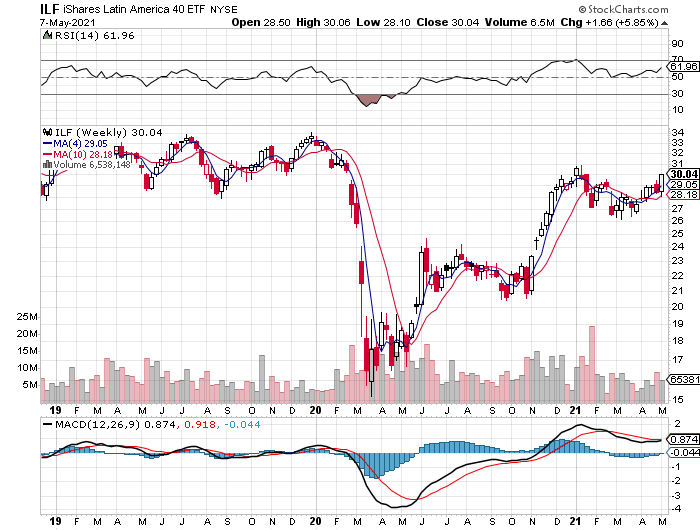

Save for US real estate investment trusts, every slice of our global ETF opportunity set jumped for the trading week through May 7. The leader: shares in Latin America. The iShares Latin America 40 ETF (ILF) seems to be making a new play at taking out its previous high and perhaps going on to repair the remaining damage from last year’s pandemic selloff.

Despite a second-place finish, the real star of the week: commodities, which continued to rally. WisdomTree Continuous Commodity (GCC), which tracks a broad, equal-weighted index of commodities, is on fire. The ETF jumped 5.2% this week—the sixth straight weekly advance. Growing anxiety about inflation is keeping the asset class on everyone’s short list of hedges. Then again, how does that sentiment square with a materially weaker job market in the US? Perhaps the crowd will sort it out next week.

Meanwhile, the soft payrolls report kept the benchmark 10-year rate treading water this week (it slipped a bit to 1.60%). For the moment, rates remain on hold after running higher through mid-March. The bond market is increasingly of a mind to price in expectations that rates will remain steady or slip for the foreseeable future. Of course, that depends on how hot (or not) next week’s consumer inflation report for April compares.

This week, however, the iShares 7-10 Year Treasury Bond ETF (IEF) certainly got a break and managed to rise 0.5%. That was enough to lift the fund close to its best close in nearly two months.

US real estate was the odd man out this week, suffering the only loss for our 16-fund global opportunity set. That’s hardly a tragedy since Vanguard US Real Estate’s (VNQ) setback is the first weekly loss after a marathon six-week rally.

Follow the bouncing benchmarks: After a brief setback at the end of April, our suite of portfolio strategy benchmarks regained their upside bias and posted solid gains this week.

Leading the charge higher: Global Beta 5 (G.B5). Theis five-fund portfolio rose 1.3%. The weakest performer: US 60/40 (US.60.40), which advanced 0.6%. For details on all the strategy rules and risk metrics, see this summary.

For the year-to-date column, Global Beta 16 (G.B16), which holds all the funds in the first table above (in weights shown below), continues to hold the top spot. The portfolio’s 8.6% return so far in 2021 is impressive, but it’s peanuts next to the strategy’s one-year gain: 41.1%, which is also the leading benchmark return for that time window too.

How long can these stellar gains continue? History suggests that we’re near the as-good-as-it-gets mark. Of course, if today’s attitude adjustment re: the interest-rate outlook has legs, we could be headed for a new bull wave in the weeks ahead. ■